|

|

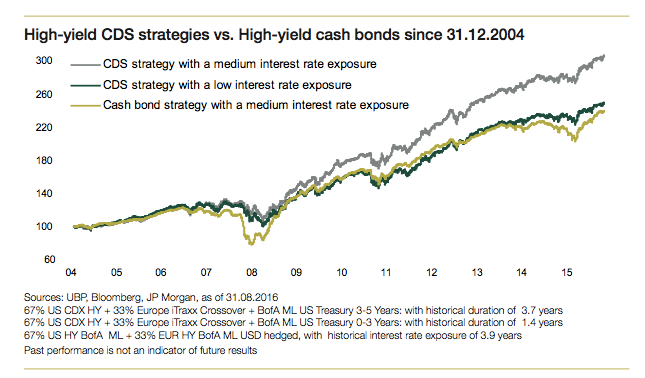

Investing in high-yield bonds can be profitable but it can also be risky, particularly in the current rising interest rate environment. But by using credit default swap (CDS) indices an investor can generate five-year credit spreads without taking on the duration risk that comes with a five-year investment period.

Investors can generate five-year credit spreads with the instrument without taking on duration risks. UBP Asset Management is one management firm that uses CDS indices for investing in high-yield bonds. Using this strategy, the firm generated US$4.8 billion in assets under management (AUM) since 2010.

Where most fund managers invest in high-yield bonds using a bottom-up process with fundamental credit selectors, UBP approaches high-yield bond investing via top-down macro methodology that employs CDS indices.

A CDS index serves as a gauge of apprehension in credit markets. A CDS index typically falls when perception of credit risk decreases and rises when sentiment deteriorates.

“We don’t invest in cash high-yield bonds but we invest via CDS indices. The way we play it is that we are sellers of credit protection, capturing full exposure into five-year credit spreads,” says Ted Holland,

managing director, Asset Management and head of Business Development at UBP Asset Management Asia Ltd., in an interview with The Asset.

A CDS is basically an OTC derivative designed to transfer the credit exposure of bonds between two or more parties and bears no interest rate sensitivity or interest rate risk. By investing in CDS indices, UBP is able to get high-yield bonds with five-year spreads without taking on their interest rate risk.

UBP then uses the cash that they would have invested in the high-yield bonds and invests them in short-dated US treasury bonds with zero-to-two-year maturities. In this way, the strategy’s sensitivity to interest rates is limited since its exposure to interest rates is achieved primarily via US treasury bonds with maturities of less than two years.

“This way we are tweaking the interest rate exposure. For example, if today the interest rate exposure is around 1.2-years or 1.3-years, we have an arbitrage to where we’re getting full exposure to the five-year spread. If we were to get that five-year spread within the cash fund portfolio, we will be taking on that duration risk that comes with the five-years exposure,” says Holland.

Market data indicate that high-yield CDS indices provide much better liquidity and have very low transaction costs as opposed to standard high-yield bonds, even during crises.

Since December 2004, the high-yield CDS index market has an excellent level of liquidity in all market conditions, in particular compared to the regular high-yield bond market, with very tight and stable bid-offer spreads.

This CDS index-based strategy is suitable for the current rising-interest rate environment where the investment options are limited to investing cash in high-yield bonds with five-year maturity and having to take on the duration risk, or investing in shorter duration bonds and giving up the five-year credit spread.

“This way we’re maintaining a five-year spread, yet getting short duration on your interest rate sensitivity,” says Holland.

UBP launched this strategy seven years ago and it’s now the top high-yield bond fund for US, global and short duration funds.

“This is an innovative fund that provides liquid exposure to the high return potential of high-yield credit with limited interest-rate risk through a top-down investment process. The environment remains positive for high-yield, with default rates at low levels,” says Holland.