The pressure of mass capital flight has been temporarily alleviated in China on the back of a stronger renminbi and higher onshore asset valuations and yields.

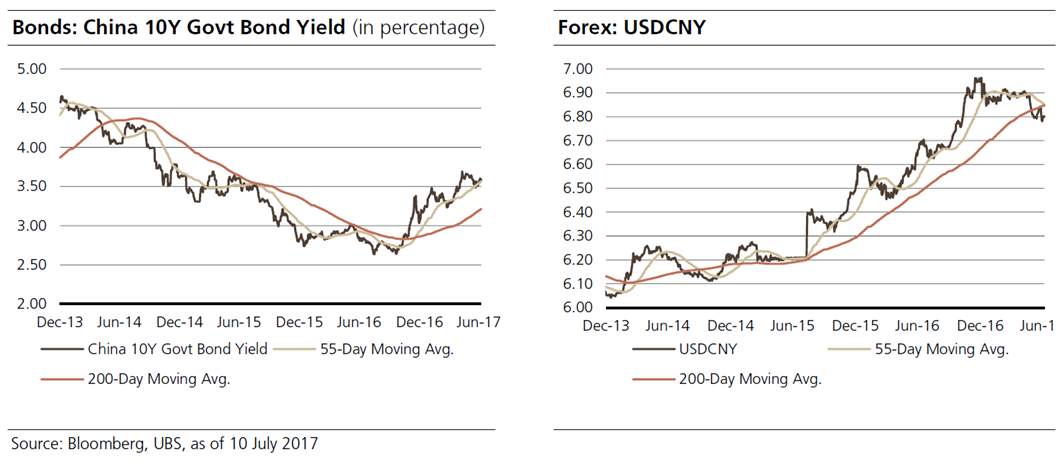

“It is a result of natural evolution due to asset returns. In the first half of the year, Chinese ten-year government bond yields widened by around 100bp, and in the same period US ten-year bond yields dropped by around 30bp,” explains Wenjie Lu, China investment strategist at BlackRock. “Chinese assets look more attractive compared to offshore assets. That is a strong reason why capital outflow has slowed down.”

As a reflection of capital flight, China’s FX reserves shrank for eight consecutive months in a row as of January 2017, due to the Chinese government’s attempts to stop the renminbi depreciating too rapidly. The renminbi depreciated over 10% in almost a year-and-a-half, from August 2015 (when the renminbi reform began) to the end of 2016. The expectation of further renminbi depreciation gave rise to strong demand among Chinese corporates to acquire overseas assets.

As a reflection of capital flight, China’s FX reserves shrank for eight consecutive months in a row as of January 2017, due to the Chinese government’s attempts to stop the renminbi depreciating too rapidly. The renminbi depreciated over 10% in almost a year-and-a-half, from August 2015 (when the renminbi reform began) to the end of 2016. The expectation of further renminbi depreciation gave rise to strong demand among Chinese corporates to acquire overseas assets.

For the past few years, Chinese conglomerates such as HNA Group and Fosun Group have been aggressively acquiring overseas assets to diversify their portfolios as well as hedge their currency risk. Data from Dealogic show that for the past five years, overseas acquisitions from Wanda Group, Anbang Group, HNA Group and Fosun Group totaled US$41 billion.

The depreciation of the renminbi since 2015 was regarded as a major motivation of Chinese corporates to acquire offshore assets. On the other hand, large overseas M&As also accelerated the capital outflow as a result.

Since the start of 2017, China started to closely monitor outbound investment by Chinese corporates. Government bodies began making statements condemning what they deemed as ‘unreasonable’ outbound acquisitions.

The authorities’ rhetoric indicates that ‘unreasonable’ outbound activities include highly leveraged deals, high-risk deals, or deals in unrelated industries, whilst ‘reasonable’ deals would meet the expansion needs of a company or meet a government objective, such as participating in the Belt Road initiative.

In a press conference held by the National Development and Reform Commission (NDRC), Pengcheng Yan, a spokesperson for NDRC, stated that it will continue to keep an eye on ‘unreasonable’ outbound investment in real estate, hotels, cinemas, entertainment and football clubs. This was soon echoed by the State Administration of Foreign Exchange (SAFE). According to SAFE, it will collaborate with other authorities to monitor ‘unreasonable’ outbound activities while still encouraging 'reasonable' M&As.

According to Yan, NDRC supports corporates with real expansion needs who wish to partake in outbound acquisitions, and particularly supports projects under the Belt Road initiative. In the first half of 2017, China’s trade activity grew significantly with Belt-Road countries. Trade volumes with Asean countries, India and Russia increased by 21.9%, 30.4% and 33.1%, respectively.

During the first half of 2017, China's outbound direct investment was 331.1 billion yuan, 42.9% down from the same period in 2016. According to Keming Qian, a spokesperson at the Ministry of Commerce, outbound investment classified as ‘unreasonable’ has also slowed in the first half of 2017.

“Chinese policy makers have no problem with M&A or investment but if these companies have to rely on very high leverage, even some shadow credit tools, there are some restrictions,” says Lu. “Going forward, with the appreciation of the currency and given that the growth and stability of the economy are improving, I do not expect there will be strong outflows in the coming quarter.”