When the People’s Bank of China (PBoC), first announced the country’s onshore bond market would be opened to most foreign institutional investors, the market reacted with excitement. A catalogue of more than 100 questions was submitted to the PBoC within just three days of the announcement in late February, seeking clarification on operational issues and risk management on the China Interbank Bond Market (CIBM). Recognizing the potential for wide-scale capital inflow if foreign investors pursue the new channel, the PBoC wasted little time in providing feedback.

On May 27, investors received the comprehensive guidelines they had requested.

Barnaby Nelson, Standard Chartered’s managing director of investors and intermediaries, Northeast Asia and Greater China, speaks for many of his peers when calling the clarified rules “significantly more liberal than expected” and predicting “enormous take-up” of this “core mechanism of the future.”

Indeed, among 900 institutional investors polled by Standard Chartered globally just weeks after the liberalization was first announced, 33% said they were keen to register with the PBoC and invest in the onshore bond market.

According to Nelson, the new channel to China’s onshore bond market will be utilized first by those already familiar with the market - licensed Qualified Foreign Institutional Investors (QFIIs) and Renminbi QFIIs. These companies already have portfolios of onshore bonds but, once registered with the PBoC, would no longer be subject to any quota.

Showcasing the type of coordination among regulators that some had found wanting in the past, the State Administration of Foreign Exchange (SAFE) also announced in late May that foreign investors in the interbank bond market will also be able to access the onshore rates markets freely.

This ability to hedge underlying positions through derivatives “removes one major hindrance for these investors”, remarks Frances Cheung, head of rates strategy for Asia ex-Japan at Société Générale. “That said,” she continues, “initial bond inflows will be dwarfed by the sheer size of the onshore market and thus [fail to make a] material impact on CNY rates and yields.”

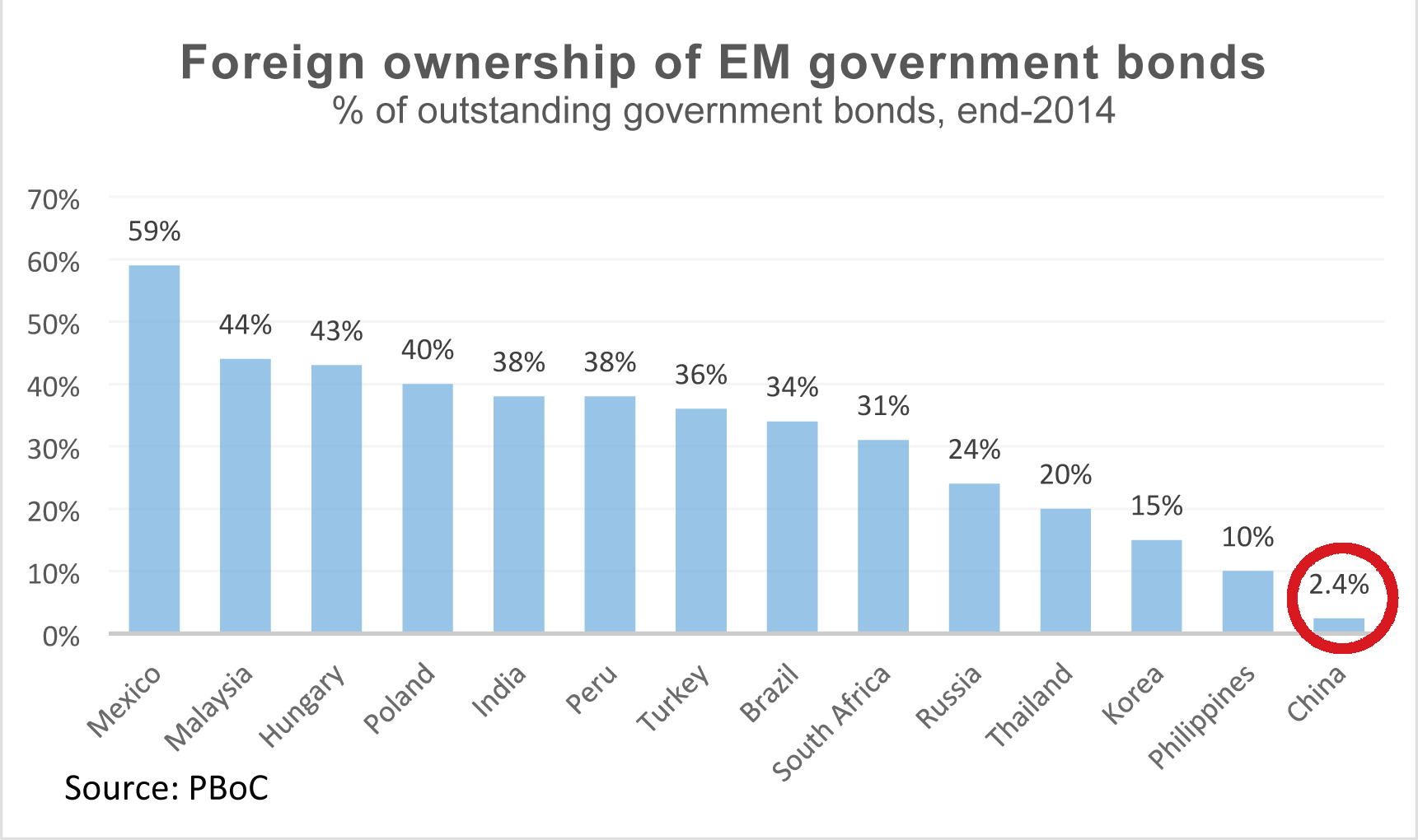

That leaves liquidity as a factor that foreign investors could improve. Yet, the track record of those already allowed to invest suggests otherwise. According to Lukas Petrikas, SVP of group strategy at Hong Kong Exchanges and Clearing (HKEx), speaking at a roundtable organized by Standard Chartered, foreign investors currently hold 2% of the onshore bond market “but account for only 0.5% of daily turnover”. Unless the mix of foreign investors broadens, this is unlikely to change, he continues.

While the PBOC has clarified that the new channel is designed for “medium and long term investors”, Nelson highlights an important nuance in the scheme that may allow a wider range of asset managers to participate. “We have had retail brokers and hedge funds turn up – they all want a piece of the action. [The fact is that] it is the onshore settlement agent who is registering [an investor] with the PBOC [and] we believe there is a case to be made to the PBOC that some of these guys are basically asset managers as opposed to hedge funds. If you don’t short, how are you realistically different from any other investor?”

The question will be, he adds, whether an investor’s onshore custodian is willing to vouch for the client and how the regulator defines a short, medium and long term investor. Potentially, though, there is a possibility that more opportunistic investors which turn over their portfolio more often will be deemed eligible for the channel.

Notably, multinational corporates have had a very different experience with Chinese regulators since the beginning of the year—marked by backtracking rather than further reform. Following the wider use of intercompany loans to repatriate earnings out of China and the landmark introduction of cross-border cash pooling nationwide in 2014, this year has witnessed the reversal of many of these reforms. Cash pools today can no longer be in a net deficit position and even dividend payments (which are already subject to 10% withholding tax) are virtually impossible, one treasury manager of a large European multinational corporation (MNC) confirms. For many profitable MNCs in China, the liberalization process witnessed a brusque end this year amid fears over capital outflows.

Perhaps investors would do well to study this recent experience of corporates before they get too excited about new investment channels giving access to the onshore bond market. Because at some point, they will want to redeem their investments. - Additional reporting by Derrick Hong