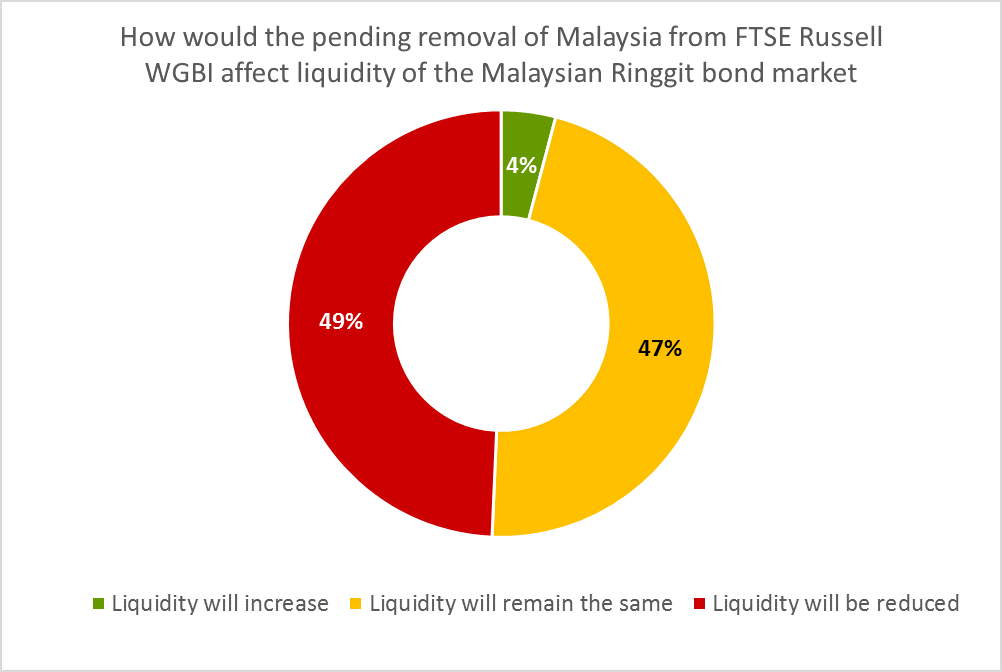

Facing a potential removal from the FTSE World Government Bond Index (WGBI), half of the sellside individuals (49%) active in the ringgit bond market expect liquidity to decrease while the other half (51%) believes it will remain the same or even increase, according to the latest survey done by Asset Benchmark Research (ABR).

On April 15, FTSE Russell announced it would put Malaysia (which has been included in the WGBI since 2007) on a watch list and is considering downgrading the country from “2” to “1”, which would render it ineligible for inclusion in the WGBI.

The 49% of the individuals who are expecting a reduction in liquidity expect that offshore funds will be “forced” to withdraw from the ringgit bond market if the removal were finalized. “It is estimated that US$2-3 trillion of funds are benchmarked against the WGBI, of which Malaysia’s weight is 0.4% (US$8 billion at the low end). Hence, there is a potential outflow of 20-33 billion ringgit, should the exclusion from FTSE index materialize,” says a senior dealer of a local bank.

Yet, the rest (51%) of the respondents suggest that a sell-off could pose a buying opportunity to local investors, who would enter the market trough with strong appetite, keeping liquidity more or less the same level. “Local MYR investors are short of MYR assets to buy. If there is any sell off due to the removal, local investors can easily mop it up. It is just a matter of yield and price,” says Kelly Ong, salesperson at Hong Leong Bank.

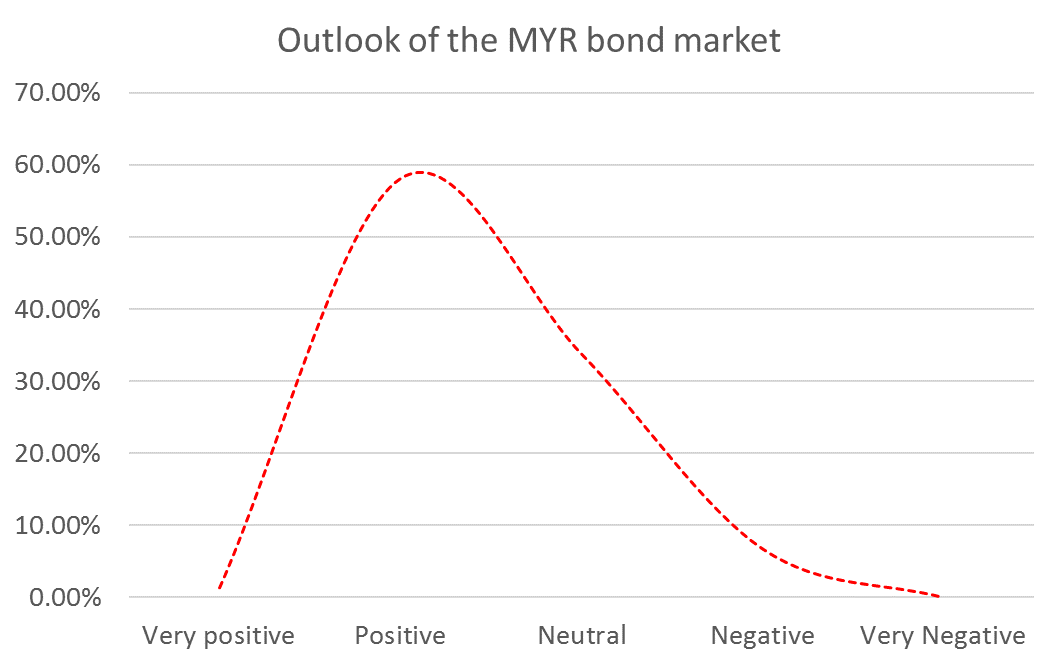

Despite the uncertain expulsion from WGBI, market sentiment remains intact for now. Three out of five (59%) sellside professionals are still either very positive or positive about the outlook of the ringgit bond market in the coming twelve months.

Turnaround is still possible when FTSE Russel will meet with Malaysian regulators in September. Sellside professionals are confident that local authorities will try hard to keep Malaysia in the WGBI. “FTSE Russell said it will meet Malaysia’s regulators and market participants to assess the potential changes and I believe the regulators will try to make sure that Malaysia remains on the WGBI list,” says a salesperson at a local bank.

The survey of 346 sellside individuals took place between April 26 and May 14. The sellside individuals were nominated by investors taking part in the Asian Currency Bond Benchmark Review 2019, which covers 11 markets including China (onshore and offshore), Hong Kong, India, Indonesia, Korea, Malaysia, the Philippines, Singapore, Taiwan and Thailand.

The review has been conducted annually since 2000 and provides a wealth of data on the product needs of investors and the market penetration of the banks that are active in local currency bonds. It also provides detailed analysis on investors’ buying behaviour when selecting their counterparties.

To find out more about Asset Benchmark Research and our work, please click here.

To view the rankings of the best research, sales and trading individuals in Asian local currency bonds by country, please click here.