Chinese private equity firms have taken a more active role in outbound M&A activity as they continue to grow in size, number and sophistication. These outbound investments represent an opportunity for these companies to diversify their portfolio and enter new markets, both in developed and emerging markets.

China-based funds have so far invested US$7.4 billion in cross-border transactions into Europe and the US in the first half of 2016. According to a study by international investment bank Houlihan Lokey, in conjunction with M&A intelligence provider Mergermarket and the Asian Venture Capital Journal, the amount already exceeded the US$5.8 billion invested in 2015.

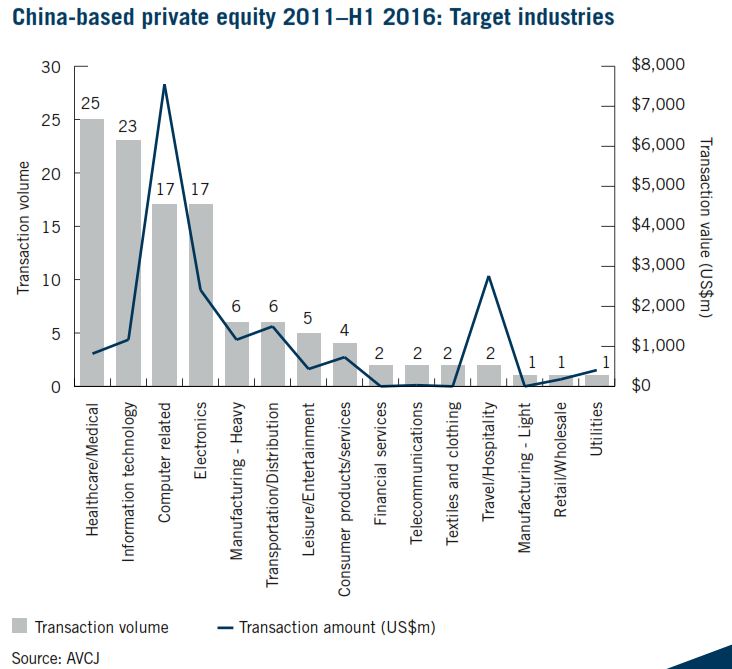

Much of the activity surrounding Chinese private equity investments into Europe and North America has been concentrated in several key sectors, including healthcare and technology. This is underpinned by evolving demographics and the trend to bring global best practices, technologies and products onshore.

Among the notable deals, the Chinese private equity firms participated in the US$3.5 billion takeover of US printer Lexmark International, the US$2.75 billion purchase of Dutch chipmaker NXP Semiconductors’ standard products unit and in the US$600 million acquisition of Norway-based Opera Software’s web browser business.

The healthcare sector is also attracting a lot of interest from the Chinese private equity firms, although the average deal size is comparably smaller. The deals include the US$150 million investment Ally Bridge Group-led consortium in Sorrento Therapeutics, a US-based biopharmaceutical company, and the US$45 million acquisition of Ambrx, a US-based clinical-stage biotechnology company by a consortium involving Hopu Investments and CEL Healthcare Fund.

In looking for targets overseas, the Chinese private equity firms are generally cash-rich with funds typically raised from a mix of state-owned enterprises (SOEs), privately-owned businesses and high net worth individuals (HNWIs). More funding is expected to come from smaller Chinese non-SOEs and HNWIs as they seek high quality assets overseas and China gradually relaxes its controls over foreign exchange.

Jeffrey Wilson, a Houlihan Lokey director in Hong Kong in charge of corporate finance practice, says there are common themes that go beyond the standard strategy of bringing Western brands and technology to the large Chinese domestic market. The overall driver is the maturation of the market for private equity investments in China. “The domestic market has become quite competitive and the valuation for quality assets is relatively high compared to the West, thus some outbound investment can be seen as bargain hunting,” he notes.

But buying overseas assets faces challenges as well and Wilson says the Chinese private equity firms will continue to face regulatory hurdles from Western countries, such as the US, Canada and Australia, which have set up formal review processes for foreign investments.

Sectors that involve sensitive technologies such as aerospace, defence and semiconductors as well as infrastructure sectors are most likely to face regulatory challenges due to concerns over national security. Large and high profile transactions may also trigger antitrust reviews.

Wilson adds, though, that they expect these challenges to gradually diminish as Chinese buyers become increasingly sophisticated in reducing regulators’ concerns by designing smarter deal structures and communicating more effectively with the regulators.