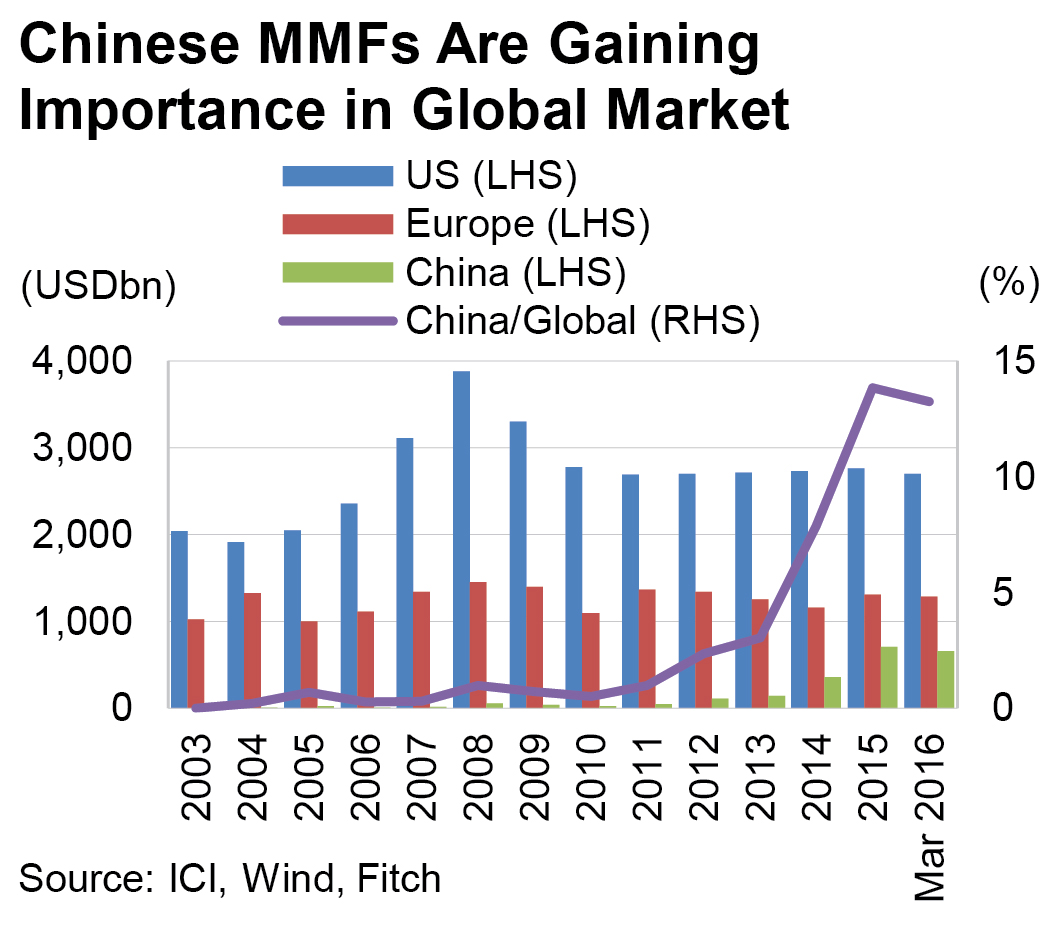

China has become the second-largest money market funds (MMF) domicile following the US representing 13% of the global market compared with just 2% at the beginning of 2013. In the Chinese mutual fund industry, money funds became the largest asset class, representing 55% of the market, according to Fitch Ratings.

Assets under management (AUM) in Chinese MMF were 4.4 trillion yuan (US$ 657 billion) at end-June 2016, little changed at end- 2015. This stabilization belies the growth in this segment in recent years; assets more than doubled in 2015 and AUM at end-June 2016 were 10 times larger than three years ago

Driving the growth are institutional investors that sought safe haven in MMFs after the China stock market crashed last year. Institutional demand surpassed that of retail investors and now accounts for 63% of money fund assets as of end 2015, Fitch notes. Retail demand triggered the rapid expansion of the Chinese money funds market from mid- 2013 and dominated this market until mid-2015. Institutional demand surged following the extreme volatility in the Chinese stock market in June 2015.

“These investors are likely to reallocate assets as new investment opportunities emerge, which could lead to volatile asset flows. Large fund-flows pose challenges for MMF portfolio liquidity management,” notes Fitch.

Among interesting trends is the rise of money market ETFs that surged in the second half of 2015 after the extreme volatility in the stock market. At June 2016 there were a total of 16 money market ETFs with assets totalling 317 billion yuan.

The new Chinese MMF regulations launched in December 2015 have taken effect. Almost all money funds have become compliant with the maturity constraints as of March 2016, limiting the weighted average maturity (WAM) within 120 days.

The new rules require asset managers to implement redemption management tools under certain circumstances. Negotiable certificates of deposit (NCDs) are eligible to MMFs under the new regulation. The growth of NCDs volumes and their improved secondary market liquidity contribute to the liquidity of MMFs’ portfolios.