At a time of growing doubts about China’s economic prospects, India’s rise has been attracting increasing attention, with some predicting that the country will become the developing world’s next economic superstar. Whether you believe India can be the “next China,” however, may depend on whether you subscribe more to “young” or “old” Schumpeterian logic.

The 20th century economist Joseph Schumpeter is best known for the concept of “creative destruction”, which describes how new innovations transform the economy partly by making older technologies obsolete. But Schumpeter’s ideas about economic dynamism and development were not static: whereas he initially emphasized the role of entrepreneurship above all, he later recognized the importance of big businesses.

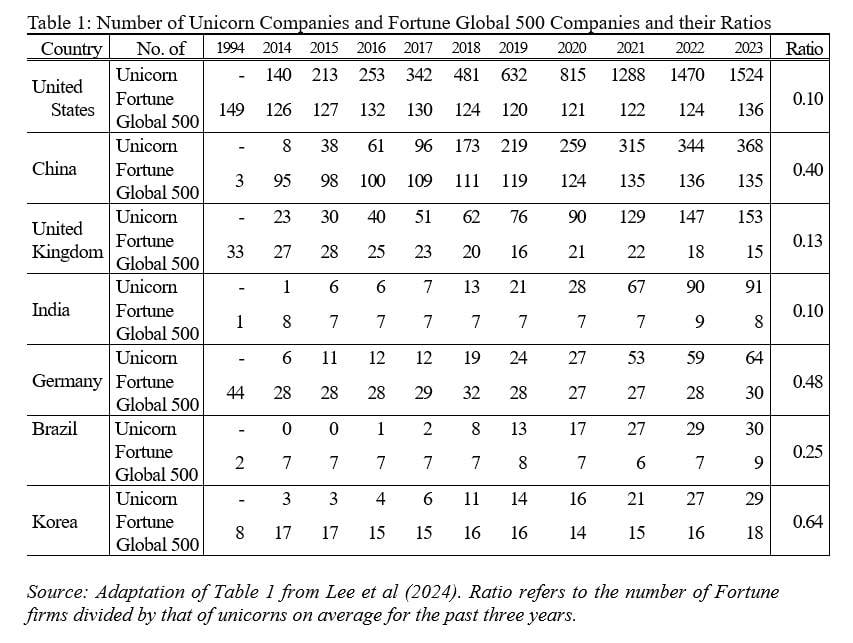

So, in assessing India’s prospects, the “old” Schumpeter might look at the number of big businesses the country has produced (Table 1). India lags well behind China on this front, with just eight Fortune Global 500 companies, compared to its neighbour’s 135. (To put this in perspective, the United States has 136 Fortune Global 500 companies, and South Korea has 18, despite having a much smaller population.) China has achieved this lead over India in just a few decades: in the early 1990s, China had three Fortune Global 500 companies, and India had one.

China has also pulled well ahead of India in terms of per capita income. In 1978 – just before China initiated the “reform and opening up” that enabled its “economic miracle”– both countries’ per capita income amounted to about 5% of the US level. By the early 2010s, Chinese incomes had reached about 20% of the US level, compared to just 10% for India. Today, Chinese and Indian per capita income relative to the US stands at 33% and 13%, respectively.

The fact that China has been far more successful than India in generating world-class big businesses might help to explain this divergence. As my colleagues and I showed in 2013, big businesses contribute significantly to economic growth. By contrast, a larger number of small and medium-size enterprises (SMEs) is only correlated with faster growth, indicating that it may be growth that fuels the proliferation of SMEs, not the other way around.

One reason for this – as “old” Schumpeter might note – is that big businesses tend to execute high-end and high-value-added activities, such as research and development and marketing, at home, while carrying out low-value-added activities abroad. Though the latter can boost growth and facilitate knowledge transfer, latecomer countries must translate this into locally owned, innovative big businesses if they are to break into high-end segments of the global economy.

The “young” Schumpeter might be more impressed by India. That is because India has proved more than capable of generating “unicorns” – private companies with a valuation above US$1 billion – boasting 91 such companies, as of last year (Table 1). To be sure, China far outstrips India here, too, with 368 unicorns. But India remains in the top four globally, behind the US (1,524) and the United Kingdom (153), but ahead of countries like Germany (64), Brazil (30), and South Korea (29).

Yet the discrepancy between Fortune Global 500 businesses and unicorns in India is notable. In 2020-23, that ratio amounted to just 0.1 in India, compared to 0.4 in China, 0.5 in Germany, and 0.25 in Brazil. The ratio in South Korea – whose economy is notoriously dominated by big businesses – is particularly high, at 0.6, implying that big businesses actually facilitate the rise of unicorns.

This likely happens through a few channels. One is the transmission of relevant skills and know-how through employment. To cite one example, the founders of Naver – essentially the “Korean Google” – used to work for Samsung. Another is direct investment: the Chinese tech giant Tencent supports hundreds of start-ups as an equity investor.

The older Schumpeter would probably argue that, if India wants to become an economic superpower on par with China, it should devote more attention to generating big businesses. In fact, without homegrown big businesses to drive growth and investment, India is likely to lose its innovative start-ups to acquisitions by foreign giants.

To avoid this kind of “brain drain”, efforts must be made to help start-ups grow quickly within India, so that they can become the flagship companies of tomorrow. South Korea and Taiwan became high-income economies by growing a few large firms, such as Samsung and Taiwan Semiconductor Manufacturing Company (TSMC), not by having thousands of SMEs. Creating a sound institutional or investment climate to nurture start-ups can take decades. It takes less time to concentrate resources and competencies among a few firms so that they may grow into leading flagship companies.

Keun Lee is a professor of economics at Seoul National University, a fellow at CIFAR, an editor at Research Policy and a former vice-chair of the National Economic Advisory Council for the President of South Korea.

Copyright: Project Syndicate