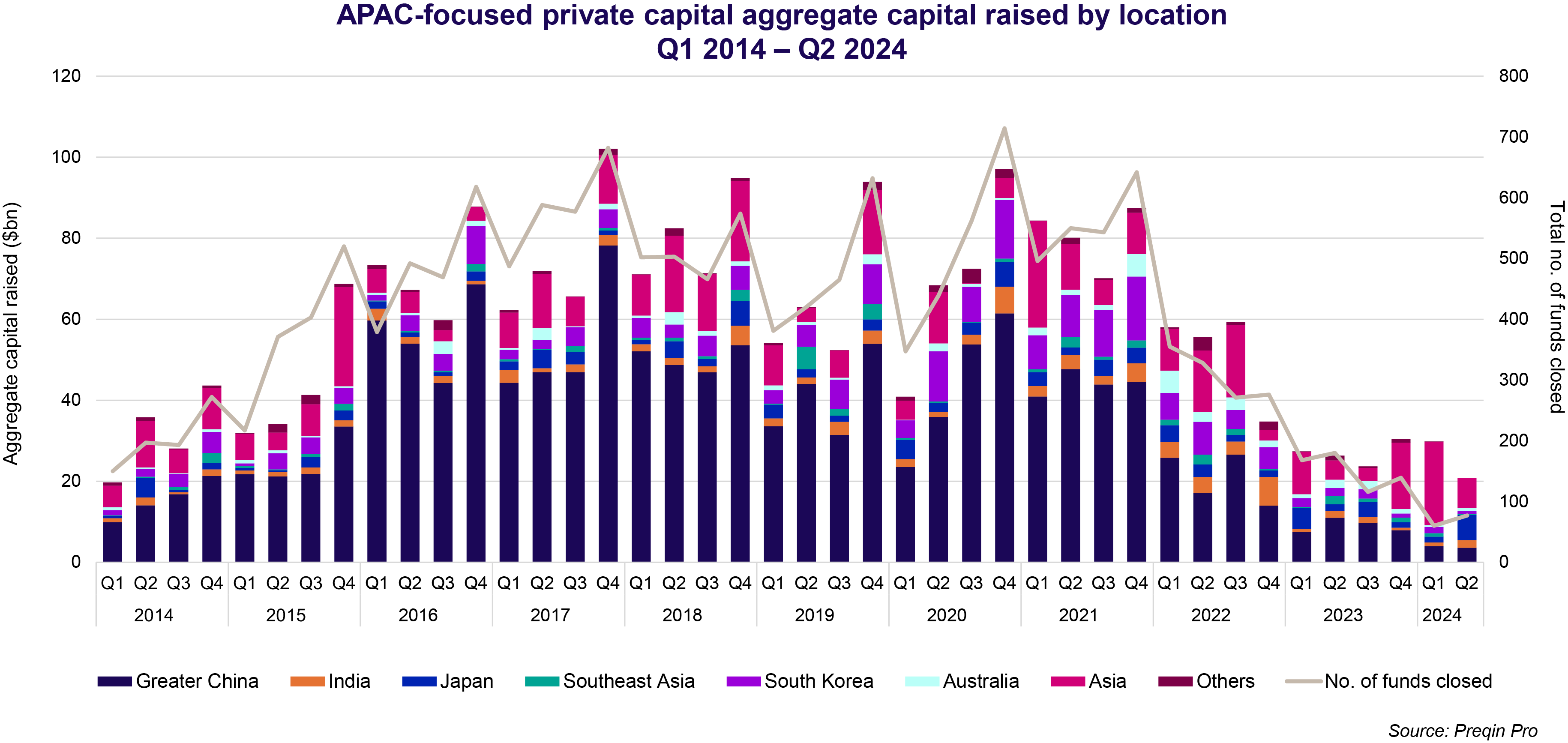

Private capital fundraising activities in Asia-Pacific slowed down in the first half of 2024 as investors remained cautious amid high interest rates and geopolitical tensions.

Asian regional funds sought opportunities throughout the region, instead of focusing on specific countries. Still, several countries such as Japan and India stood out as attractive single markets, Preqin says in a recent webinar, Alternatives in APAC 2024.

Asian regional funds accounted for 53.9% of total capital raised in Asia-Pacific in Q4 2023, and the proportion further grew to 69.1% in Q1 2024, compared with the five-year average of 20.6%. This was mainly contributed by the successful closing of several large funds. In February, for example, CVC Capital Partners closed its latest Asia-focused buyout fund, CVC Capital Partners Asia VI, raising US$6.8 billion, which is higher than its US$6 billion target.

For investors focusing on developed markets, Japan, next to the United States and Western Europe, presents the best investment opportunities in private capital, including private equity, venture capital, and real estate, a Preqin survey finds.

In emerging countries, India has been drawing much attention from investors across all asset classes except hedge funds. In H1 2024, India accounted for a large proportion of the aggregate deal value in Asia-Pacific, mostly involving infrastructure deals.

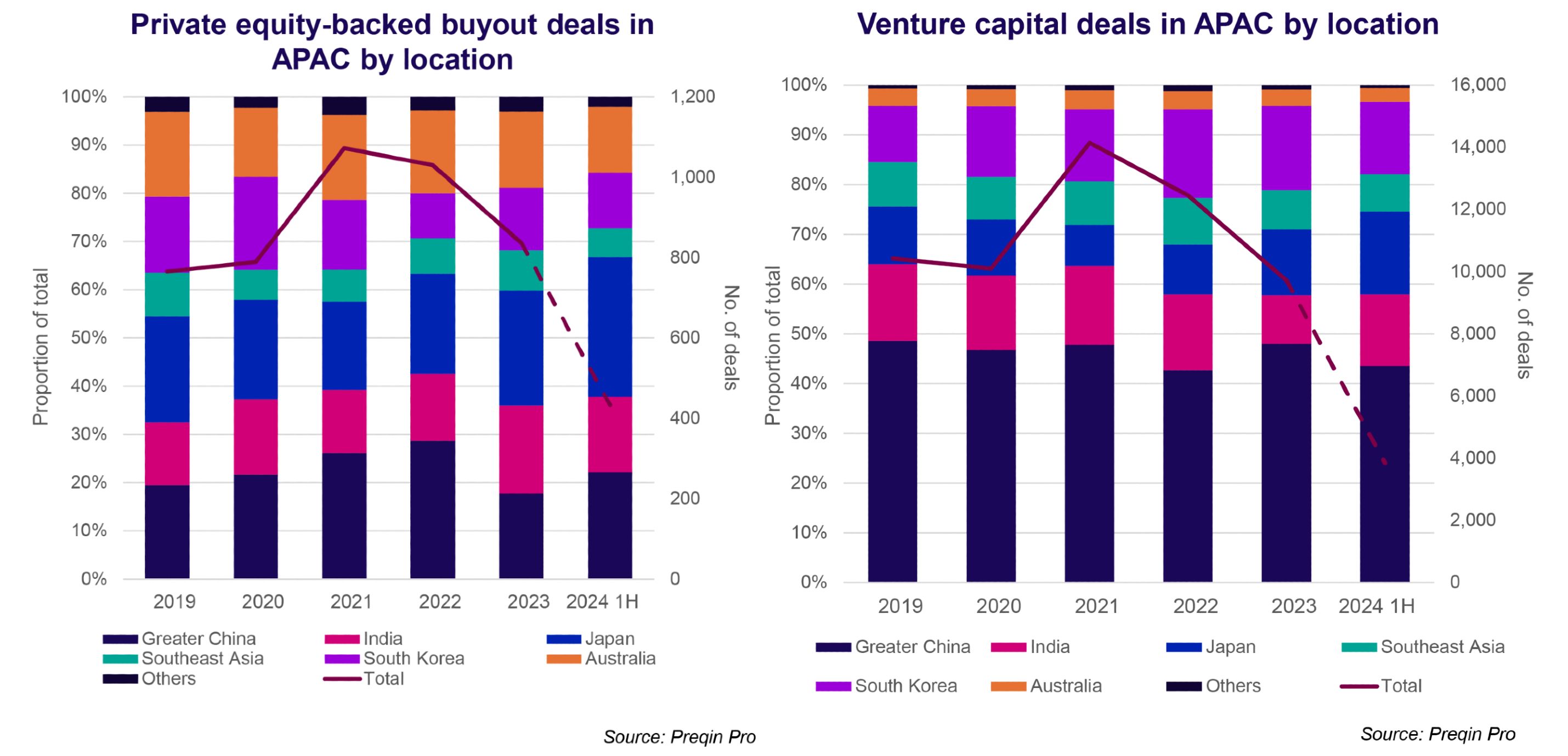

Private equity, venture capital

Private equity dominates fundraising activities in Japan, which has defied the softer investor sentiment seen in most major private capital markets since 2022. It surpassed Greater China as the most active private equity market in Asia, cornering most of the buyout deals in the space since 2023.

“There might be two reasons that non-Japanese investors will be looking at private capital activities in Japan. One is for market reasons, and the other is general partners’ attitudes,” says Nobuyuki Inomata, head of fund investment team, alternative investment solution department, at Nomura Asset Management.

Inomata mentions four market reasons, one being the active flows of buyout and private equity investment into the Japanese market. Another reason is the low interest rate. Although the Bank of Japan recently raised interest rates by 15 basis points to 0.25%, the borrowing costs remain much lower in Japan than in other global markets. As a result, Japanese GPs use loans to structure their buyout investments.

The third reason is the weak Japanese yen, which translates to lower investment costs for foreign investors. The fourth reason is geopolitical as some of the investments have shifted from China to Japan.

According to Inomata, more Japanese GPs are inviting non-Japanese limited partners (LPs) into their funds, which are getting bigger, as local investors may not be sufficient to meet the demand.

China still dominates the Asia-Pacific venture capital market in terms of volume, although Japan has been relatively resilient in the last two years. The Japanese market poses some challenges for foreign investors, such as language barriers and different accounting standards, which is probably why domestic investors dominate the market. South Korea and India are also significant players in the space.

Private capital funds in Japan have generated a median net internal rate of return of over 20%, the highest in the region, while also having a relatively moderate risk profile, according to Preqin data.

Private debt

Assets under management (AUM) in the APAC private debt market have doubled over the past five years. While the majority of the assets are managed by pan-Asia funds, which have the flexibility to allocate across the region, India has seen the fastest growth and is the largest single country-focused private debt market in the region in terms of AUM.

“Even with this growth, APAC is still a relatively small part of the global private debt market, and the AUM is only around 7% for now, as banks still dominate lending,” says Angela Lai, vice president, head of APAC and valuations, research insights, at Preqin.

In the next 12 months, global investors are most likely to increase their private debt allocations, with the IRR in the region higher than in the US and Europe, according to Preqin’s 2023-2028 performance forecast.

“Venture debt was probably more favoured historically, but direct lending, and better-performing credit for corporates, is really starting to grow, but it is still early stages, which is why you're not seeing the huge capital swings come in just yet. Depending on how you look at it, private credit is probably less than 1% across all the different types of debt that are out there. Asia arguably has the most opportunities out of any region globally, and there's also obviously less competition,” says Peter Graf, partner, head of financial sponsor lending Asia, at Ares Management.