Commercial property sales in Asia-Pacific declined 13% to US$31.3 billion in the first quarter of 2024, compared with a year ago, weighed down by the high interest rate environment and a retreat from apartment, office and seniors housing deal activities, a new report finds.

The pace of decline was steeper than one quarter ago, but still slower than in the previous five quarters, according to the latest Asia-Pacific Capital Trends report from MSCI Real Assets.

Japan was one of the bright spots, with a recovery in office investment and strong acquisition momentum for other sectors indicating that recent tweaks to the Bank of Japan’s interest rate policy have had little impact on investor sentiment.

“While Japan has been the standout market for some time, Asia-Pacific’s resilience across both deal activity and performance returns extends to other markets as well,” says Benjamin Chow, head of real assets research for Asia at MSCI.

“Activity is stabilizing for many major markets, while returns in 2023 were still positive for many sectors despite the high interest rate environment. Initial signs in 2024 so far point to investors continuing to focus on growth areas like data centres and emerging living sectors.”

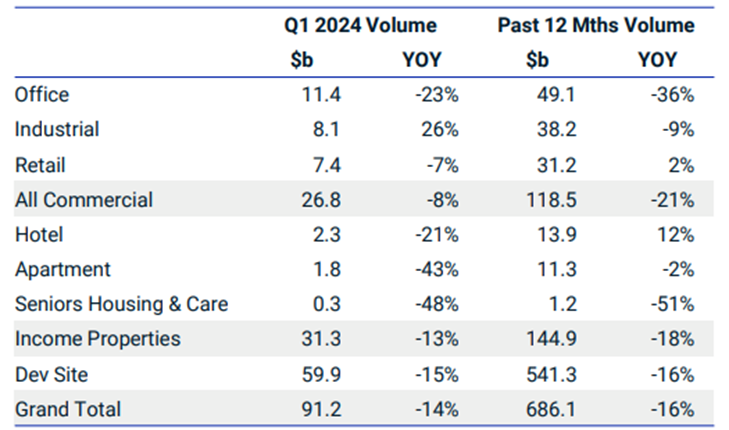

Investment volume by sector

Source: MSCI Real Assets

Source: MSCI Real Assets

Strong appetite for data centres

Interest in growth sectors across Asia-Pacific remained strong, with acquisitions of standing data centre assets totalling more than US$1.6 billion in the first quarter alone, surpassing both the first and second halves of 2023. Activity in the sector was being fuelled by a rising appetite for assets powering the digital economy.

Another bright spot for the region amid the sluggish dealmaking environment is the retail sector. Following several quarters of subdued activity, appetite for retail has started to pick up in recent quarters. This points to a trend of investors seeking value in the sector that has seen the most substantial repricing in the region.

Retail deal activity ended the quarter at US$7.4 billion of deals, which accounted for nearly a quarter of total commercial real estate sales in the quarter – the highest proportion that the sector has notched for any single quarter over the past five years.

Office volume continued its decline across most of Asia-Pacific, falling more than 20% from the first three months of last year, MSCI says. This was the only sector where deal activity over the past 12 months remains significantly lower than the prior periods, dragged down by muted activity in markets like Singapore, Hong Kong and Osaka.

While acquisitions of apartments fell by over 40%, investors continued to gain exposure to the sector through conversions of hotel properties. In addition to Singapore, this trend was noticed in several other markets.

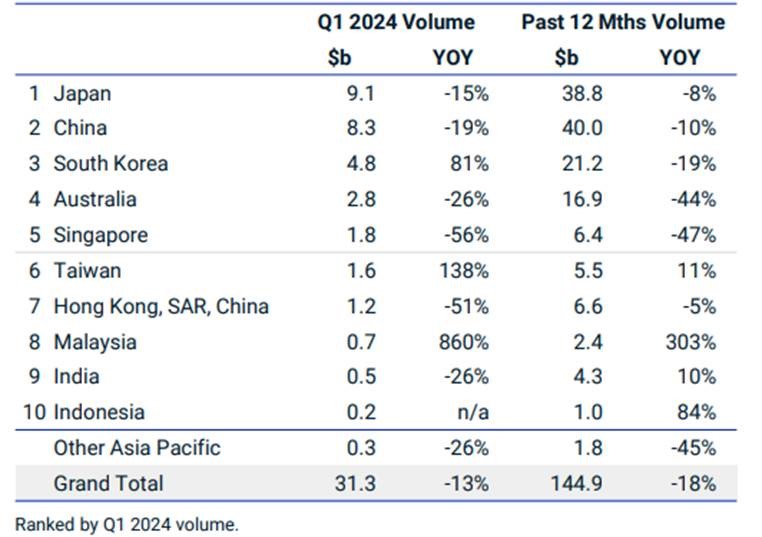

Investment volume by market

Source: MSCI Real Assets

Source: MSCI Real Assets

China market still active

Activity in China’s commercial real estate sector slowed 19% from the Q1 2023 tally, but it remained the biggest market over the past 12 months, with US$40 billion of assets traded, the report says.

There were strong year-over-year gains in volume for both industrial and retail, while the office sector continued to languish. The rental apartment sector continued to feature, with the sale of a 1,000-unit project. Investment in Shanghai offices fell by almost two-thirds, putting its office market behind Beijing in the first quarter. Shanghai did take the crown for the biggest retail market, with almost US$900 million of deal volume.

Looking ahead, several signs suggest the trend of declining investment activity is nearing the bottom. The deal pipeline – the stock of outstanding deals where a contract has been signed but has yet to be completed – has remained relatively stable over the past few quarters, MSCI says.

In addition, yield expansion has started to taper off for key institutionally focused sectors, such as Korean and Australian offices, as well as Australian warehouses.

Nearing the bottom, however, does not imply an imminent recovery, according to the report. For most markets outside of Japan and China, yield spreads to borrowing costs remain thin or even negative. Many deals that could have generated sizable returns prior to 2022 would no longer be as attractive under current debt costs.

“A lot still rides on the timing and magnitude of US-led interest rate cuts, and in recent weeks the question has become whether these will even happen. It is clear though, that this trough is likely to be a bumpy one,” the report says.