With inflation cooling down and prospects improving for interest rate cuts in the medium term, US equities and fixed income are providing more opportunities for investors in the year ahead.

Although the US Federal Reserve Board did not cut interest rates, and made it clear that it was not ready to do so, at its policy meeting on January 30-31, the outlook for fixed income looks far better as inflation has moderated significantly even if it remains above the Fed’s target level.

Following its meeting, the Federal Open Market Committee, which sets the Fed's policy rate, issued a statement saying it has no plans to cut interest rates while inflation is still above the target of 2%. However, it removed language that indicated a willingness to keep on raising interest rates until inflation had been brought under control. In its last meeting in December, the Fed adopted a dovish posture, projecting 75 basis points of rate cuts in 2024.

Meantime, personal consumption expenditure (PCE) data for December, released last Friday, supported the Fed’s stance, with headline and core PCE (which excludes volatile food and energy components and is the Fed’s preferred inflation barometer) meeting expectations, according to Saira Malik, chief investment officer of Nuveen Global Investments.

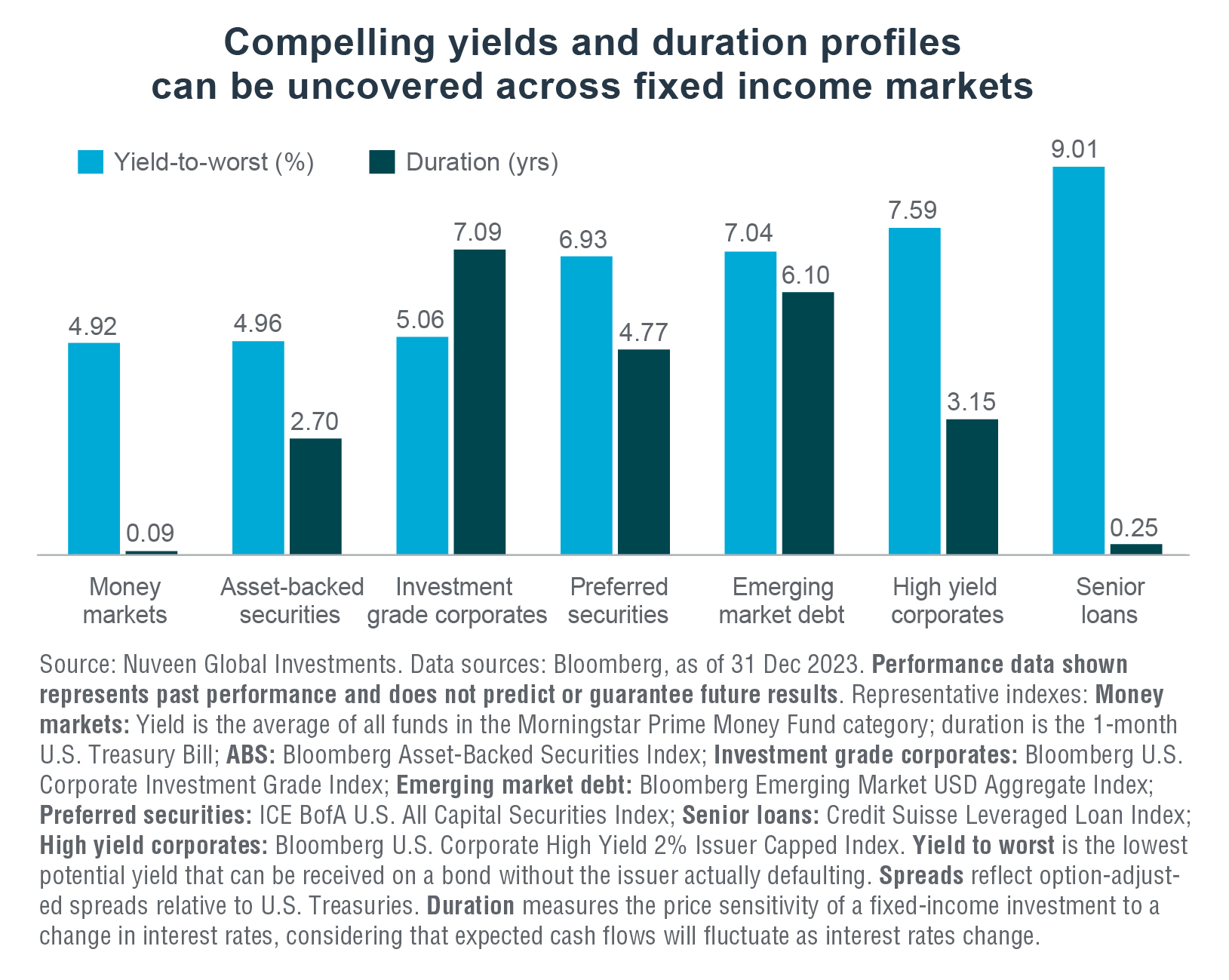

“We believe the recent increase in bond yields has created ample opportunity for investors to benefit from what should be several rate cuts this year (beginning later than markets expect). Our outlook calls for the 10-year US treasury yield to fall from current levels to finish 2024 around 3.50%,” Malik says. “In some investment-grade sectors, yields are now north of 5%. This higher-yield environment is driving greater dispersion and creating more opportunities to capture attractive returns.”

Longer duration profile

Investors are advised to extend duration in fixed-income portfolios but stay nimble and flexible when investing in the credit sector.

“Investment-grade corporate bonds, for instance, offer a longer duration profile, and their higher relative quality could provide a cushion if the economy weakens more than we expect,” she says.

In equities, the major US indices hit another record high on Monday (January 29) with the S&P500 trading up to 4,930 for the first time, driven higher by falling US yields.

The overall positive sentiment for US markets has prompted the BlackRock Investment Institute (BII) to upgrade its outlook for US stocks to overweight in 2024 from neutral in 2023, in its weekly commentary issued on Monday.

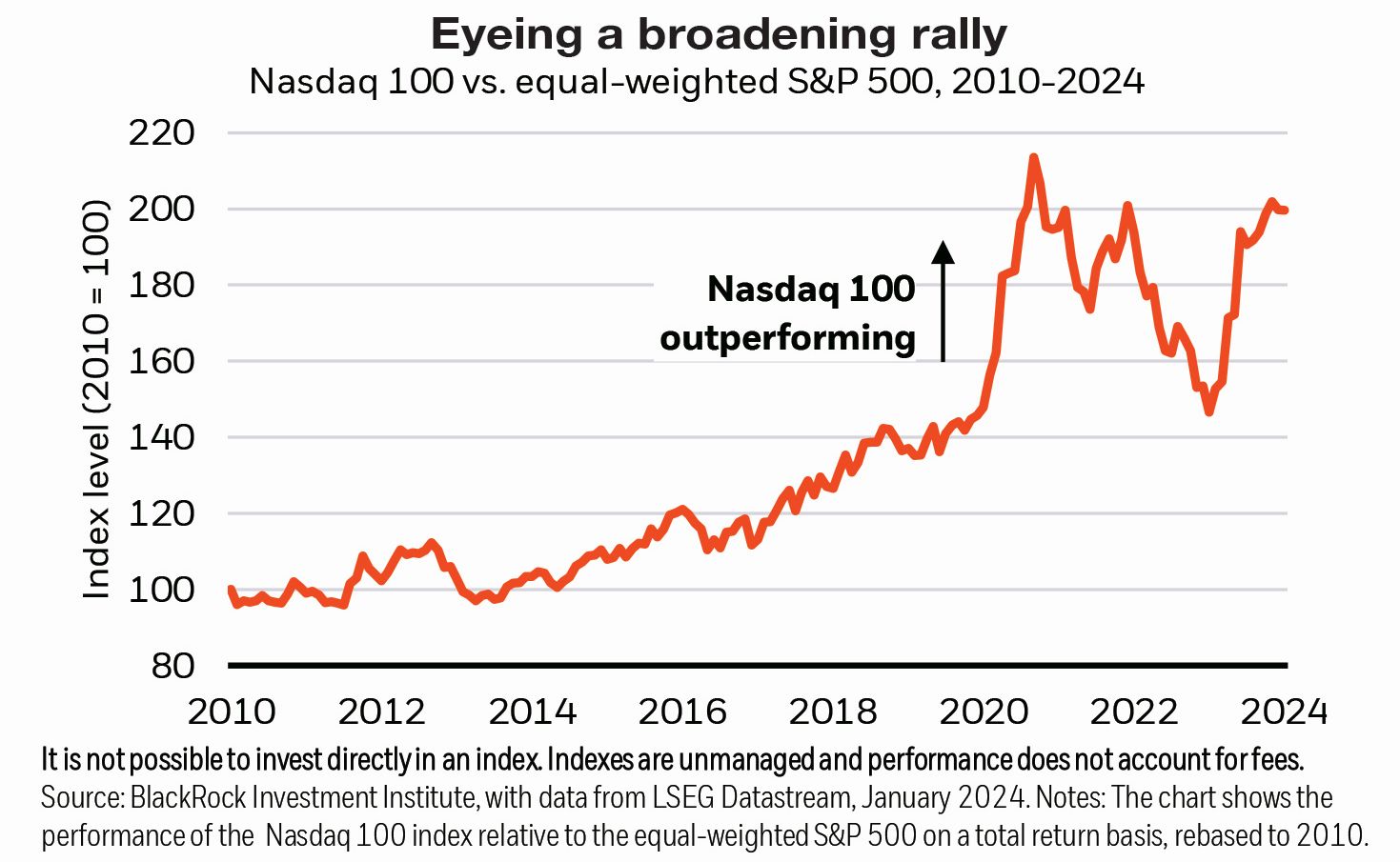

“We think stock momentum can run for now as inflation cools and the Federal Reserve readies to cut rates,” according to BII. “So, we up our overall US stocks view to overweight. Excitement over artificial intelligence (AI) spurred a rally in US tech stocks that buoyed the market in 2023. We’ve said the rally can run for now and broaden out.”

In mid-2023, BII shifted how it presented its tactical views to capture opportunities from mega forces or big structural forces, referring to how the big technology stocks, known as the Magnificent Seven (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) had collectively risen nearly 117%, far outpacing the performance of the other 493 companies in the S&P 500.

“Our overall US equity view was neutral (in 2023), consisting of an underweight at the benchmark level and an overweight to the AI theme. That selectivity has been rewarded in the past 12 months, with tech pushing US stocks to all-time highs,” according to BII.

Sustained revenue growth

In 2024, with inflation expected to approach the Fed’s 2% target and interest rate cuts looming, BII has upgraded its outlook for broad US stocks, its index level view plus AI theme preference, to overweight on a tactical horizon of six to 12 months.

Outside the United States, the outlook for corporate earnings within emerging markets remains fairly constructive and it is expected that there will be sustained revenue growth and margins at the corporate level, according to Leonard Kwan, portfolio manager of the dynamic emerging markets bond strategy at T. Rowe Price.

“Real incomes are also expected to improve, along with resilient labour markets and rising wealth effects that should continue to drive consumption, particularly in the first half of 2024. Emerging markets fixed income has been resilient thus far in this cycle of higher core rates. We think the asset class may offer strong income potential given attractive yields and the prospect for lower interest rates,” says Kwan.