Fixed income investors still consider rising inflation as the biggest risk to their asset class amid data showing that inflation remains at levels higher than where the US Federal Reserve wants it to be.

Although inflation rates slowed down in March 2023 following a series of interest rate hikes since last year, fixed income and private debt investors fear that the prolonged period of high interest rates aimed at taming rising prices is weighing down on company earnings that underlie these asset classes.

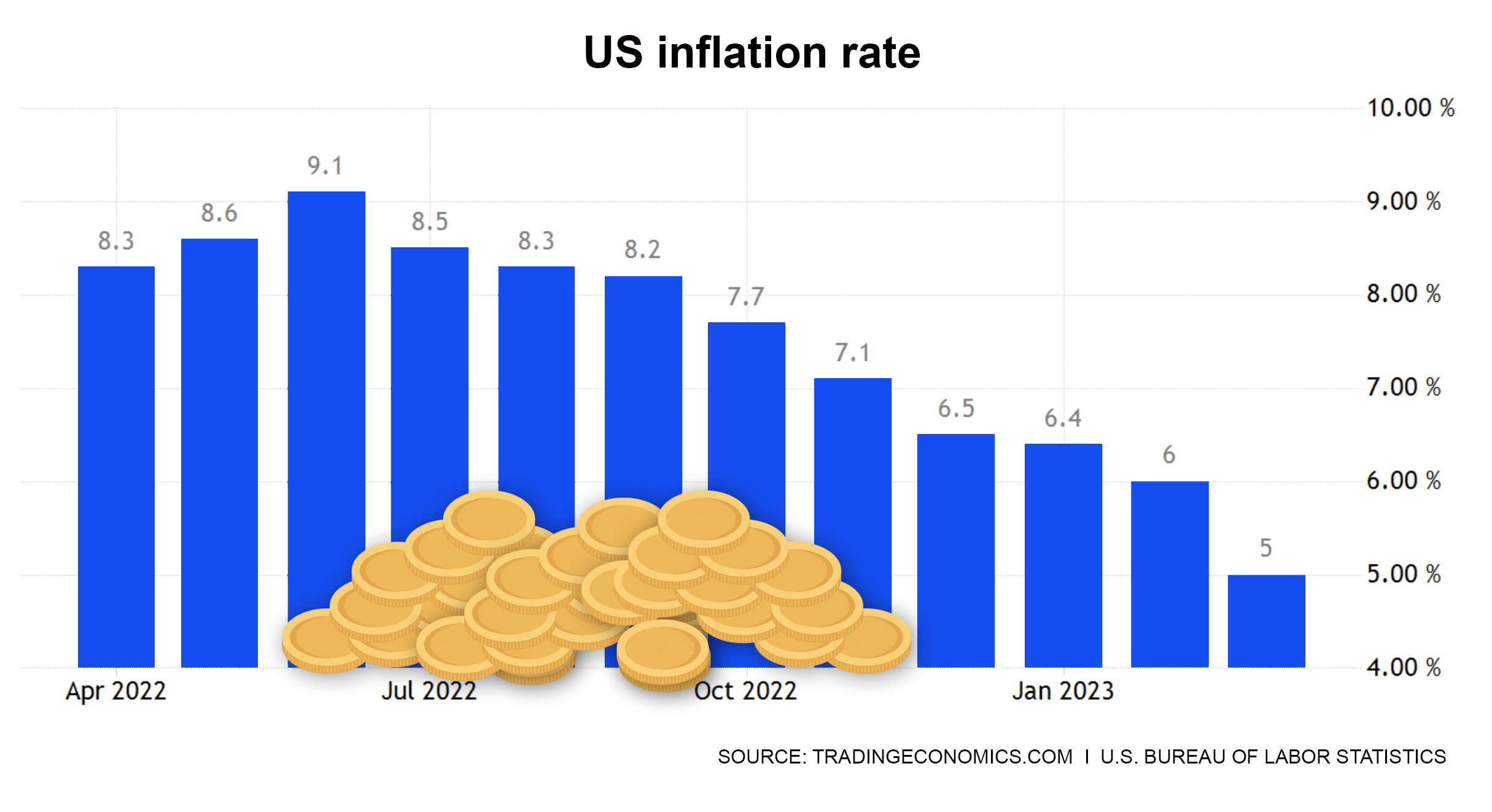

The US inflation rate slowed for the ninth consecutive month to 5% in March 2023, the lowest since May 2021 and below market forecasts of 5.2%. Fed chairman Jerome Powell has insisted that the central bank aims to reduce inflation to 2% but declines to give a specific time period.

On the bright side, fixed income markets are considered to be more resilient, and should hold up much better than equities in a rising inflation rate environment.

“Relative to equity markets, the fixed income markets should hold up much better, investment grade should hold up much better than high yield even as company earnings are coming under some pressure,” says a fixed income portfolio manager for a global fund house.

Debt profile

In terms of the macro landscape, an inflationary environment may benefit borrowers who have fixed interest rate debts because they can pay off these debts and get their earnings in nominal dollar terms. This means that inflation can reduce some of their debt profile.

However, the resilience of fixed income markets may be tested by the so-called maturity wall, which is when billions of dollars’ worth of bonds are expected to mature within the next two to three years and have to be refinanced.

In Europe, for example, companies with loans outstanding in the Morningstar European Leveraged Loan Index (ELLI) faced nearly €72 billion (US$79 billion) of debt coming due within the next three years, and nearly €27 billion in the next two years, the highest figures for five years.

In China, property developers are also facing growing pressure on debt repayment as 958 billion yuan (US$141 billion) of onshore and offshore bonds come due by the end of 2023, 70 billion yuan more than in 2022.

However, bond issuance hit record levels in 2021 and 2022, even in January this year, with significant amounts of new issuance in the investment-grade bond market, as well as, tactical issuance happening in the high-yield bond market.

“Generally, if you're looking at the maturity wall near-term, there's not that risk. But the longer that inflation and interest rates remain higher eventually, companies will have to refinance,” the portfolio manager says.

Growing pressure

Because of this, there is concern among fixed income investors that there will be increasing pressure on corporates and potentially more bond defaults unless the capital markets open up sufficiently in the next 18 months.

At the same time, the inflation risk has been exacerbated by the banking crisis in the US, which threatens to impose an immediate and long-lasting economic drag from reduced bank lending and the associated hit to sentiment.

“That’s what we need to keep an eye out for, how long and how sustained amount of time will be that the capital markets will come under pressure and does that eventually cause a very hard landing for the global economy,” says the portfolio manager.

Some asset managers, particularly PGIM Fixed Income, have already raised the probability of a recession in the US from 30% to 40%, and the odds of stagflation from 5% to 15%, owing to the possibility that the Fed may have to prematurely pause its rate hike cycle to prevent further financial instability.

“Consistent with these adjustments, the shock has reduced the likelihood of a soft landing,” says Daleep Singh, chief global economist, head of global macroeconomic research, at PGIM Fixed Income. “As such, the March hike to an upper bound of 5% likely marked the end of the Fed's tightening cycle, and the credit crunch that is already brewing will likely cause economic contraction in the second half of the year, forcing the Fed to make 50bp to 75bp of rate cuts in Q4.”