While facing short-term financial burdens and transition risks, China’s corporations can reap long-term benefits from the country’s well-rounded green transition policy framework, which has been updated several times this year with new measures covering various issues, among them, carbon emission trading; environmental, social and governance (ESG) and climate information disclosure; and green transition finance, according to a recent report.

China’s push for economic transition and decarbonization at the national level brings profound implications for the outlook of its industries, finds the report by Moody’s Ratings. The first is that the property sector’s role will diminish, which will be a drag on China’s economic performance. China’s GDP amid the weakening property market, Moody’s expects, will grow by 4.5% for 2024, lower than the official target of 5%.

In the meantime, a bourgeoning green industry dominated by new energy vehicles (NEVs) will bring in new growth opportunities, offsetting some of the negativities from the slowdown of the property market. The share of NEVs and their related sectors in its nominal GDP, the report predicts, will reach 4.5% by the end of this decade, tripling from the 2023 level of 1.5%.

.jpg)

Finally, carbon-intensive sectors, such as aluminium and steelmaking, are facing mounting pressure – partly from strengthened regulations in both domestic and overseas markets around carbon emission reduction and the green transition, but also from the property sector’s reduced demand.

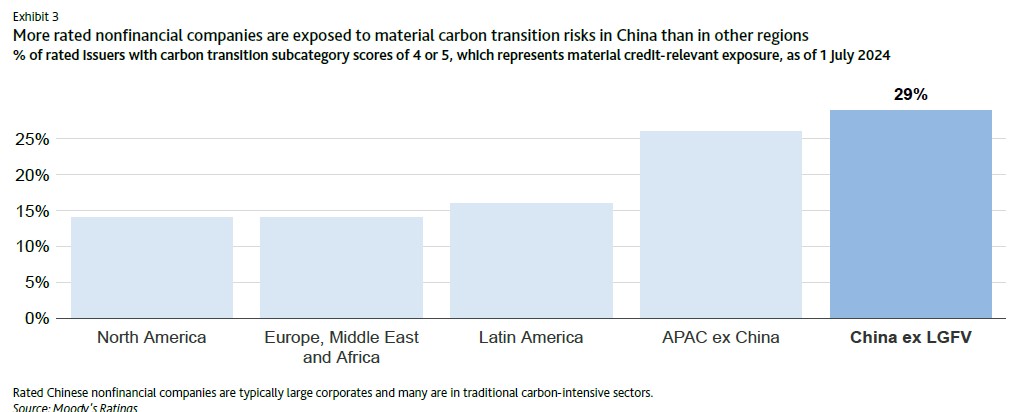

Given these risk factors, 29% of its rated Chinese non-financial companies, excluding local government financing vehicles, the report finds, are exposed to material carbon transition risks, which is higher than other parts of the world.

Nevertheless, China’s overall policy design towards decarbonization aims at alleviating some of the transition risks faced by companies and empowering them in their green transition journey.

Carbon emission trading

A key part of China’s decarbonization roadmap is to build an effective carbon emission trading market. China’s existing national carbon emission trading system (ETS) was launched in 2021 and currently only covers the power generation sector.

In the first half of 2024, the government has proposed to include electrolytic aluminium and cement into the national ETS to cover more carbon emissions and further develop the market. The two sectors, according to data from their relevant industry associations, respectively account for 5% and 10% of China’s total carbon emissions.

Being included in the national ETS creates an incentivizing mechanism for companies to reduce their carbon emissions and save expenses in carbon trading by upgrading their production technologies and rearranging supply chains.

While this creates extra financial burden and other transition risks for electrolytic aluminium and cement companies in the short run, the report predicts that inclusion will pay off in the long run. For example, inclusion in the ETS could help China’s aluminium makers mitigate the impact of eroding competitiveness in the EU market by encouraging reductions in carbon emissions from production and potentially avoiding carbon tariffs in the future if carbon prices reach similar levels to those in the EU.

Additionally, inclusion in the system is also to the benefit of large companies with stronger financial and technological capabilities and will thus eliminate the more inefficient and high-polluting players.

Enhanced disclosure

Another enabler in China’s decarbonization policy design is to increase the transparency of companies’ disclosure of ESG and climate-related information. China’s major stock exchanges are announcing new sustainability disclosure guidelines for their listed companies, which will make climate disclosure a mandatory issue.

Similar to the expansion of the national ETS, the new regulation, the report estimates, will increase Chinese corporates’ administrative costs in the near term, but it will increase their sustainability performance in the domestic as well as the international capital market in the longer term by combating greenwashing and increasing investor confidence.

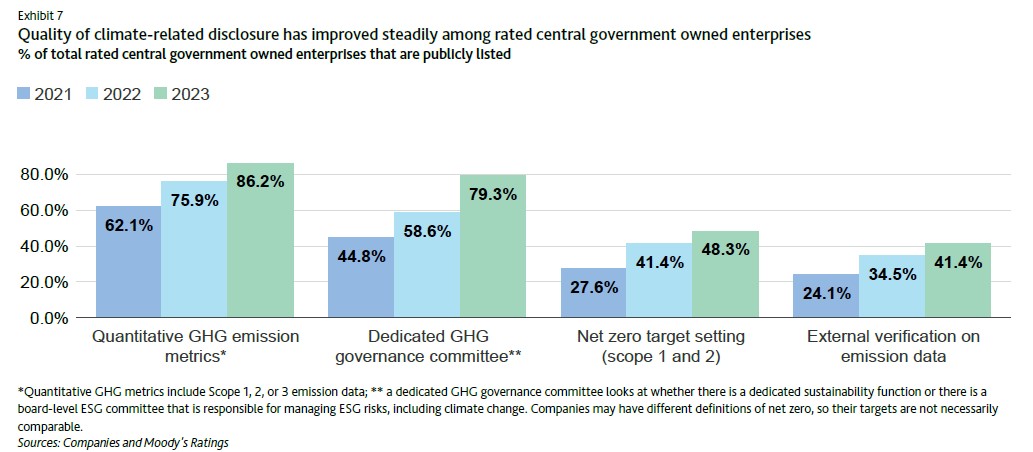

China’s central government-owned enterprises, the report notes, have improved the quality of their climate-related reporting since 2021.

Financing channels

Last but not least, China is considering tapping the transition finance market to expand green financing channels for its hard-to-abate sectors. The country’s current sustainable bond market is dominated by labelled green bonds, which are project based and inaccessible to companies in the hard-to-abate sectors.

To hasten the green transition, more companies in these hard-to-abate sectors must be included into the sustainable bond market, and a key enabler is the launch of transition finance solutions.

At present, Japan is Asia’s transition finance leader with its issuance of sovereign transition bonds; and, in China, some municipal and provincial governments, including those of Huzhou and Hebei, are piloting carbon transition financing programmes.

China’s national authorities, the report predicts, will roll out a specific transition taxonomy with definitions of transition activities, guidelines for the disclosure of the use of proceeds and progress in transition projects, rules for transition financing products, and incentive schemes.