Welcome back! This is the final article in our three-part series on “ESG take-up in the spotlight”, based on findings from an in-depth survey with CEOs, CFOs, CSOs, Treasury professionals and experts from BNP Paribas sharing their voices and insights on the latest trends in ESG strategy and market developments in sustainable finance. For those who missed the previous articles, you can find them here (Part 1) and here (Part 2).

In the second section of our analysis as part of a three-part research series, we highlighted various challenges faced by companies and leadership teams in the implementation of ESG strategy. In this final section we explore the solutions.

Sustainable finance is an integral part of the C-suite toolkit, a necessity to help accelerate the integration of ESG strategy within an organisation, both across functions and regions, and create long-term value which addresses key sustainability challenges. However, the market for sustainable finance is still developing, and according to the research, many companies do not understand how sustainable finance can be further integrated within their organisations. The survey has captured the following trends in sustainable finance:

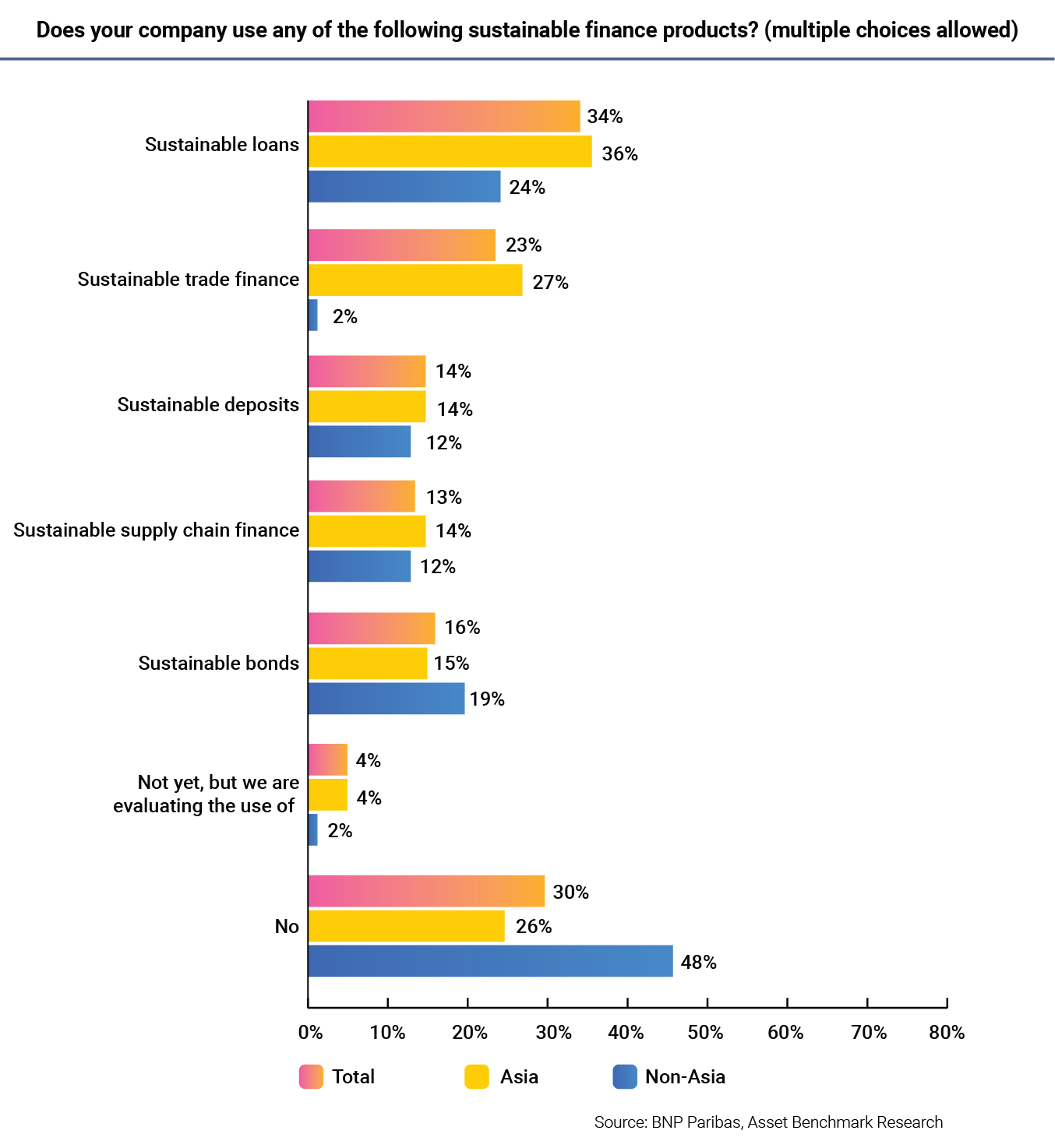

Two-thirds of surveyed companies are using a variety of sustainable financing solutions, including sustainable loans, bonds and trade finance, to support their funding needs. This suggests the use of sustainable finance has increased. Interestingly, the proportion of Asia-based companies using sustainable finance products (except bonds) is greater than that for companies outside of Asia.

This is perhaps because the needs and opportunities for transition finance are more prevalent in Asia than elsewhere. “Asia is a great place for innovation, especially in the space of digital technologies and inclusive finance with EDMEs (emerging and developing market economies) needing both expertise and capital for climate mitigation and adaptation,” shares Eric Tran, Head of Sustainability, Transaction Banking APAC, at BNP Paribas. He explains the other reason is that the definition and threshold for sustainable finance may also be different between Asia and non-Asia corporates.

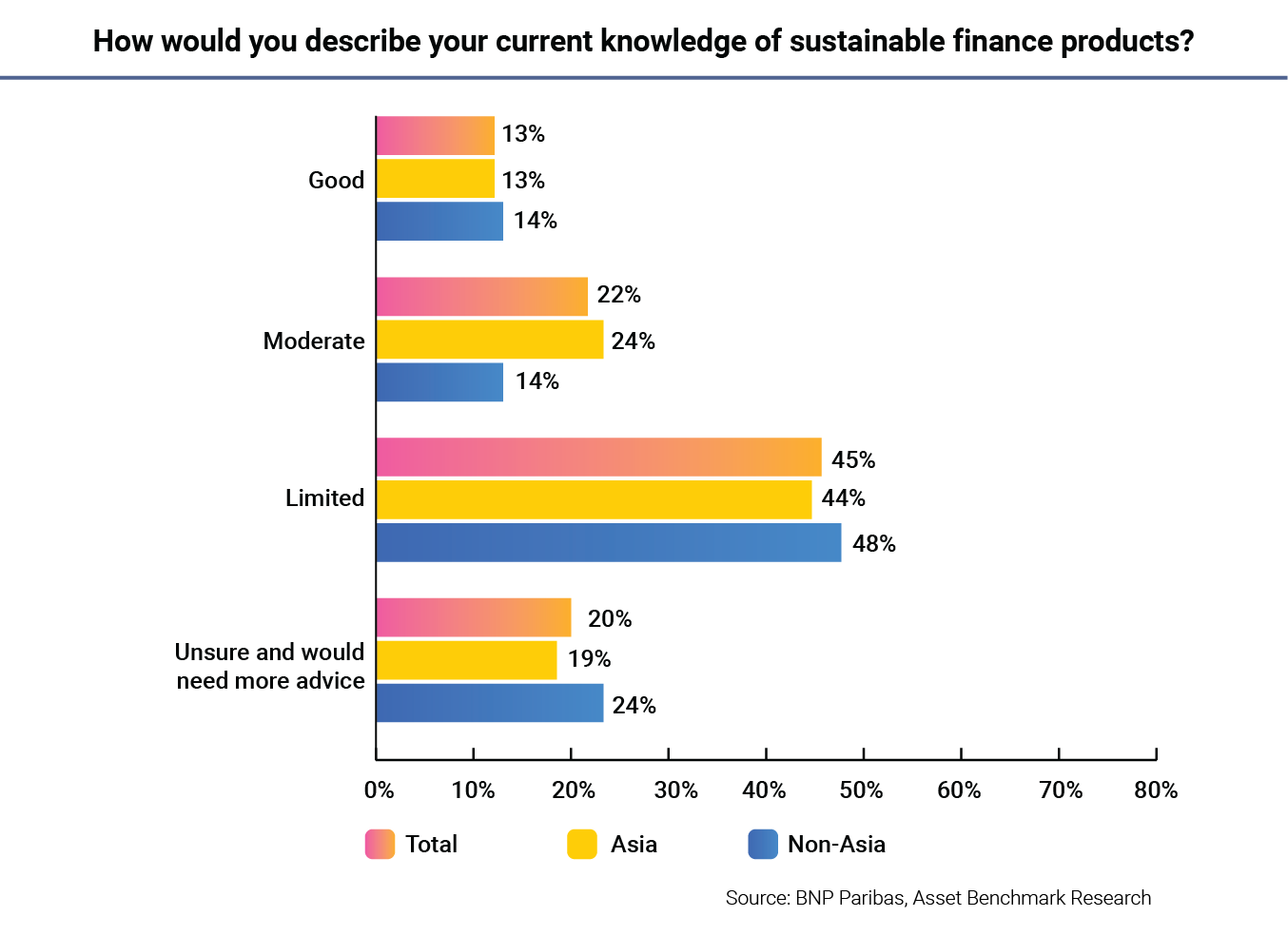

The survey also highlights some gaps in terms of the overall understanding of sustainable finance. Notably, 45% of respondents say their knowledge about such products is “limited”, 22% describe their proficiency level as “moderate”, and only 13% are confident enough to say that they have a “good” understanding of these sustainable finance products.

This insufficient level of understanding about sustainable finance products partly explains the trend noted earlier in this report – that only a small proportion (20%) of companies are able to put ESG considerations into financial decision-making and other strategic considerations in a consistent manner.

This trend also suggests that companies need greater support from external advisers on ESG strategy and sustainable finance. With their expertise in fund mobilisation, risk management and anticipation of regulatory trends, banks have the opportunity to act as trusted partners for companies creating sustainable finance and ESG-integrated strategy.

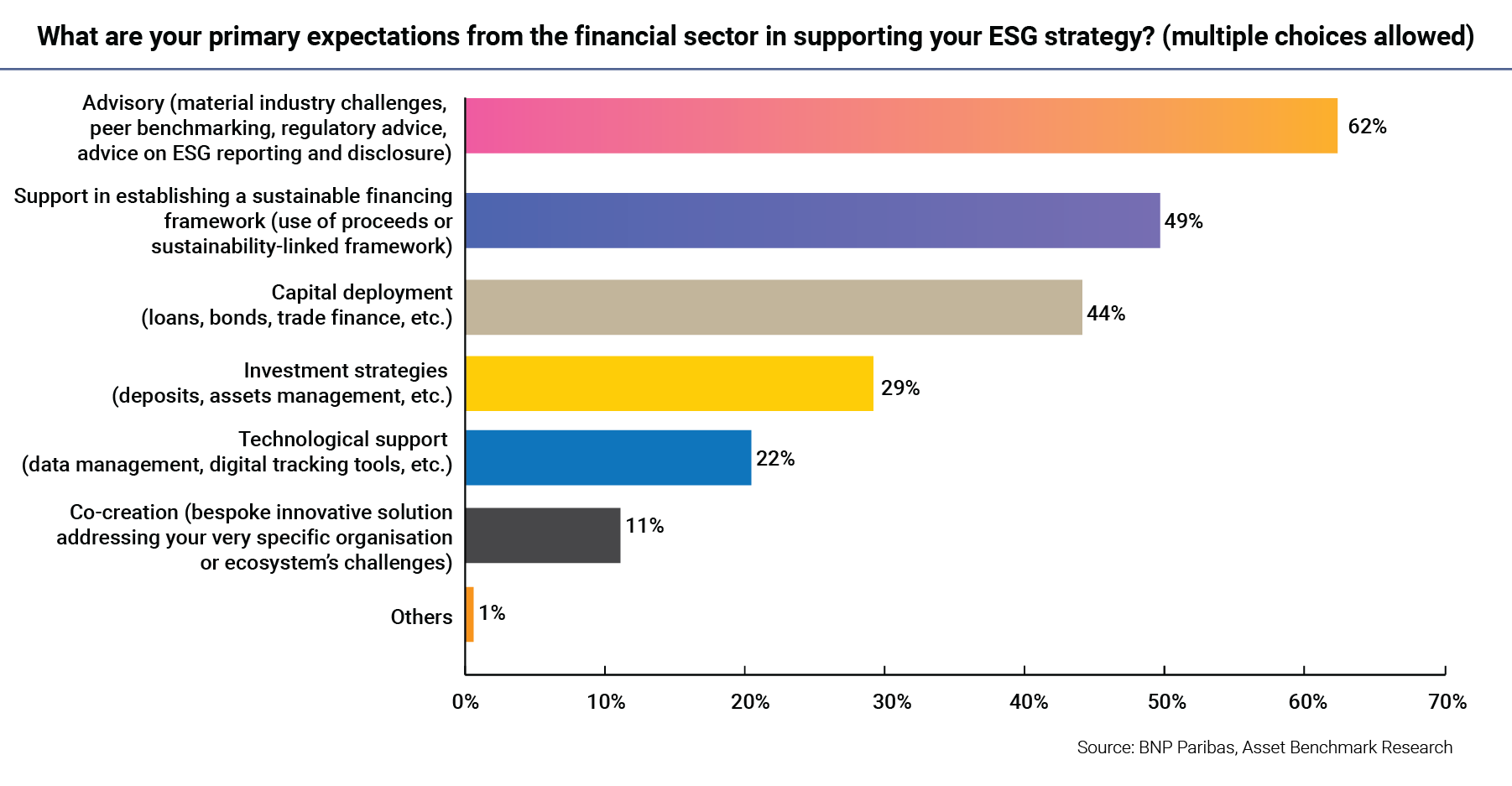

The survey confirms this need – 62% of respondents indicate they would like banks to provide them with advisory services like decoding ESG regulations, setting ESG benchmarks with industry peers, and formulating sustainable finance frameworks. And 22% of the respondents hope banks can provide them with technical support in ESG data tracking and management.

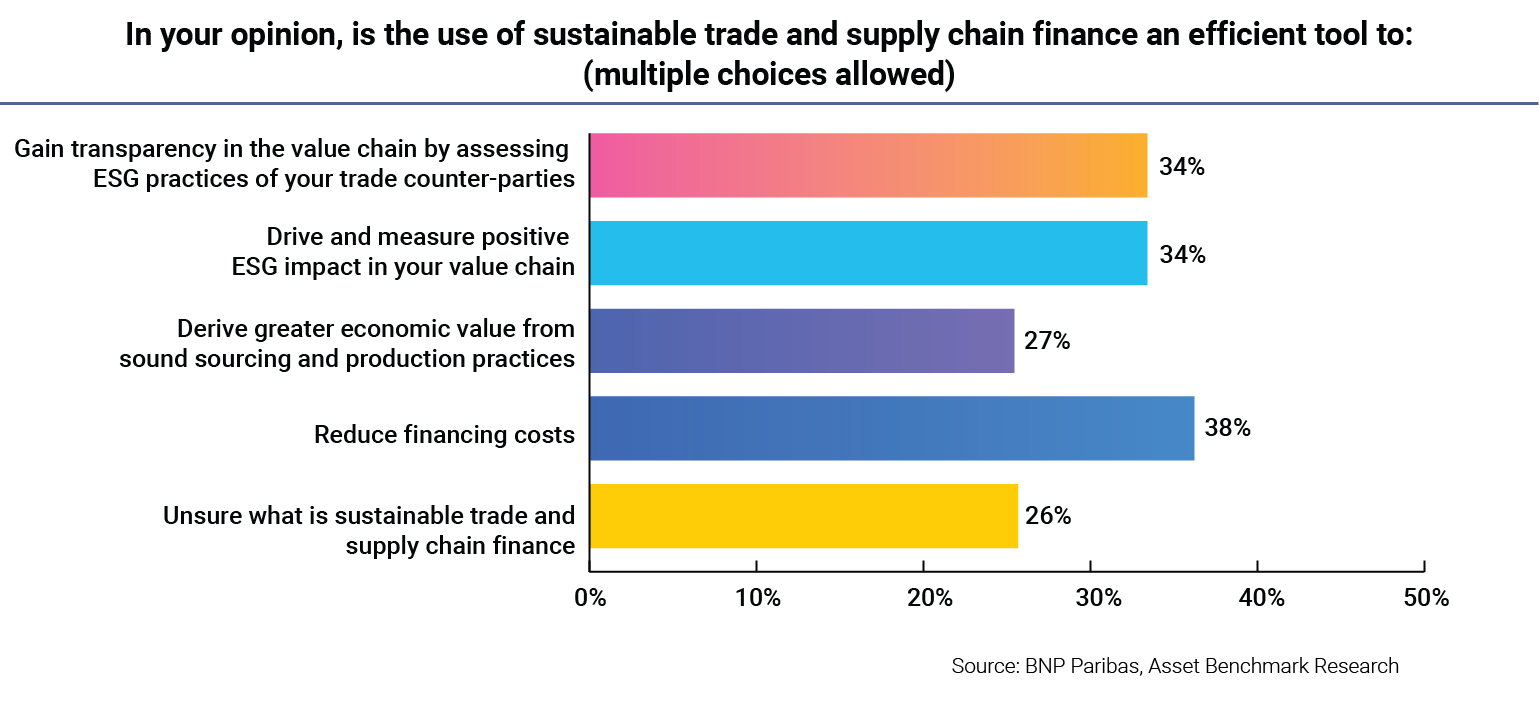

Companies also value the ability of banks to provide diversified, sustainable finance products. As the survey reveals, 34% of respondents believe sustainable trade and supply-chain finance are efficient tools to gain transparency in the value chain. And 27% of them believe these products can help them derive greater economic value from sound sourcing and production practices.

In one-on-one interviews, treasurers also indicated their increased take-up of sustainable finance solutions and their expectations for more of these solutions.

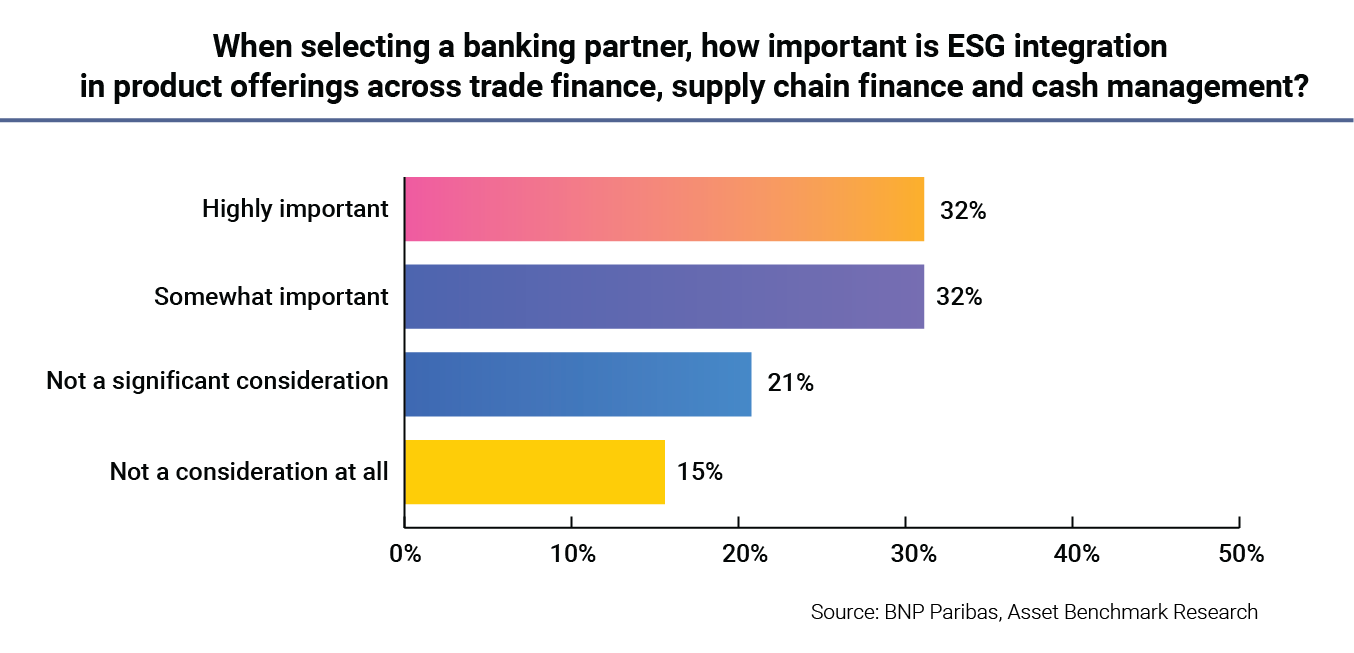

Finally, when selecting banking partners, two-thirds of survey respondents say that it is important for banks to embed ESG into their trade and supply-chain finance and cash management services. In other words, companies are more willing to work with banks that have strong ESG capabilities.

In response to this client demand, banks are also on the move to enhance their capabilities in delivering catered ESG solutions.

Since banks have dedicated resources on topics ranging from regulatory anticipation to low-carbon technologies, as well as a wide ecosystem composed of regulators, industry bodies, NGOs and ESG consulting firms, they play a critical role in guiding their clients through the ESG complexities.

On this matter, Tran shares how BNP Paribas is helping its clients to factor in sustainable finance into their operations. “For the past several years, we have been forming partnerships with leading innovative ESG solution providers to support the collection of ESG data across the value chain of our clients, helping them to set up KPIs [key performance indicators] and targets in line with their ESG material issues, and offering financing solutions to incentivise partners and lower the costs of capital for our clients,” he highlights.

Q: What are the key drivers for ESG & finance integration?

A: For CFOs and Treasurers, sustainability has become an imperative (from a regulatory, consumer and shareholders/investors standpoint) and an enabler (from a business perspective) as a differentiating factor and to widen access to capital.

There are positive developments across our clients’ organisations, including within the finance and treasury functions, given current climate urgency and regulatory pressures. We anticipate Treasury functions will play a larger role in climate-related disclosures, ESG risk management and alignment of the financing strategy with the ESG strategy.

The corporate CFO and the finance function both have expertise in financial planning, reporting, as well as investor relations. These skills and experience are well-suited to navigate regulatory frameworks and minimise ESG risks, secure funding for the companies’ sustainability initiatives and manage implementation of key ESG measures such as the internal carbon pricing across the company.

We are of the view that these efforts should be led by a company’s finance function. Sustainability performance (and the ability to manage non-financial information) has become inseparable from financial performance, making companies’ ability to act on ESG-related issues a key differentiator in achieving corporate success.

Conclusion

The survey responses, together with key insights from BNP Paribas, capture the latest ESG trends and outlook.

Firstly, ESG factors are increasingly being factored in by C-suite executives, and more resources are being invested in ESG strategy and sustainable finance. However, this is mainly being led by CEOs and CSOs, while CFOs and treasurers could exert greater influence within their organisations in this area.

Secondly, the pace at which companies develop their ESG strategy varies significantly, as can be seen in the survey statistics on ESG target-setting, GHG emission accounting and ESG-integrated decision-making.

Thirdly, companies face numerous challenges from both within and outside their organisations, including understanding the latest regulations. The lack of a clear ESG strategy, insufficient data availability and limited financial resources also hinder companies’ ambitions in implementing a clear ESG strategy. Companies are now realising these challenges and are actively seeking engagement with their industry peers and cooperating with banks to overcome these challenges.

Finally, sustainable finance is a powerful tool for advancing ESG strategies. However, companies’ understanding of sustainable finance is still at an early stage. CFOs and treasurers need more assistance from banks across various sustainability-related services. Banks should therefore seize the opportunity to forge a deeper relationship with their clients to deliver impactful ESG results.

Looking ahead, as the regulations become clearer, ESG data becomes more accessible and partnerships between corporates and banks start to consolidate, it is expected that CFOs and treasurers are increasingly set to play a significant role.

This is part of a series of articles on “ESG take-up in the spotlight”, based on a survey commissioned by BNP Paribas.

BNP Paribas and Asset Benchmark Research gathered feedback from over 200 CEOs, CFOs, CSOs and other senior managers from corporations around the globe on their views on ESG adoption and what they expected from their service providers to take their respective companies to the next level of sustainability development. To ensure a comprehensive understanding of their viewpoints, respondents were involved in one-on-one interviews and an online survey was conducted in the first half of 2024.

Appendix: Respondents’ profile

This appendix provides a brief statistical overview of respondents, including their geographical distribution, business turnover, industry sector and ownership type.

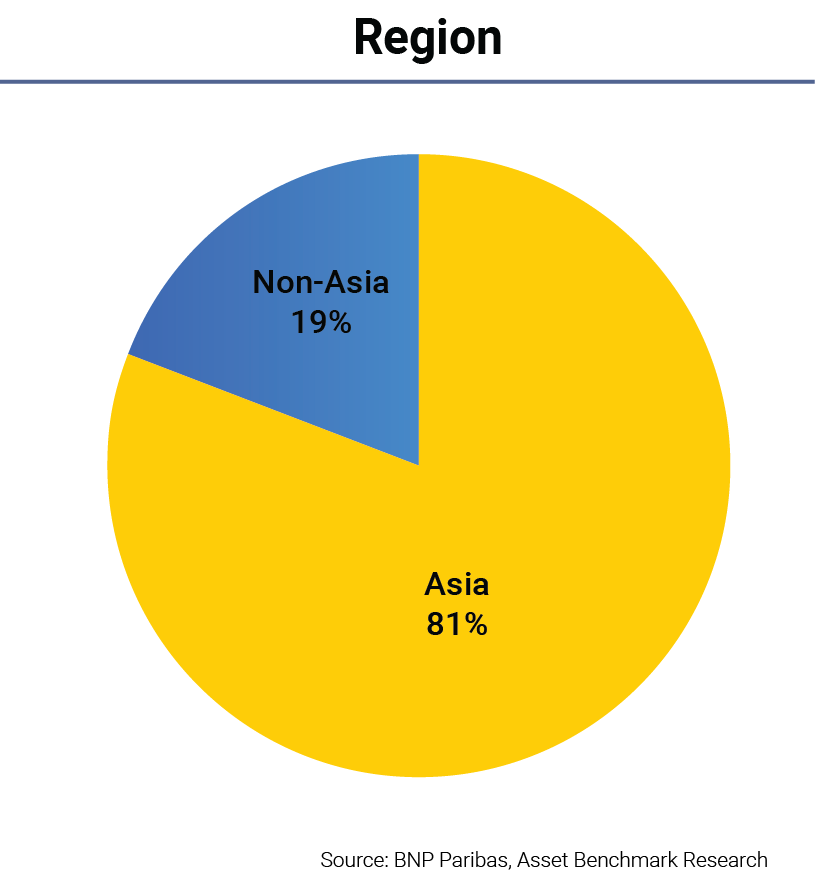

1. Regional distribution of respondents

The survey gathered feedback from over 200 CEOs, CFOs, CSOs and other senior managers from corporations across the globe, with the majority of them in Asia.

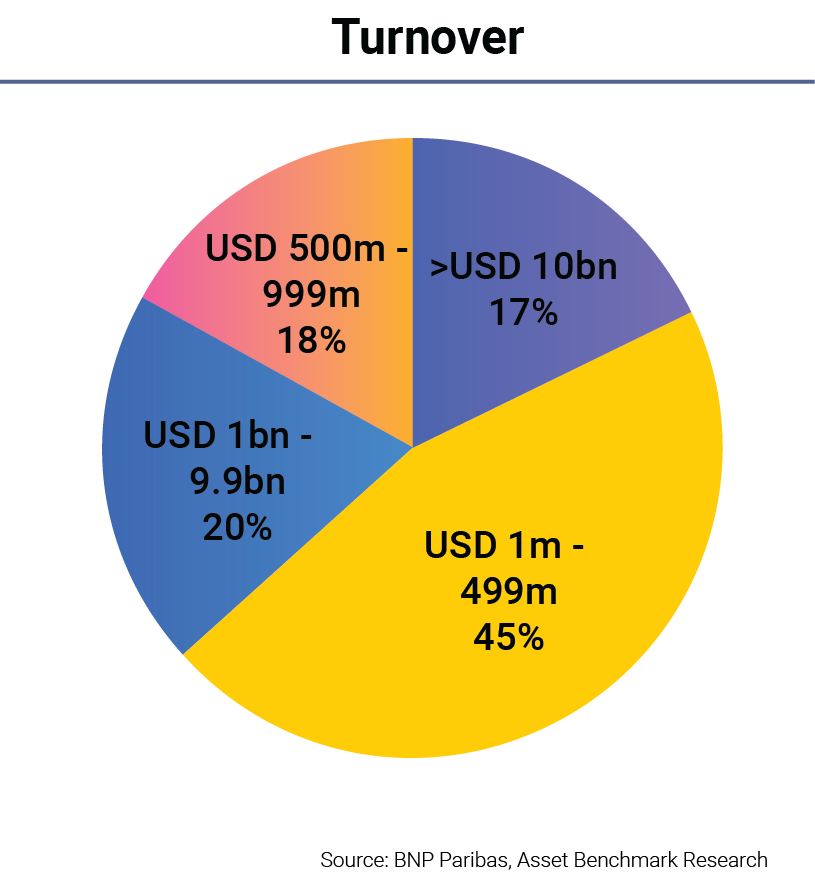

2. Business turnover breakdown of respondents

The majority of survey respondents (45%) are from companies with annual business turnovers of between US$1 million and US$499 million. The distribution for companies with annual business turnovers of over US$500 million (55%) is roughly balanced, with 18% of companies having turnovers of between US$500 million and US$999 million, 20% between US$1 billion and US9.9 billion and, finally, 17% above US$10 billion.

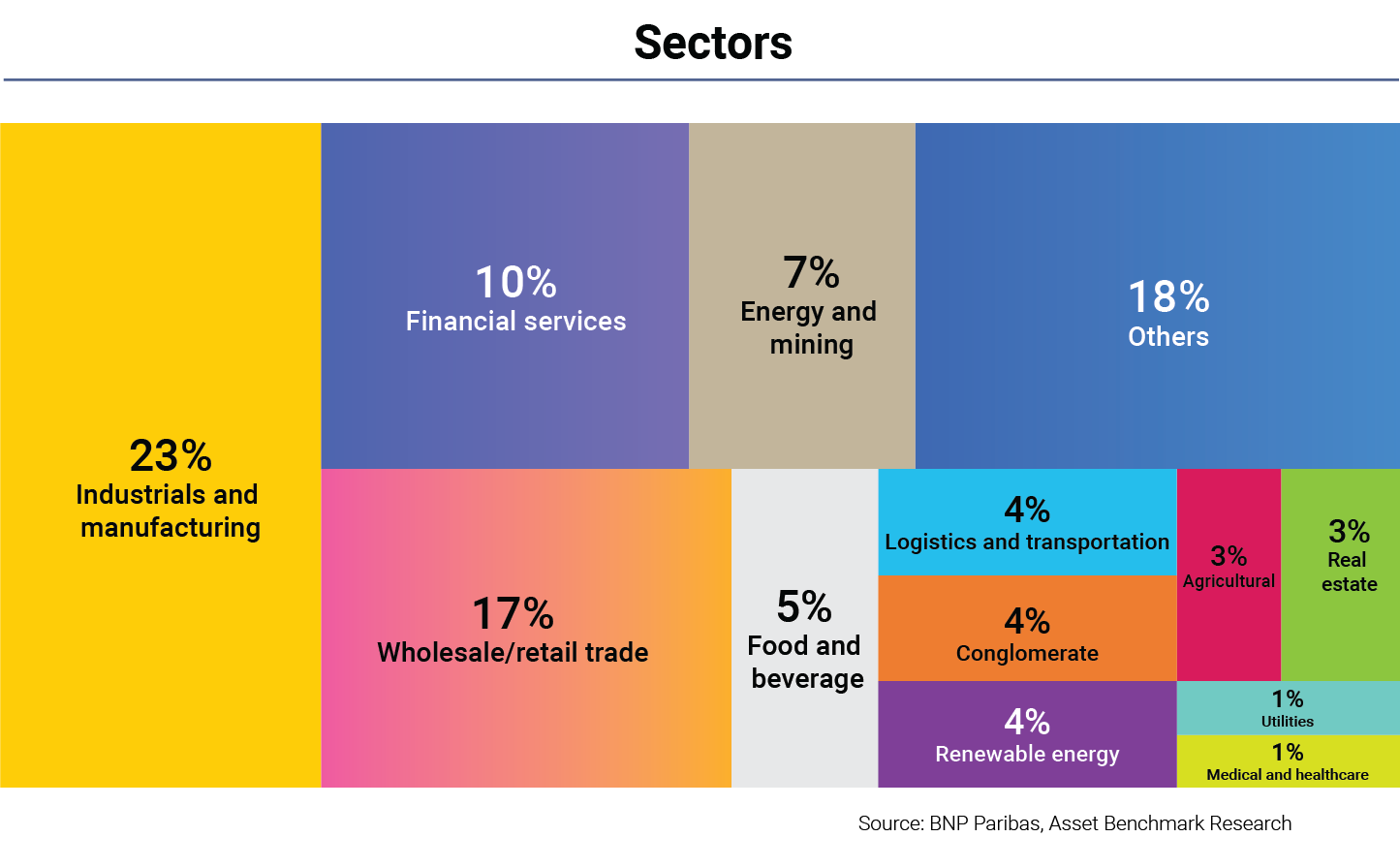

3. Industry breakdown of respondents

Respondents are from a diversified range of industries, with the top three industry sectors being industrials and manufacturing (23%), wholesale and retail trade (17%), and financial services (10%).

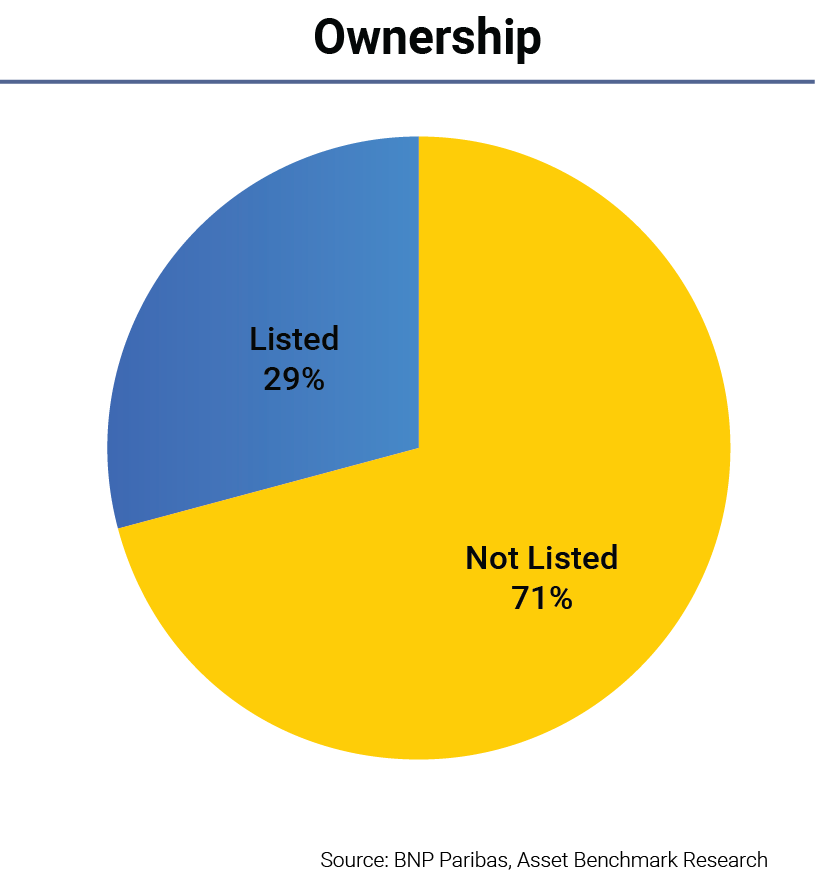

4. Ownership type of respondents

About 70% of respondents are from unlisted companies, while 30% of them are from listed companies. Such a pattern suggests that there is high interest among non-public companies within traditional treasury functions regarding ESG incorporation, despite the fact that they face less pressure from public exchanges and regulators to do so.