Private debt, particularly US collateralized loan obligations (CLOs), have become more attractive for Mainland Chinese institutional investors who are seeking to diversify their portfolios in response to rising interest rates and the search for yield.

CLOs, basically a securitized product backed by a diversified pool of non-investment grade senior secured leveraged loans, have become more attractive as an asset class compared to fixed rate bonds, as short-term interest rates have been rising steadily and the US economy is growing at a pace where the Federal Reserve is expected to continue with interest rate hikes.

“Although US CLOs have long been popular among Japanese and Korean institutional investors, it was only during the last 12-18 months that Mainland Chinese institutional investors, particularly banks and insurance companies, have become extremely active investors. Based on the size of their balance sheets, to the extent that there is a significant capital shift, they can become major players in this market in a relatively short period,” says Oliver Wriedt, co-chief executive officer of CIFC Asset Management, one of the largest CLO fund managers in the US.

.png)

Data as of August 31 2017, as of date of fund closing, includes CLO 2.0 and Fund/SMA investors only. Data from CIFC.

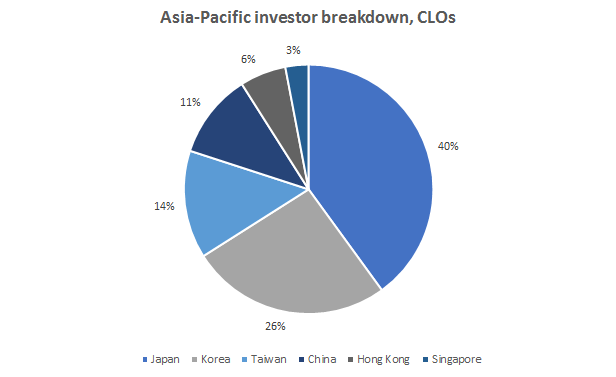

Asia-Pacific investors now account for 16% of CIFC’s total assets of US$16 billion as of August 2017. Of this total, Chinese investors account for 11%, following Japan (40%), Korea (26%), and Taiwan (14%). Hong Kong accounts for 6% and Singapore accounts for 3%.

Data as of August 31 2017, as of date of fund closing, includes CLO 2.0 and Fund/SMA investors only. Data from CIFC.

“We’re seeing a shift out of high-yield bonds, so public non-investment grade debt into private non-investment grade debt. Investors moving away from fixed rate risks into floating rate assets. They’re also moving away from unsecured risk because the typical high grade bond is generally senior unsecured, whereas the loans that we invest in are all senior secured, so we have a perfected interest in all of the companies’ assets,” Wriedt says.

In addition, investors in private debt, which are less liquid assets when compared to public debt, can enjoy an “illiquidity premium” of anywhere from fifty to several hundred basis points, depending on the size of the instrument.

“So if you’re making a direct loan to a middle market borrower, you’re going to get a much higher premium for illiquidity than you get, for instance, if you finance a company like Hilton or Burger King through their syndicated leverage loan,” Wriedt says.

The biggest concern among Asian investors investing in CLOs is how to access the asset class, since the market has become intensely competitive.

“This market is so well bid right now, it has become so competitive that a lot of the big Asian institutions are really trying to figure out how to get into it. Even as deal sizes have grown, the oversubscription is so significant that getting allocations has become difficult, just like in every asset class,” Wriedt says.

In response to this situation, many Asian investors are now seeking to develop strategic relationships with US asset managers who can safeguard access to the CLO market for them and actually deploy the capital.

“2017, and more so 2018, is really about how to deploy this capital because the flows are really significant and they’re really flows out of this region into the US market. A lot of our discussions are around how do you get access to the market, and how do you safeguard getting the exposure,” Wriedt says.

“We found, generally speaking, the sophistication of the Chinese investor is very, very high. We feel that these investors have done their homework. They have a very good understanding of the market, and interestingly, we feel that they know exactly what they want. It’s generally a very good dialogue that we’ve had, certainly when compared to other markets in the region where we feel it’s taking them years to climb up the learning curve,” Wriedt says.