With the markets increasingly expecting the Federal Reserve to cut interest rates in the months ahead, how should Asian investors be thinking about bonds?

Fixed income is a crucial component in portfolio construction for two reasons.

First, its volatility is lower than equities, which helps to manage overall portfolio volatility. Some fixed income, such as development market government bonds, have a negative correlation with equities, meaning the value of these bonds would rise when equities are falling.

Second, fixed income provides a better risk-reward balance than cash. Our analysis of the last two equity bear markets (dot-com bust and Global Financial Crisis) shows US aggregate bonds consistently outperformed cash. This is due to the rise in bond prices as bond yield falls.

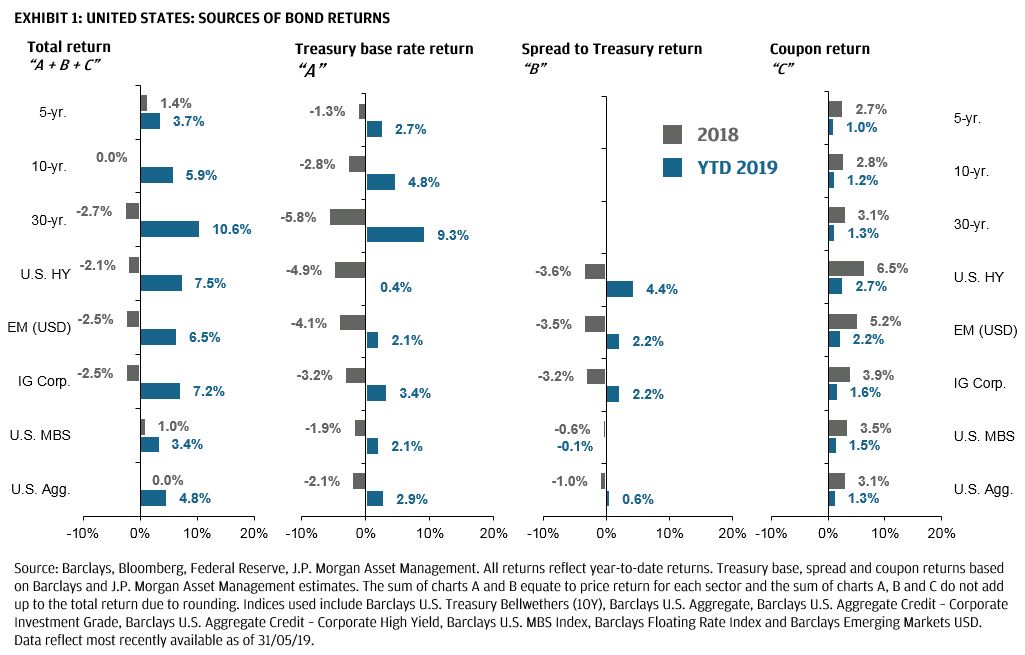

For the question of which fixed income asset class Asian investors should consider, we would propose the following framework. The following chart breaks down three sources of bond return, namely Treasury base rate return (A), or sensitivity towards Treasury bond movements; credit spread (B); and coupon (C).

Coupon (C) is relatively straightforward since this should be know at the time of investing. Corporate high-yield bond and emerging market debt typically offer higher coupon compared to development governments or investment grade corporates because investors are exposed to higher risks, such as credit risk or market risk.

The Treasury base rate return (A) would depend on the movements of US Treasury yields. Falling yields would imply a positive return. The magnitude of this return would depend on the sensitivity of different types of bonds to changes in interest rates, or duration. Historically, we note that Treasury yields continued to fall after the Fed rate cut cycle has started. So this component should continue to contribute to total return.

The credit spread (B) is probably the trickiest of the three sources of return. A deterioration in economic performance would raise the risk of default and this would cause a spread widening for corporate debt, and bond price to fall. High-yield debt is particularly sensitive to this development. EM debt would also depend on the US dollar exchange rate, since a strong US dollar could lead to more capital outflow.

Tai Hui is the J.P. Morgan Asset Management Asia Pacific Chief Market Strategist.