China Securities Regulatory Commission (CSRC) issued guidance on China Depository Receipts (CDRs) on 6 June 2018. This may prompt a few overseas listed China companies to return to China's A-share market.

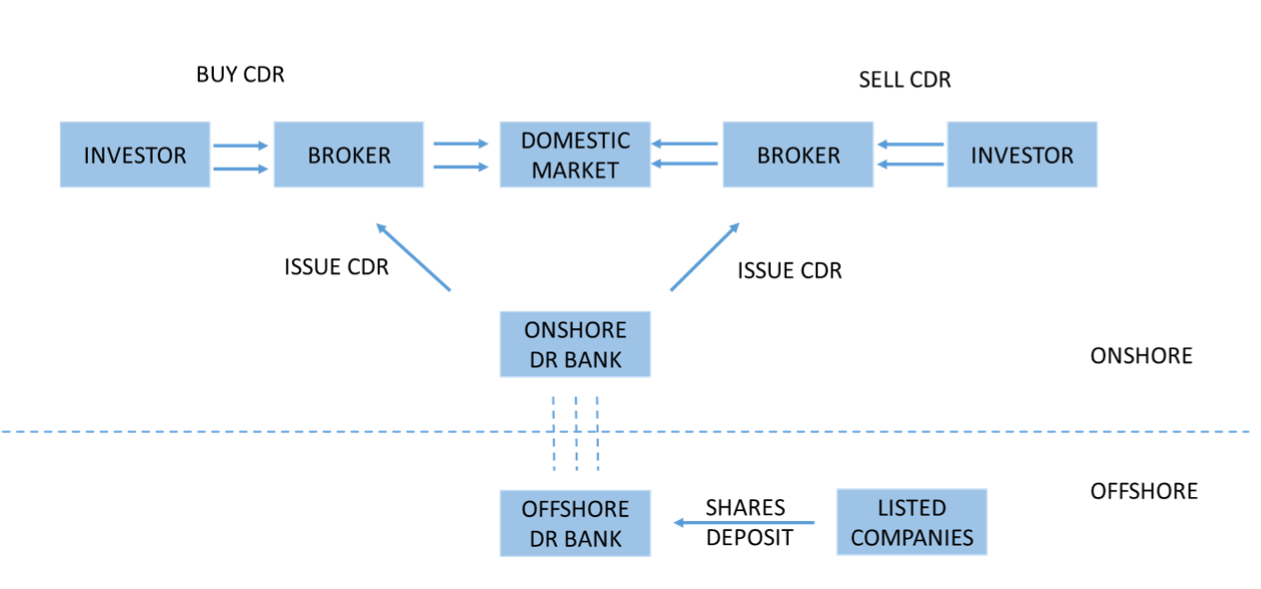

How do CDRs work?

China A-shares cannot have a variable interest entity (VIE) structure, so bypassing the VIE structure and applying for an A-share IPO or having a CDR are the only ways to get listed in the A-share market.

In the CDR program, companies can maintain their VIE structure. The overseas listed stocks will be put in the onshore depository bank. The onshore depository bank will issue corresponding onshore depository receipts. Onshore investors then directly hold overseas stocks through onshore depository receipts.

Note: DR is depository receipt. Source: The Asset

Eligible applicants for CDR?

According to the CSRC, eligible applicants for a CDR are overseas listed China red chips, with market caps of at least 200 billion yuan (US$31.2 billion). For non-listed companies including red chips and domestic companies, applicants need to have revenues of at least 3 billion yuan and a valuation of at least 200 billion yuan for the past calendar year. Applicants should sport high growth, a competitive edge and strong international R&D. Only Baidu, Alibaba, Tencent, JD.com and Netease fulfil the requirements and are qualified overseas-listed applicants. Xiaomi will likely become the first CDR issuer in the program. Baidu is expected to be the first US-listed company to return to the CDR market.

Why CDR?

Key drivers for overseas listed companies to return to the A-share market: higher valuation and a regulatory requirement. As of 11 June 2018 Shanghai Stock Exchange's (SSE) PE was 15.1x while Hong Kong Exchanges and Clearing's (HKEX) PE was 12.7x. In late 2017, Chinese anti-virus software company Qihoo 360 completed its backdoor listing in the A-share market with a PE of more than 100x. The CDR program aims to introduce more Chinese new economy companies and broaden industry breadth in the A-share market.

Potential impact on A-share market?

The CDR program will gradually change the industry composition of the A-share market and add quality high-tech and new economy companies, per China International Capital Corp. It should also boost the growth of new economy companies and accelerate China's economic transition.

Opportunities for financial institutions?

Sponsoring and underwriting are key revenue streams for investment banks, or securities companies in China. Given the size of eligible CDR applicants, related fees may be large. The average IPO fee is 5% in China per Fortune Securities. Asset managers are also set to benefit from strong demand for CDR companies. China AMC, E Fund Management, China Universal Asset Management, China Southern Asset Management, Harvest Fund Management and China Merchants Fund have already launched CDR mutual funds.

.JPG)