With the recent reduction in the US corporate tax rates from 35% to 20% by the Trump administration, there are fears that Chinese corporates, or at least US companies operating in China, may flee to the US to enjoy the new tax benefits.

However, this appears unlikely given that China’s effective tax rate, including value-added tax (VAT), is only 17%, much lower than the US corporate tax alone. In addition, most Chinese local governments still give implicit subsidies to corporates who are large investors to compensate for tax losses, according to a report by Natixis Economic Research.

Hence, while a lower tax rate may lure some large overseas corporates to set up in the US, it is unlikely that China-based CFOs and treasurers will interested.

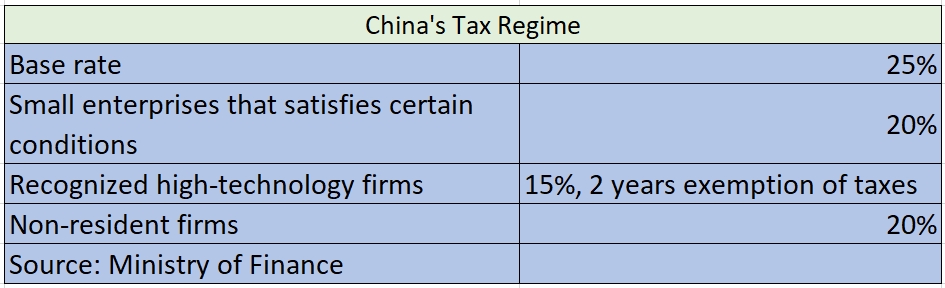

Currently, the official standard corporate income tax rate in China is 25%. This is the base rate. In reality, the base rate is just a maximum rate as China has various tax schemes for different types of companies.

Small companies fulfilling certain criteria are able to enjoy a tax rate as low as 20%, for example, while, high technology companies can even apply for a 15% tax rate with a two-year exemption. China also offers a 20% tax incentive to foreign companies.

China has a very flexible tax rate that can be easily adapted to fulfil its industrial policy or fight off international tax competition.

“The special economic zones, bonded ports and some local governments will also retain some of their tax income when attracting new business. The retained tax income will then be given to companies as a tax subsidy, which lowers the actual tax rate,” says Chao Li, chief macro analyst at Huatai Securities in a note.

Apart from corporate tax, indirect tax such as VAT plays a larger role in China’s tax system. While corporates need to pay VAT, the tax is still deductible for these corporates and they pass it on to their customers who ultimately bear a large part of the tax. According to Natixis, adding all types of taxes together, China’s actual corporate tax rate may not be higher than the US.

“The indirect tax burden is limited to corporates in China, as the characteristic of the indirect tax is that the actual tax burden will be transferred to the consumers,” says Li.

China introduced VAT reform in 2011 on a pilot basis. The reform was expanded to four major sectors, including construction, real estate, and financial and consumer services, starting from May 1 2016. It is expected that China will continue its VAT reform by broadening the tax deductible activities.

In a bid to retain foreign investors in China, the Ministry of Finance, National Development and Reform Commission, Ministry of Commerce and State Administration of Taxation jointly announced a temporary exemption for foreign firms from taxes for reinvested profits on December 29 2017. In addition, most Chinese local governments still give implicit subsidies to large investors to compensate for their losses in tax, according to Natixis.

Data from Ministry of Commerce show that for the first 11 months of 2017, 30,815 new foreign companies have set up in China, 26.5% up from same period in 2016.