Financing difficulties have always been a pain point for Chinese small and medium enterprises (SME). But there's hope since fintech enables Chinese banks and financial institutions to manage risk more efficiently, and ignite a passion for micro-finance.

“In the future, in the context of symmetric information, risk management will change significantly, because I won’t need to make guesses about you. Nowadays, we only have part of the information, and we have to complete the whole personal profile based on incomplete information. But in the future, we will know a lot more about you,” says Liu Bo, founder and CEO of Dashu Finance, at the 10th Asian Financial Forum in Hong Kong.

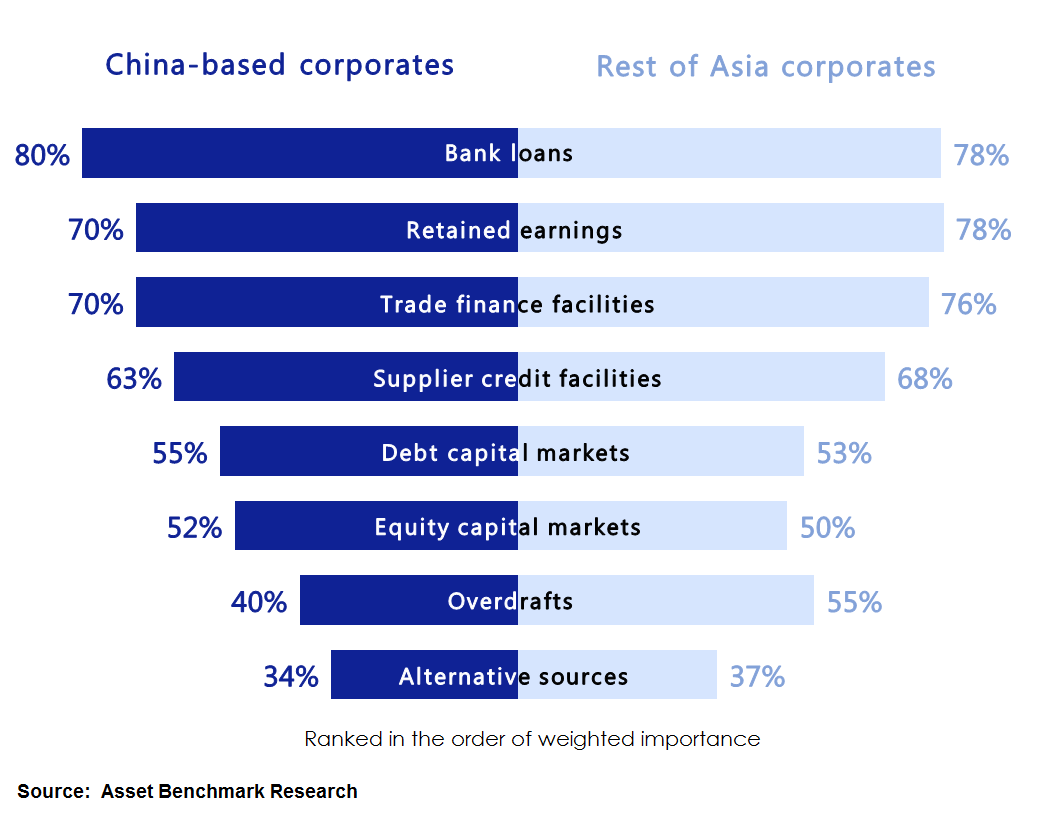

According to a survey conducted by Asset Benchmark Research in 2016, bank loans are still the most favourable funding tool among Chinese corporates. However, a complex application process and strict requirements make bank loans a costly approach for SMEs and financial institutions.

“The micro financing scheme that is currently applied by banks is still similar to standardized bank loans. That makes it complicated and costly for banks to do the micro-financing,” says Ni Rongqing, vice president and chief product officer of Ping An Puhui. “But fintech enables financial institutions to adopt an innovative and better cost structure.”

Comparing the business environments in the US and China, Ni pointed out that the credit market in the US is much more sophisticated than in China, and it is easier for US financial institutions to get access to personal credit data. In addition, the consumption pattern in the US is more predictable, while in China, emerging e-commerce makes it difficult to estimate consumer behaviour, but at the same time, it also provides opportunities for data owners and big data players.

“More third-party institutions will play an important role in collecting information and data, which is not only cheap and easy to get, but also trustful,” says Ni.