As Chinese investors seek more leverage and return, private debt in China is set to take off especially in a private sector that has been suffering from lower bank loan accessibility.

"A lot of good companies with potential are sophisticated, but they don't have the capital to run their business," says a head of structured finance & principal investment at a Chinese securities company in an interview with The Asset. "In the meantime, investors are seeking for more leverage. That's why there is a private debt market, especially mezzanine (market)," he adds.

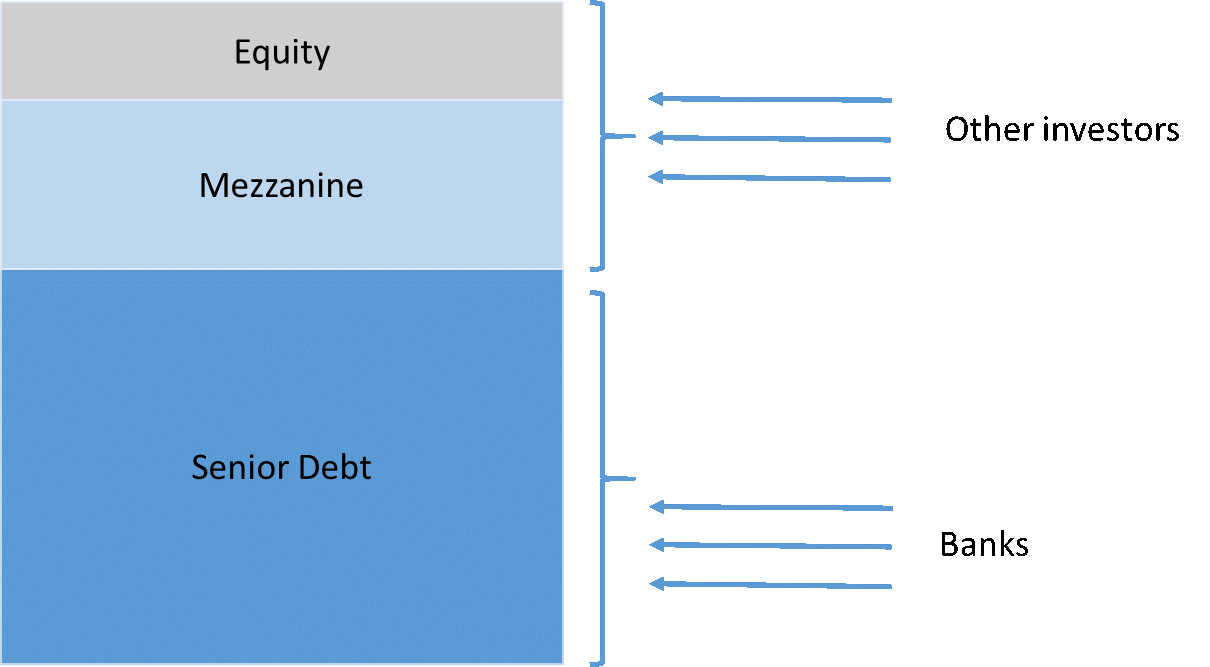

In a typical private debt structure, banks take senior debt at single digit return while private investors, such as private equity (PEs) who possess higher risk appetite, buy the mezzanine and equity portions at double digit returns. When cash flow is generated from the underlying project, senior debt investors are paid first.

A research report from Bain & Company shows that buyout and growth PE funds in Asia-Pacific posted a 13.2% internal rate of return (IRR) in 2017. Given similar rates of return, investors are considering opting for the mezzanine market, which is exposed to credit risk, whereas in PE transactions investors face equity risk. In other words, private debt offers higher risk-adjusted returns than private equity for investors.

Prior to US quantitative easing, asset prices were low and PE investors were able to earn over 20% IRR without leverage. "I used to buy things at 5 times EBITDA, now we are talking about 50 times EBITDA." says the banker. "LPs will start to think, why should I take this risk in this market where asset prices are so high and not much meat is left? Why not take a look at private debt?"

For growing privately-owned enterprises (POEs) which need working capital or acquisition financing, bank loans may not necessarily be available, especially as banks become more cautious in granting credit. China's Industrial Bank, which used to focus a lot on POEs, began easing up on giving loans to POEs three years ago, according to the banker. As a result, private debt became an alternative and preferred option for POEs. In contrast to private equity financing, private debts do no dilute equity to the existing shareholders.

On the back of burgeoning M&A activity from China's POEs, leverage buyouts (LBOs) have also become a popular route for proactive buyers such as HNA over the past three years. In 2016, ChinaChem acquired Syngenta at a value of US$43 billion. The LBO deal was financed through a structure containing loans and bonds.

Chinese financial regulators have been encouraging structured finance as an innovative direct financing channel. China's securitization market, as a major part of structured finance, is now the world second largest, with a market size of 2.37 trillion yuan (US$341 billion).

State-owned distressed debt players such as Huarong have been active acquiring private debts over the past few years, which drove private debt prices higher and yields lower. Yet, as market correction started in 2018, it is expected that the asset return will go back to normal level.

"It was not healthy for the past three years in private credit space. LBO mezzanine requires very high technical skills because sponsors are also technical," says the banker. "People are overly focusing on private equity, but not private credit. And this is a space to fill now."