Issuances in China’s structured finance market are expected to continue to increase in size and breadth of asset classes in 2017 after surging 42% to a record high of 865 billion yuan (US$125 billion) in 2016.

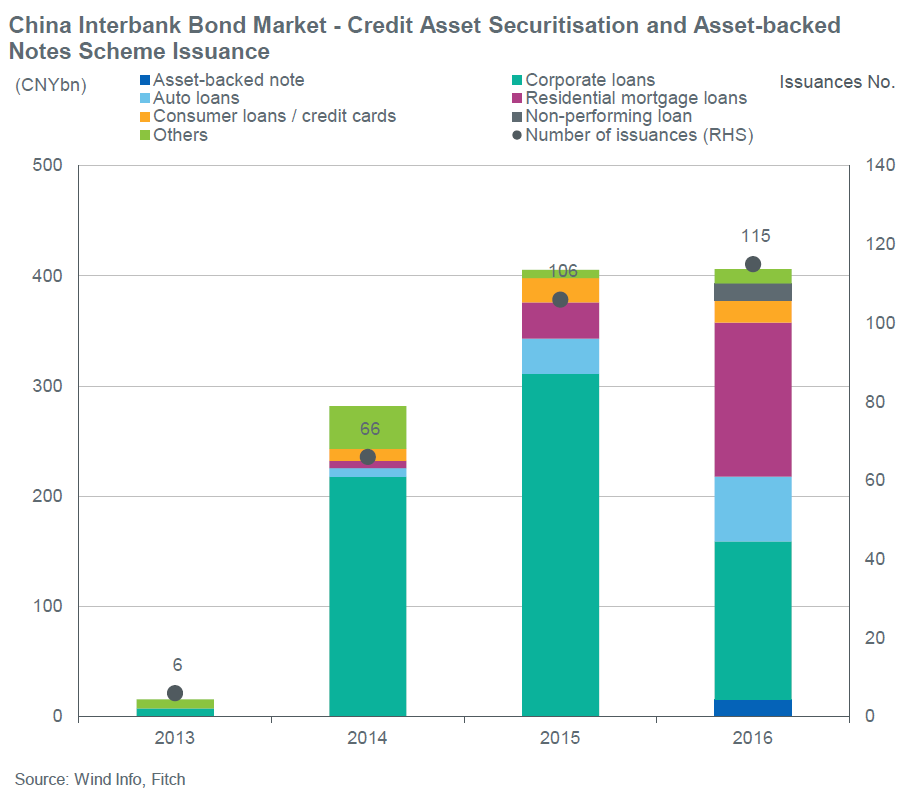

Last year’s issuances also demonstrated the shift in the China interbank bond market (CIBM) from one that was dominated by collateralized loan obligations (CLOs) to a market with more diverse assets. The proportion of auto loans, residential mortgages and consumer loans/credit cards rose in 2016, while 14 non-performing loans and seven asset-backed notes (ABN) were issued last year.

A Fitch Ratings report says the significant growth last year was largely underpinned by the 125% increase in issuance under the asset-backed specific plan (ABSP) to 459 billion yuan. This was driven by exchange markets trying to attract corporate issuers with more diverse underlying asset classes, which may not be eligible to issue in CIBM under the credit asset securitization (CAS) scheme and ABN structure.

ABSP assets include account receivables, rental leases, trust certificates, SME private debts and infrastructure charges.

Total issuance under the CAS scheme and ABN structure in 2016 rose marginally by 0.2% to 406 billion yuan. CLOs registered a 54% drop in issuance, but this was offset by the 84% rise in auto asset-backed securities (ABS) deals and a quadrupling in residential mortgage-backed securities (RMBS) transactions.

In the fourth quarter of 2016, there were seven new auto loan ABS deals with a total volume of 23.9 billion yuan, bringing the full year amount to 58.7 billion yuan, compared with 31.9 billion yuan in 2015. ABS has been used by 14 auto finance companies and banks as at end-2016 and Fitch expects this sector to continue expanding in 2017 with more new entrants into the market.

There were eight new RMBS transactions in the fourth quarter of 2016, with the total issuance of 66.9 billion yuan, bringing the full-year total to 139.7 billion yuan. Three new issuers – Industrial and Commercial Bank of China, Baoshang Bank and Bank of Hangzhou – were granted new RMBS registered quotas during the fourth quarter.

Bank of Suzhou issued its first RMBS transaction in the fourth quarter amounting to 500 million yuan and Fitch expects more issuers will use RMBS securitization as an alternative funding and balance sheet management tool in 2017.

In other asset classes, two new credit card ABS, two new consumer loan ABS and one new financial leasing ABS transaction were recorded in the fourth quarter of 2016. Fitch expects the issuance of consumer-related and auto ABS, as well as RMBS to continue to be the mainstays of

China’s structured finance market in 2017 – in line with the supply-side reform emphasized by the government in its efforts to rebalance the economy.

Meanwhile, more ABN special purpose trust (SPT) structure transactions were issued in the fourth quarter after the National Association of Financial Market Institutional Investors (NAFMII) issued amendments to the ABN guidelines in December 2016 that clarified the use of SPT in ABN issuance.

Fitch says it believes a migration of transactions from the ABSP scheme to the ABN scheme is likely in 2017 as the ABN with SPT structure may offer a more robust segregation of assets from transaction counterparties than the ABSP scheme and issuers may be keen to tap the deeper investor base in the CIBM.

.JPG)