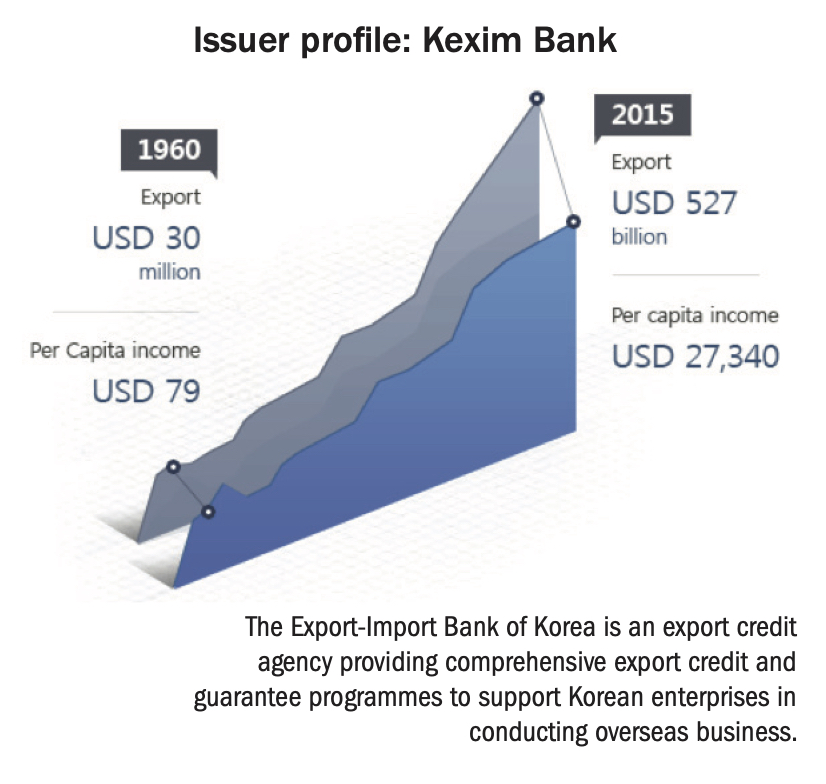

As one of the savviest and frequent issuers in the G3 bond market in Asia, the Export-Import Bank of Korea (Kexim) should have no problem accessing the market to meet its annual funding requirements. But its treasurer Hee-sung Hoon has some concerns as the market ushers in the new year, and as it commenced its issuance activity in 2017.

“We saw an uptick in rates post the US election,” he tells The Asset. “Also, the victory of Donald Trump gave another leg to the strong US dollar theme, with the euro and yen all set to weaken. The fiscal stimulus from the new administration is likely to boost growth in the US, while the Federal Reserve could accelerate the rate hikes.”

On Europe, Hoon notes that political uncertainty still persists, and growth and inflation rely on easy policy, which are likely to lead to a weak euro. The yen could further weaken, also driven by higher US yields.

“We are facing tough external headwinds with potentially more volatile market conditions,” says Hoon. “We need to capture the right window for execution to avoid any potential market risk and any uncertainties, and we should be nimble to capture the right timing.”

Hoon’s comments come as Kexim commenced its fund raising in 2017 as it priced on January 18 a three-tranche offering totaling US$1.5 billion in equal split of US$500 million each. The first tranche was a three-year fixed rate note which was priced at 99.905% with a coupon of 2.125% to offer a yield of 2.158%. This represented a spread of 70bp over the US treasuries, or at the tight end of the final price guidance of between 70bp and 75bp.

The second tranche was a five-year fixed rate note which was priced at 99.736% with a coupon of 2.75% to offer a yield of 2.807%. This was equivalent to a spread of 92.5bp – also at the tight end of the final price guidance of 95% area (+/- 2.5bp).

The final tranche was a five-year floating rate note (FRN), which was priced at par with a re-offer spread of 87.5bp over three-month US dollar Libor. This was the first five-year FRN in public offering space out of Korea after the Lehman crisis.

“After the Republic of Korea trade, we saw global investors’ confidence in the Korean economy and wanted to take maximum advantage of it,” says Hoon. “As the most frequent issuer in Korea, we wanted to pave the way for other Korean issuers to follow as we have always done historically.”

Kexim was not supposed to price the deal on January 18, which turned out to be an extremely busy day with a lot of competing supply – there were eight deals out in the Asian primary market.

“January 17 was on the table for the execution window for us, but another policy bank in China already made an announcement that they would print their bonds on that day,” says Hoon. “We knew the pipeline for the rest of the week was pretty congested, but we did not want two Asian policy banks out in the market simultaneously and be in comparison with each other. Instead, after carefully monitoring the market, we accepted the arrangers’ recommendation that January 18 would be more proper to attract focus from investors.” One of China’s policy banks, China Development Bank, on January 17 priced a dual-currency, multi-tranche offering amounting to over US$4 billion equivalent.

In printing a three-tranche transaction, Kexim’s main motivation was to re-price its five-year part of the curve and find fair value. “We thought that our outstanding bonds in the five-year part of the curve did not reflect the fair value, so we wanted to establish the new five-year benchmark and re-price while taking maximum size out of that part of the curve,” says Hoon.

That is why Kexim added the FRN portion in the transaction. “We have witnessed our regional and global peers printing five-year fixed and FRN simultaneously – to target additional pockets of demand that focus on FRN and diversify investor base,” adds Hoon.

While targeting the additional demand on FRN, with the five-year trade, Kexim took some of the pressure off from the five-year fixed tranche, and had full discretion to manoeuver the size and target of either fixed and FRN, subject to demand and its aspiration for this offering. Eventually, both the five-year fixed and FRN ended up as a success, according to Hoon, achieving the target size.

In printing a three-tranche transaction, Kexim’s main motivation was to re-price its five-year part of the curve and find fair value. “We thought that our outstanding bonds in the five-year part of the curve did not reflect the fair value, so we wanted to establish the new five-year benchmark and re-price while taking maximum size out of that part of the curve,” says Hoon.

That is why Kexim added the FRN portion in the transaction. “We have witnessed our regional and global peers printing five-year fixed and FRN simultaneously – to target additional pockets of demand that focus on FRN and diversify investor base,” adds Hoon.

Proceeds from the offering will be used for general corporate purposes. Daiwa, Deutsche Bank, Goldman Sachs, HSBC, J.P. Morgan and Standard Chartered were the joint bookrunners for the transaction, as well as joint lead managers along with Hanwha Investment and Securities. Kexim Asia acted a co-manager.

.JPG)