Welch Lin, chief financial officer at Taishin Financial Holdings and chairman of Taishin Securities, cannot hide a smile when comparing recent analyst calls to a few years back. “Two years ago, when talking to investors and analysts, they would ask me: ‘Hey, you are missing out on opportunities in China. What are you going to do to catch up?’ But in recent months, they ask: ‘What is your exposure to China? How will you control the risk?’ Their attitude has changed completely.”

Welch Lin, chief financial officer at Taishin Financial Holdings and chairman of Taishin Securities, cannot hide a smile when comparing recent analyst calls to a few years back. “Two years ago, when talking to investors and analysts, they would ask me: ‘Hey, you are missing out on opportunities in China. What are you going to do to catch up?’ But in recent months, they ask: ‘What is your exposure to China? How will you control the risk?’ Their attitude has changed completely.”

Cross-strait exposure under review

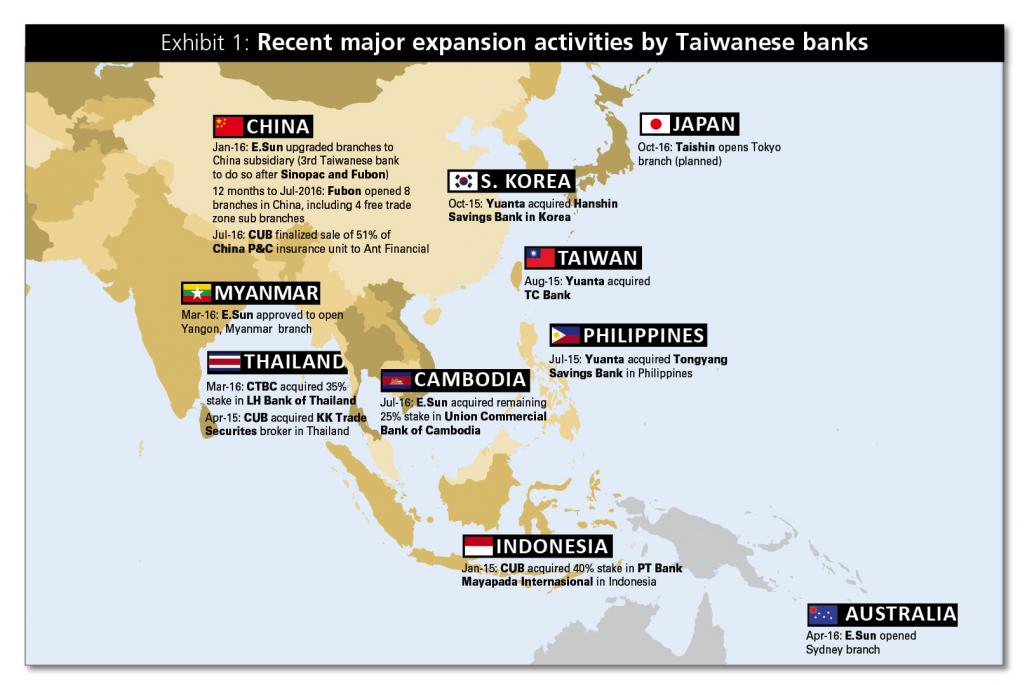

Taiwanese banks are still keen on expanding in China

In contrast to the explicit recommendation by the financial regulator to Taiwan’s banks to expand in Southeast Asia, the Ministry of Finance issues a stern warning with respect to exposure northbound. “Naturally, we as a shareholder, do not want Taiwanese banks to have much exposure to the mainland China market,” Deputy Minister Jain-Rong Su of the MoF says in an interview with The Asset. “Banks’ debt level and the quality of assets are the two concerns. We want them to reduce exposure as much as possible, especially when the mainland China market is having problems these days [and] bad loans are going up.”

Dr. Su urges banks to implement rigorous assessments when extending credit to customers in China. He also cites a Financial Supervisory Commission (FSC) regulation that stipulates exposure of Taiwanese banks to China cannot exceed 1x their net assets. In reality, no bank reaches that ceiling and instead, the industry average has decreased to about 0.6x, officials from the FSC confirm. Yet, at the same time, non-performing loans of some banks with exposure to China has increased markedly.

For Fubon Bank (China), for instance, NPLs rose from 1.04% at the end of 2015 to 1.91% at the end of the March this year. Executives at the bank expect the ratio to stabilise, though, going forward.

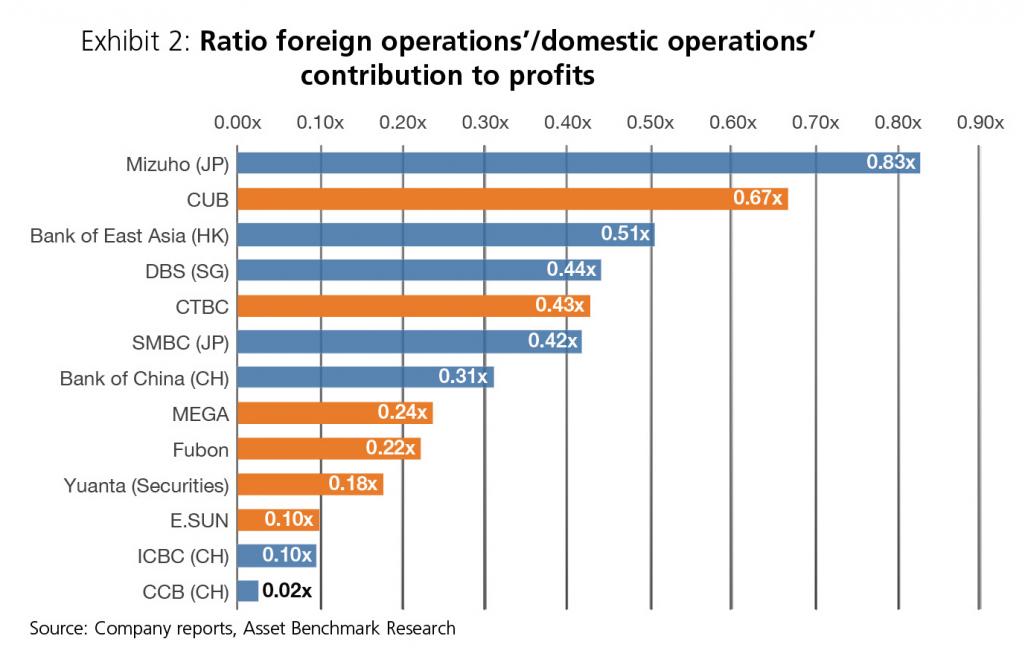

Analysts at HSBC believe the China-related fears are overdone. Even if the NPL ratio for loans of mainland subsidiaries and branches of four large Taiwanese financial institutions (E.Sun, Mega, Yuanta and CTBC) were to rise to 5%, the overall NPL at these banks would remain below 0.7% and the pro-forma NPL coverage would stay above 200%, their analysis shows.

Indeed, Taiwan’s banks are still keen on expanding in China, selectively. Fubon, which in May received the green light to acquire the remaining 20% stake in its China subsidiary from Shanghai Pudong Development Bank, has increased its branch network to 22 in the mainland. That includes two new provincial branches in Nanjing and Beijing. It has obtained nearly all licenses, including for debit card and negotiable certificate of deposit issuance. It expects to submit its application for a renminbi retail banking license later this year.

Cross-strait strains will not have an impact on the success of the application, says Vivien Hsu, president of Fubon Financial Holdings. “The communication with China’s regulators and local peers has been quite smooth and frequent despite Taiwan’s government changing hands,” she notes.

Regular exchange with the CBRC and other regulatory authorities continues. A yearly summit between financial regulators from both sides of the Taiwan Strait is scheduled to occur in the last quarter of the year.

Cathay United Bank, which completed the sale of 51% of its P&C insurance company in mainland China to Ant Financial in 2016, also seeks to upgrade its branch network to a subsidiary. According to Alan Lee, chief executive officer, approval has been granted from the FSC while CBRC approval is pending.

Joseph Huang, president of E.Sun FHC, expects long-term pragmatism to prevail. “There are some challenges in the relationship after the new government took over. They have different views on the 1992 consensus which has caused some disputes. But in the long run, the cross-strait relationship is necessary to both sides.” E.Sun, which upgraded its China operations to a subsidiary in January, has a loan book of US$200 million in the mainland.

Taishin, which currently has two leasing companies in the mainland, has not given up on its plans to open branches as well. “Our new Brisbane branch has a hidden agenda,” confirms Welch Lin, chief financial officer at Taishin. “We still want to enter China but because of the OECD restriction we haven’t been able to.” Banks from either side of the Strait must be present in an OECD country for at least five years before they are allowed to open branches on the other side of the strait.

With the Australian branch expected to open early 2017, Taishin would be able to open a branch in mainland China in 2022 at the latest – unless, of course, both sides agree to scrap the OECD Rule. Until then, Taishin will need to be a bit more patient.

New momentum in CHB acquisition?

Taishin is keen to restart its international expansion on its own

When Taishin Financial Holding Company retracted an injunction against Taiwan’s Ministry of Finance on May 19, it was not waving a white flag of defeat. Eleven years after its spade with the Ministry over Chang Hwa Commercial Bank began, Taishin hopes to finally come full circle.

“We chose the date of our appeal carefully, on May 19, to signal we are suing the old government,” says Welch Lin, chief financial officer of Taishin FHC in an interview with The Asset.

To recap, Taishin had acquired 22.5% in Chang Hwa Bank in 2005 at NT$26.12 per preferred share – at a time when common shares of CHB traded at NT$18 and a global depository receipt offering had fallen through. Singapore’s Temasek Holdings as well as Mega Financial Holdings had made lower bids for the troubled lender. Taishin paid the hefty premium because the Ministry of Finance agreed to help it win majority control of CHB’s board, an agreement that the ministry later refused to honour when the government changed hands in 2008.

The renewed rise of the Democratic Progressive Party to power this year may bring things full circle. Indeed, current Premier Lin Chuan was Minister of Finance at the time of the transaction in 2005 and is therefore privy to all intricacies of the deal. Now is the government’s turn to introduce new momentum in the merger, Lin urges.

“I am calling on the new government to do the right thing, to complete what they should have completed years ago. If they change the policy and decide to stop consolidation, Taishin will support that decision. But there should be a reasonable mechanism for Taishin to withdraw from CHB, instead of violently using governmental power to take away the legal rights of Taishin shareholders.”

The response by the Ministry of Finance, however, follows a well-known beat. “The MOF insists that it does not have a contractual obligation with Taishin Financial,” a spokesperson for the Ministry responds to a written request for comment by The Asset in September. “As for Chang Hwa Bank’s board or directors’ re-election in 2017, the MOF will seek to gain the most favourable seats to oversee the management of the company to ensure and enhance the government equity [stake].”

Taishin currently is CHB’s largest shareholder and holds 22.55% of outstanding shares. It controls three seats in the 10-member board of CHB while the Ministry of Finance, which owns 12.19% of shares, is represented with four delegates. The terms of the current board members expire in July 2017. Lin hopes to see one of two things to happen preferably before then: either Taishin is given control of CHB’s board so that it can again consolidate financial statements or a sale of its stake to another government-owned bank or other institutional investor is arranged at terms agreeable to Taishin. With compound annual growth of net income at CHB exceeding 12% over the last three years, shareholders would likely prefer the former.

With the Ministry’s stance unchanged, though, Taishin has little choice but to restart its international expansion plans on its own.

“As early as 2003, we had our Hong Kong branch and started to go overseas where we could. Two years later, when we got the stake in CHB, we slowed down our international deployment because CHB already had six overseas branches. Things did not go as well as we had hoped with CHB, so we restarted our international deployment in 2014 with the opening of our Singapore branch,” Lin explains.

Earlier this year, Taishin’s shareholders agreed to a NT$80 billion capital increase, to be facilitated later this year through common or preferred shares issuance.

Taishin is currently looking to acquire a life insurance company to complement the existing banking and securities subsidiaries of its financial holding company. “Banks can collect deposits but a majority of it can be used for lending only,” reasons Lin. “But life insurance is a different story; the premiums collected can be invested in securities, real estate and other assets. So that can enlarge the footprint of the FHC and create synergies and cover a wider client base.”

Lin confirms Taishin is already in talks with specific life insurance companies but declined to disclose more comments.

Regardless of whether the new government decides to budge, Taishin is trying to move on.

Closing the case on TRFs

Can the banking industry put the TRFs behind it?

When the People’s Bank of China (PBoC) stepped up intervention in the CNH market and moved to daily liquidity injections in the onshore market right before Chinese New Year, sighs of relief were heard across Taiwan in the board rooms of the country’s largest lenders. Just when the market thought it could forget about target redemption forwards (TRFs), the renminbi devaluation of August 2015 caused a fresh wave of defaults among corporates that firmly believed in continuous renminbi appreciation.

“Had the PBoC not stepped in earlier this year, right before Chinese New Year, to set the exchange rates, a lot of companies and clients would have experienced severe financial distress,” relates John Huang, chief executive officer for Cathay United’s Private Bank. “Many were overextended, thinking such falls in exchange rates were unlikely.”

“TRFs are a real disaster,” agrees Allen Wu, executive vice present for Yuanta Bank and senior vice president for the financial holding group. “People always believed the renminbi would appreciate until August last year. As a result, banks and investors suffered.”

TRFs are over-the-counter structured notes that generally work in a way that allows clients to accrue gains amounting to the difference between strike and fixing rate, times the notional principal as long as the renminbi is stronger than the strike rate. While the upside gains are usually limited in such structures, losses in case the underlying currency depreciates are not limited.

HSBC analysts Anthony Lam and James Garner explain: “If the RMB is weaker than the strike rate, clients would lose an amount equal to the difference between fixing rate and European knock-in rate (weaker than strike), times the notional principal, times the leverage. [As] there is no knock-out protection on the downside, the contract will not terminate early by itself, exposing clients to theoretically unlimited losses.”

Renminbi TRFs were popular structures among small and medium sized enterprises, many of which declared the accrued gains in times of renminbi appreciation as part of their operating income to boost their bottom line performance. According to bankers in Taiwan, a common practice for entrepreneurs was to open accounts with as many as 10 banks and maxing out credit limits for derivatives granted to them. When the currency depreciated, few were able to meet margin calls and defaulted as a result.

Provisions taken by banks until the end of the first quarter 2016 varied widely and ranged from US$3 million at E.Sun to US$30 million at Yuanta, US$50 million at TC Bank and around US$100 million at Taishin. “We got burned,” concedes Welch Lin, chief financial officer at Taishin FHC. Changes to the commissions and incentive plans to the sales staff and enhancements in the KYC of companies keen on buying TRFs have addressed the issue, Lin continues.

As of May 2016, the notional principal of TRFs that was still outstanding stood at US$1.1 billion, the Financial Supervisory Commission (FSC) says. That is down 62% from May 2014.

“The TRF issue is really a KYC issue,” explains an industry source familiar with the matter. “The relevant KYC and KYP regulations have been revised already to make sure something similar does not occur again. But now the situation is manageable, under control.”

While the regulator did not issue a sweeping ban of TRFs, banks that distribute structured products with an FX element must first seek approval from the central bank and then register with the FSC. Furthermore, thresholds of being considered a professional investor with access to such products have been revised upwards.

Starting in the second half of 2016, banks also have the ability to check their clients’ derivative credit lines with other banks through Taiwan’s credit bureau, the Joint Credit Information Center (JCIC). Credit Suisse, a major developer and issuer of TRFs that are then sold on to Taiwan’s banks for distribution to end clients, expects TRF volume to decrease by 80% this year as a result of these regulations. Maybe Taiwan’s banking industry can now truly put TRFs behind them. Maybe, though, the better question to ask is what will replace them.

The future of ETFs

Exchange traded funds offer alternative solutions to investors

In less than two years since its listing, Yuanta’s Taiwan Top 50 1X Bear ETF has grown to become the largest ETF on Taiwan’s stock exchange, with more than NT$80 billion in assets. The popularity of an inverse ETF, which benefits investors only if the market’s largest 50 stocks by market capitalization perform poorly, is testament to a wider shift in Taiwan’s ETF landscape. It could become a model for other markets as well.

“We don’t just sell products, we sell solutions,” explains Julien Liu, president and chief executive officer of Yuanta Securities Investment Trust, Taiwan’s largest issuer and manager of exchange traded funds. “We are changing the distribution model from a push and marketing driven model to a pull and client driven solutions model. For example, some investors may not be allowed to trade futures because of their internal protocols. Inverse ETFs are an alternative solution for this group of investors seeking to hedge a particular asset.”

In addition to tracking share performance, new ETFs are also branching into other asset classes including commodities and bonds, Liu says, in order to provide solutions for different needs.

“In the future, ETFs will serve three broad needs of investors: capital protection, cash management and enhancement as well as currency hedges,” Liu explains. “That will be the new reality of Taiwan’s ETF market.”

According to Liu, ETFs could become alternatives to regular checking accounts. Similar to Yuebao, the mobile investment channel on Alipay in mainland China, retail investors could use ETFs for cash enhancement purposes of discretionary funds. The only difference would be a slightly longer settlement cycle, at T+2 rather than same-day withdrawal rights offered by a checking account. Even credit and debit cards linked to portfolios of ETFs might be introduced in the market: each time they are used, the equivalent amount spent is redeemed. With nine million brokerage accounts registered among a population of 23 million, Taiwan boasts high sensibility to exchange traded securities, providing a robust foundation for acceptance of such ideas.

On the institutional investor front, ETFs are also changing the landscape. In late July, Yuanta filed an application for the listing of the first ETF to track bond performance, specifically longer-dated U.S. treasury bonds with remaining maturities of at least 20 years. If liquidity in the Taiwan Government Bond market ever allows it, a replication involving local bonds could follow.