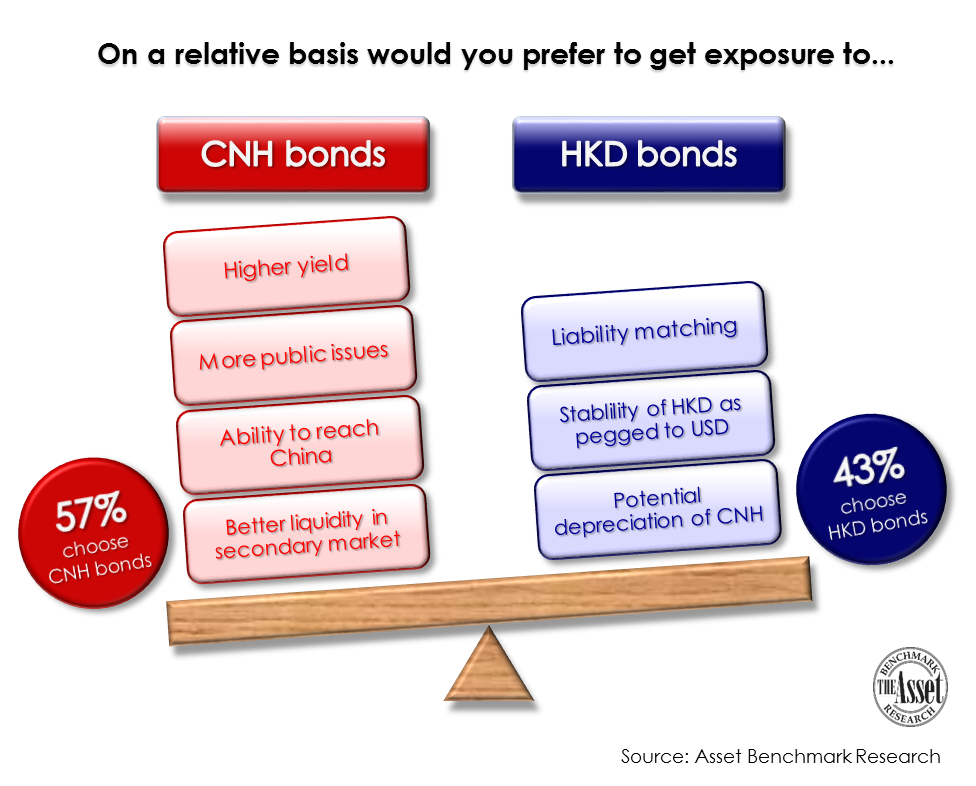

Do investors prefer to gain exposure to Hong Kong dollar or CNH bonds? A survey by Asset Benchmark Research (ABR) reveals that they would opt for the latter, but not resoundingly.

Despite the higher yields, larger choice of public issues, better secondary market liquidity and exposure to the China market, only 57% of fund managers favoured CNH bonds.

There are several push and pull factors at play. One institutional investor explained their preference for CNH was because the “Hong Kong dollar bond market is kind of dead.”

For many, yield and liquidity are major determinants. “Of course one reason is better absolute yield [in CNH bonds],” commented another investor. “Although both markets’ liquidity is still not that great, it seems the HKD bond market is still worse. The CNH bond market moves two steps forward and one step back, but it’s still gradually moving.” The attraction of the China economy is also a factor. The renminbi (and its offshore CNH) “is the currency that is up-and-coming, which is why we’re exposing ourselves more versus the Hong Kong dollar due to the opening of their economy and the ability to reach into China itself,” said a Singapore-based asset manager.

However, a significant body of those surveyed (43%) chose Hong Kong dollar bonds over CNH. One of the reasons cited was the stability of HKD as it is pegged to the USD and the outlook for the Chinese currency. “Because of a potential CNH depreciation, over the medium term against the US dollar, the FX return [of HKD assets] will be higher than CNH,” was the view of another investor. But many are locked into the Hong Kong dollar market as a result of a home bias for liability matching purposes or because clients’ mandates dictate it.

The question was part of the annual Asian Local Currency Bond Benchmark Review. The survey probes into the product needs of fixed-income investors and the market penetration of banks active in local currency bonds. Additional reporting by Jacky Fung

To read more about Asset Benchmark Research, please click here.