“Doing well by doing good” is the slogan that perhaps epitomizes ESG investing best. Or at least this is what ESG investment providers would like us to think. It is a persuasive argument: make money investing in companies that are saving the planet and helping others.

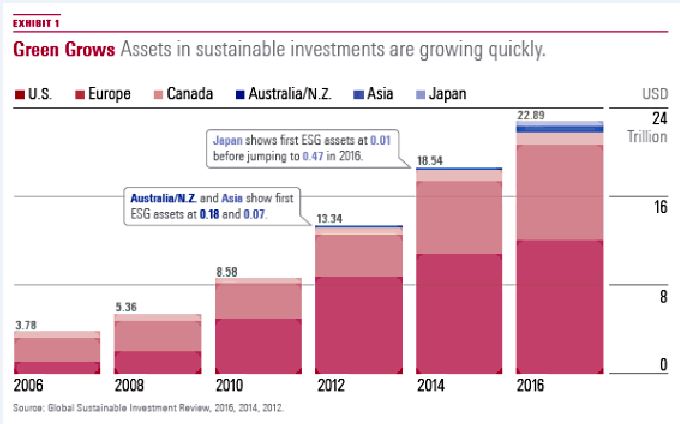

Combine this with a generational shift in consumer awareness in environmental and social responsibility – 43% of US millennials are seeking to invest in ESG products, according to one survey, while another survey shows that 33% of Asian investors reported to have increased their investments in ESG. It is no surprise that ESG investing has exploded into an estimated US$22 trillion industry today, representing about a quarter of all professionally managed financial assets in the world, according to Morningstar.

The logic behind ESG investing is absolute and faultless. Shun investments in companies that harm the environment, mistreat people and their employees, and are susceptible to corruption. With a decrease in the number of investors, these sinful companies’ cost of capital increases, which in turn lowers the number of projects they can finance. Given enough investors (and thus size), ESG investing accomplishes this.

But what many ESG investment providers fail to tell you is what happens to your investment returns should you choose to go down this virtuous path: in aggregate, over the long run, ESG investing will underperform the broader market.

The reasoning behind this fact is also ironclad. As ESG investors proliferate and crowd the market, they will send share prices of the sinful down and the virtuous up. In other words the sinful becomes cheap and the virtuous expensive. And what is the most tried and tested principle of security analysis? Over the long run, the cheap outperform, the expensive underperform. The mechanisms of reversion to the mean decree it so.

If this statistical explanation feels unsatisfactory, note earlier when we said that the cost of capital of the sinful increases as ESG investors crowd the market. When a business is debating whether to undertake a project or not, it forecasts the project’s net future cash flows and discounts it at the rate of cost of capital to calculate the project’s net present value (NPV). If this value is a positive figure, the project is deemed worth the financing (unless another project’s NPV is higher and the business has budget constraints).

The kicker here is this: the discount rate, previously stated as the cost of capital, is also the expected return. This is true because as the virtuous makes sinful businesses/projects more costly, the sinful must demand businesses/projects with higher expected returns than they would have otherwise. “One man’s discount rate, is another man’s expected return”, is how Cliff Asness, founder and CEO of the quantitative investment firm AQR Capital Management, aptly sums it up. AQR’s research have shown that companies lowly ranked by MSCI on ESG standards have had higher volatility. But the same study found that those companies also had higher returns, backing up the idea that this risk comes with rewards.

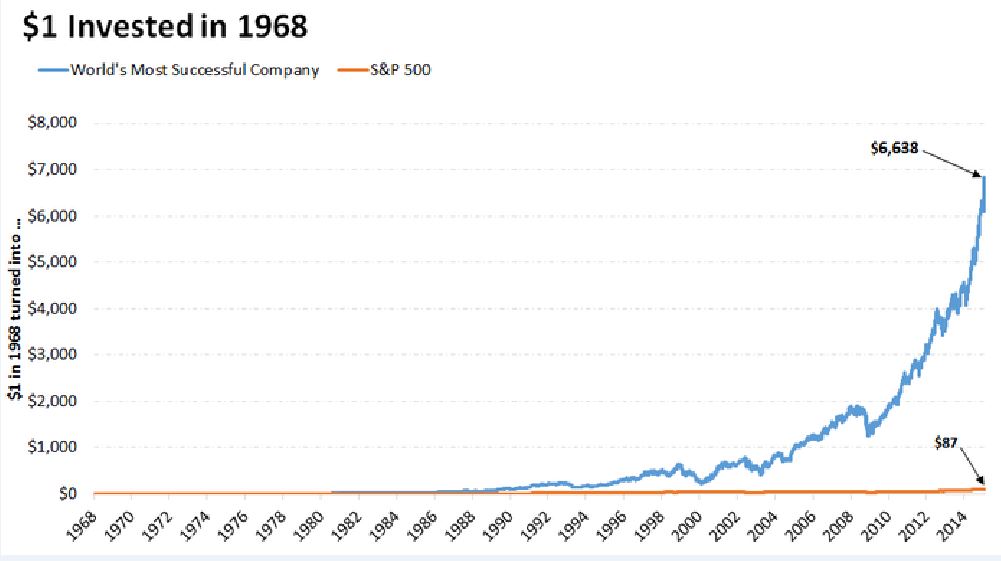

Tobacco stocks are the prime example of this phenomenon at work. For decades, large factions of the investing universe (mutual funds, pension funds, and endowments) had mandates that prohibit them from investing in cigarettes. Low investor demand has kept tobacco stock valuations perpetually low. This coupled with high dividend yields, compounded over decades, have led the best overall stock returns over the last 100+ years – one dollar invested in tobacco stocks in 1900 was worth US$6.3 million by 2010. That is 165 times better than the average of all industries. Altria (previously known as Philip Morris) is the greatest performing stock of the last 50 years, returning more than 20% annually.

Despite the fundamental reasons why ESG investing underperforms the broader market in aggregate, many ESG investment providers market themselves as being able to outperform. In some cases this may very well be true – an ESG focussed investment manager can outperform if he or she is a skilled stockpicker, overlaying ESG concerns with other factors such as value, profitability and capital structure.

At other times it seems the marketers are simply incentivized to believe what they are saying is true (it is hard to imagine a seller of a product claiming its product is inferior). Some will show five-year price charts that shows ESG investment outperformance. But it's best to remember virtually any investment strategy, no matter how irrational it is, can be made to look good within a five-year timeframe.

Then there is the whole separate issue of defining and quantifying ESG. ESG ratings providers don’t seem to agree all that much on what constitutes an ESG investment. General Motors, for example, is given an ESG score of about average by Sustainalytics, but rated at the very bottom by MSCI. Meanwhile, FTSE gives General Motors and Exxon Mobil a better score than Tesla. FTSE justifies this by saying it judges companies’ supply chain, not its products.

Ultimately, the values of virtue are in the eyes of the beholder, and these criticisms of ESG thus far were made not to deride ESG investing as a whole. As noted, ESG investing in fact does accomplish its true goal: increase the sinful’s cost of capital. The point however is to not confuse a company’s dim financials with its share price performance. Unfortunately, even the worst-run company in the world, be it in their environmental concerns or corporate governance, can be profitable investments at a cheap enough price. Prospective ESG investors would do well to keep this in mind, manage their expectations, and proceed with their eyes wide open.

James Kim is a contributing writer for The Asset.