NEXT year could be a breakout year for China’s economy, as the economy rebalances away from investment and external demands towards domestic consumption, and Chinese equities are supported by stable macroeconomic data, upward earnings revisions and reasonable valuations, according to investment experts.

“The point we have made to investors globally is that 2018 could be a breakout year for China,” says Rick Lacaille, executive vice president and global CIO of SSGA. In this context, he also sees interesting investment opportunities in emerging markets near China.

“One of the reasons we like emerging markets is the continuation of China’s growth story and the fact that it’s supportive of trade and earnings of companies in the region,” says Lacaille. “Investors have worried every year for the last four or five years that the growth of China’s economy would suddenly fall. We did not think that. China will have a gentler deceleration in 2018.”

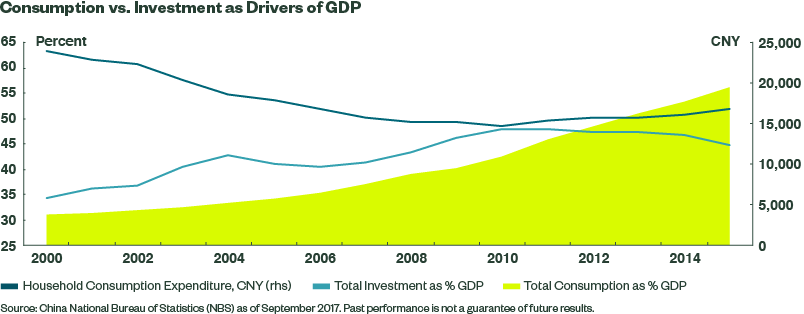

Chinese economic growth is unlikely to reduce sharply in 2018 due to long-term trends, such as the shift away from investment-driven growth towards consumer goods and services, according to a recent report by SSGA.

“China’s economic growth is expected to moderate slightly in the coming years as the economy rebalances away from investment and external demand towards domestic consumption,” says Raymond Ma, portfolio manager at Fidelity International. Ma adds that next year could be another strong year for Chinese equities supported by stable macroeconomic data, upward earnings revisions and reasonable valuations.

Jing Ning, portfolio manager at Fidelity International sees investment opportunities arising from the long-term structural changes in China. “At the sector level, I have noteworthy exposure to energy, materials and financial stocks,” she says.

After the 19th Party Congress, China’s top leaders said that the emphasis of the country’s economic activity will be on “quality over quantity”. Thus, the country is likely to focus on deleveraging and reforms, according to Ning.

“So far, the People’s Bank of China (PBoC) has been more proactive than prominent Western central banks in raising its interbank lending rates. This tighter liquidity environment is favourable for the big banks with stronger balance sheets and reflects that the economy is stabilizing, which will allow the government to pay attention to reforms,” says Ning.

In order to improve the economic growth model, China has taken steps in implementing supply-side structural reforms. Many of the country’s state-owned enterprises (SOEs) are undergoing mixed-ownership reforms, diversifying the shareholding structure of these companies. The reform scheme will be completed by the end of this year, according to China’s State Council.

The ongoing supply-side reforms will increase China’s production efficiency and improve corporate earnings, according to Ma. “Chinese corporates are expected to deliver mid-teen earnings growth in 2018,” says Ma, noting that new economy sectors such as internet, e-commerce, consumer and insurance will continue to witness the highest secular growth over the next three to five years.

Despite all the positive stories, risks still lie ahead for China in 2018. “There is always a chance that the cooling process happens too quickly. That could be one risk,” says Lacaille, also noting trade disputes with other countries such as the US as a potential risk.