Chinese overcapacity is raising concerns worldwide. It is easy to see why: China accounts for nearly one-third of the world’s manufacturing value-added, and one-fifth of global manufacturing exports. But there is good reason to believe that the decline of China’s manufacturing sector is imminent.

To understand what is happening now in China, it is worth recalling Japan’s recent history. After World War II, Japan’s manufacturing sector grew rapidly, thanks largely to access to the massive US market. But the 1985 Plaza Accord (which boosted the yen’s value and weakened Japanese exports), together with an ageing population and a shrinking labour force, reversed this trend.

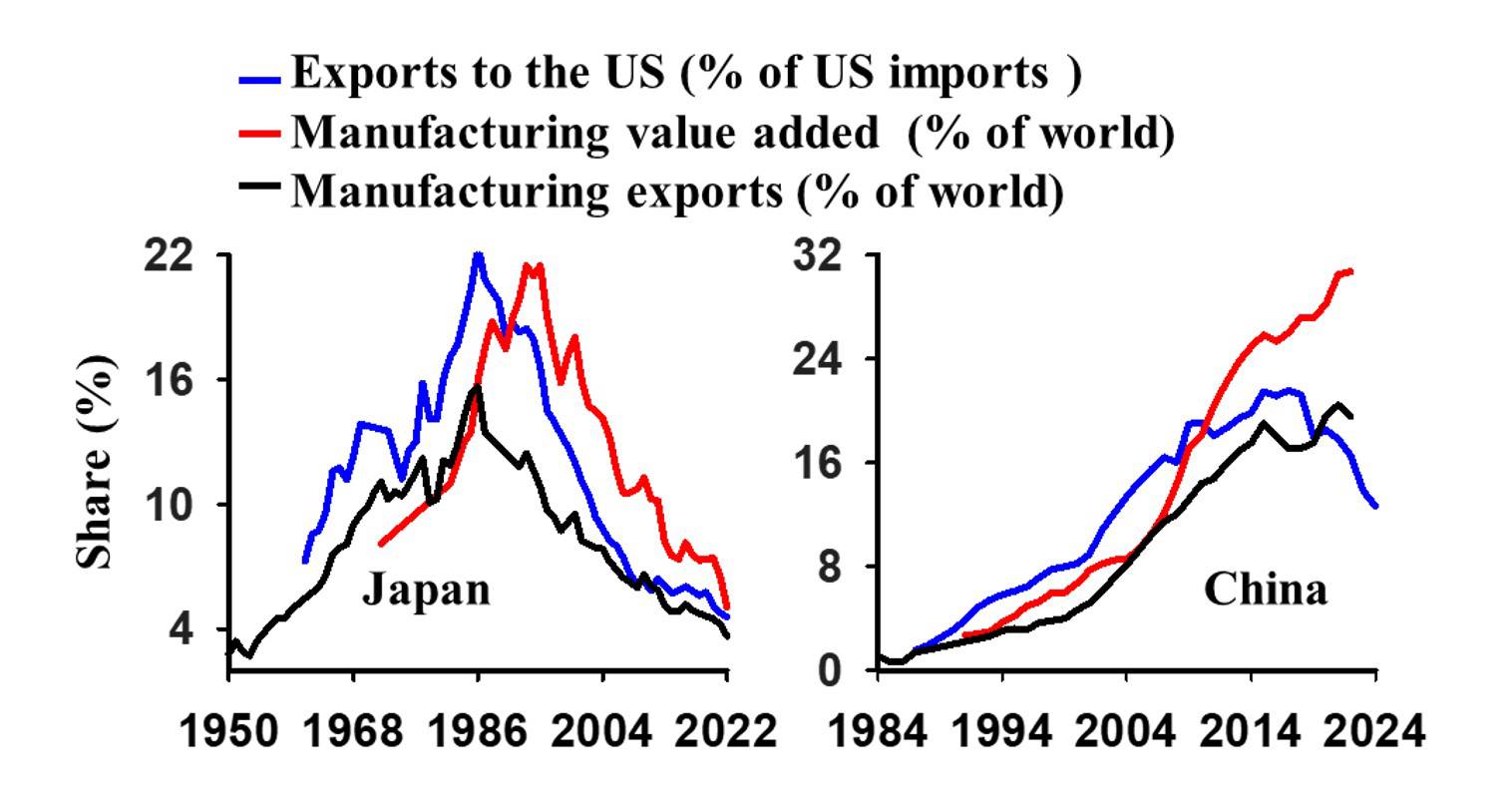

From 1985 to 2022, the share of Japanese goods in US imports dropped from 22% to 5%, and Japan’s share of global manufacturing exports declined from 16% to 4%. Moreover, Japan’s share of global manufacturing value-added fell sharply, from 22% in 1992 to 5% in 2022. And the number of Japanese companies on the Fortune Global 500 list dropped from 149 in 1995 to just 40 today.

As the chart shows, China has followed a similar upward trajectory in recent decades, but China’s manufacturing rise was even more dependent on the US market. Japan’s imports from the United States equaled 51% of its exports to the US in 1978-84, compared to a 23% share for China in 2001-18.

Source: Project Syndicate

Chinese family-planning policies are largely to blame for this imbalance. Typically, household disposable income would account for 60-70% of a country’s GDP, in order to sustain household consumption of around 60% of GDP. In China, however, the one-child policy – which was in place from 1980 until 2015 – limited household earnings, encouraged high savings, and constrained domestic demand.

As a result, Chinese household disposable income dropped from 62% of GDP in 1983 to 44% of GDP today, with household consumption falling from 53% of GDP to 37% of GDP. In Japan, by contrast, household consumption equals 56% of GDP. One can look at it this way: if wages would normally amount to $60-70, Chinese workers receive only $44 and have just $37 of spending power, whereas Japanese workers have $56 of spending power.

China’s government, however, has plenty of financial resources, which it uses to support industrial subsidies and investment in manufacturing. Moreover, because China’s manufacturing sector offers high returns, international investors are willing to channel capital toward it. Add to that a surplus of about 100 million workers, and excess capacity is difficult to avoid.

Given insufficient demand at home, China’s only option for reducing its excess capacity and creating enough jobs for its population is to maintain a large current account surplus. That is where the US comes in: the share of Chinese goods in US imports rose from 1% in 1985 to 22% in 2017. In 2001-18, the US accounted for three-quarters of China’s trade surplus.

China’s giant surplus is the mirror image of America’s deficit, and while the rise of Chinese manufacturing is hardly the only reason for the decline of US manufacturing, it is a big one. America’s share of world manufacturing exports remained stable, at 13%, between 1971 and 2000, but fell sharply after China joined the World Trade Organization in 2001, and stood at just 6% in 2022. America’s share of manufacturing value-added likewise plummeted, from 25% in 2000 to 16% in 2021.

As these trends decimated America’s Rust Belt, which stretches from Wisconsin to eastern Pennsylvania, popular frustration with globalization, and with the “political elites” who had encouraged it, grew steadily. In 2016, Donald Trump rode their frustration into the White House, vowing to revive US manufacturing and force China to change its trading practices. And Trump hopes to do the same this November.

In this sense, China’s one-child policy indirectly but profoundly reshaped the American political landscape. And now American politics are reshaping China’s economy. The US backlash against China, which began with Trump’s tariffs in 2018 and has intensified under President Joe Biden, has caused the share of Chinese goods in US imports to drop to just 12.7% in the first half of 2024.

Beyond losing the American market, China is losing some of its own manufacturing companies, which are shifting part of their production to countries such as Vietnam and Mexico to avoid US tariffs. This partial transfer augurs a wider withdrawal, much like that faced by Japan’s manufacturing sector as it fell into decline.

China is looking increasingly like Japan for two other reasons. First, its workforce is rapidly shrinking and ageing. According to the government, annual births have plummeted from 23.4 million, on average, in 1962-90 to just nine million last year, and even that figure is probably grossly exaggerated. Within a few years, China will probably record just six million births per year. Meanwhile, the median age of migrant workers, who make up 80% of China’s manufacturing workforce, has risen from 34 in 2008 to 43 last year, with the share of people over 50 rising from 11% to 31%. Some manufacturing plants are already closing for lack of workers.

Second, China’s services sector is set to squeeze manufacturing. As China’s government seeks to increase the GDP share of household disposable income, Chinese demand for US goods will rise, and some manufacturing workers will shift to services, which is also where China’s rapidly growing pool of college graduates will find employment.

The decline of manufacturing might not happen as fast as it did in Japan, because China has a larger domestic market and a more complete industrial ecosystem, and because it is investing heavily in artificial intelligence and robotics, which could deliver productivity gains. But decline is both inevitable and irreversible. Unfortunately for the US, however, this will not necessarily bring about a revival of domestic manufacturing.

Yi Fuxian is a senior scientist at the University of Wisconsin-Madison and he spear-headed the movement against China’s one-child policy.

Copyright: Project Syndicate