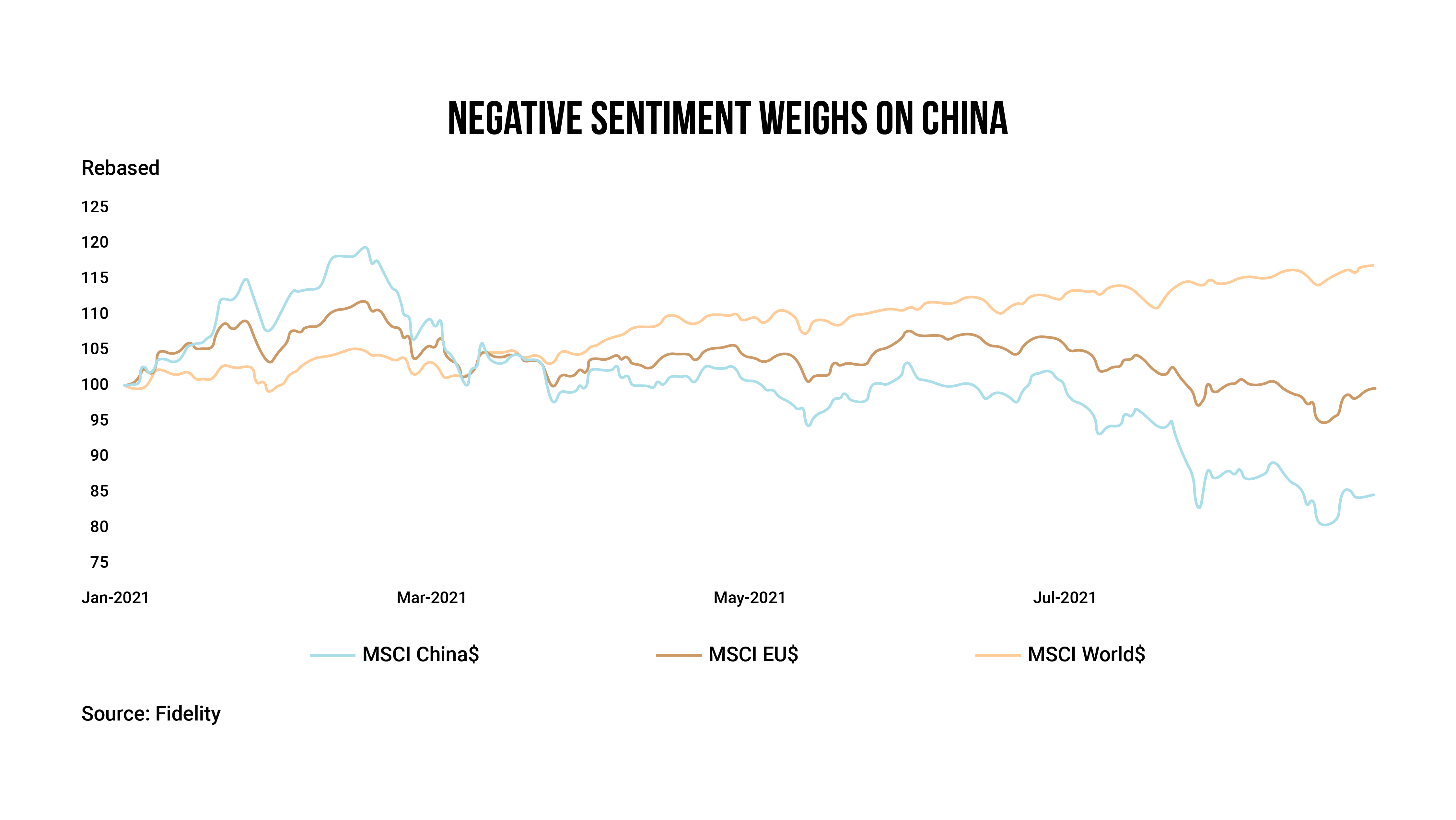

As the dust begins to settle following a series of forceful measures by Chinese regulators to redress the excess in a range of industries – from tech to property and education – intrepid international investors are starting to return.

BlackRock is accumulating Chinese assets. In its latest commentary published at the start of October, the world's biggest asset manager with nearly US$9.5 trillion of assets under management, says it has "turned modestly positive to upgrade Chinese equities to overweight as we see a gradual dovish shift in monetary and fiscal policy in response to the cyclical slowdown and anticipate that the regulatory clampdown will become less intense. We are overweight Chinese government bonds. We see the relative stability of interest rates and the carry on offer as brightening their appeal."

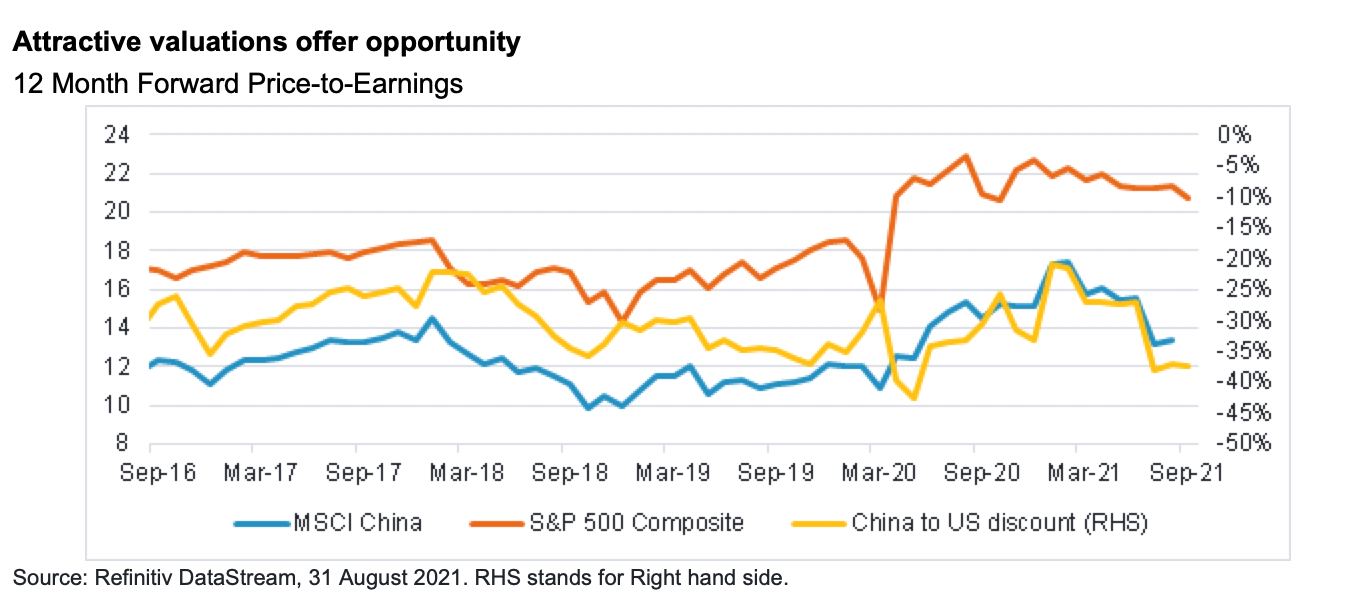

Another asset manager shares a similar view. "On the valuation of the whole market, right now for both the MSCI China and the CSI 300, the forward P/E (price/earnings) is about 12x, which is slightly below the mean. In terms of earnings, it is still double-digit. Consensus earnings is about 12% to 13% for next year. Under this kind of scenario, it is already very cheap versus historical valuations," believes Victoria Mio, director, Asian equities, Fidelity International, which manages over US$787 billion in assets.

Dale Nicholls, portfolio manager of Fidelity China Special Situations, the largest UK-China investment trust, notes that sentiment has largely taken a bigger knock than fundamentals, and corporates remain resilient in the face of change. "In terms of valuations, we are seeing many companies especially in the tech space now trading at historical low valuations, and at significant discounts to global peers. We acknowledge that there is potential for business models to change and are accordingly adjusting down our expectations around monetization levels in certain companies. Having said this, investment is all about risk-reward and for many names, this is looking favourable after recent moves."

Increased investments

A survey of 200 asset owners across North America, Asia-Pacific, Europe, and the Middle East commissioned between June and July 2021 by Invesco, which manages some US$1.5 trillion globally, revealed that 86% of respondents said their China exposure has either grown or been maintained over the past 12 months with 64% expecting further increases in the coming 12 months. Only 12% reported any expectation of a reduction.

Indeed, the hyperventilating headlines of the past weeks on China's so-called Lehman moment – a reference to the weekend in September 2008 when the iconic 164-year-old US investment bank, the 4th largest at the time, went bust as the global financial crisis escalated – and drawing a parallel to the debt woes of one of China's largest property developers, Evergrande, have been a source of puzzlement among investors active in the China market.

"Some people regarded the Evergrande crash as similar to Lehman Brother's crash, but it is a very exaggerated term," notes Edison Pun, senior market analyst at Saxo Markets. "People understand the risk of Evergrande's portfolio and it is why the bond market will regard Evergrande's as high-risk and high-yield bond."

"Investors should first understand an important fact: the real estate sector has long been a focus of the Chinese government. From 2016 onwards, it has reiterated at high-level meetings that residential properties are for housing, not for speculation," adds Winson Fong, senior portfolio manager, Greater China equities, Manulife Investment Management. "Numerous policies have since been implemented to curb real-estate speculation. This has included enforcing the three red lines policy in 2020 and 2021 to discourage real-estate speculation through excessive borrowing by developers."

Margin calls

To be sure, it is still ugly out there. Evergrande's evisceration will take some months as regulators sort through a debt restructuring plan involving thousands of supplier creditors, homeowners, and onshore investors in wealth management products. Meanwhile, the debt fallout from its missed interest payments on its offshore bonds, totalling US$15.4 billion according to BBVA Research Asia, has dragged down weaker Chinese real estate credits with Fantasia Holdings and Sinic Holdings missing coupon payments on their offshore bonds.

One head of debt capital markets at an international bank believes that for these Chinese real estate high-yield offshore bonds, among the investors who were caught in the rapid collapse of prices during the past weeks were the high-net-worth clients of private banks who were enjoying the outsized returns these bonds offered before the crisis. "There is definitely some structured unwinds going on in certain names that do stuff with Chinese dealers. Similarly, private banking margin cuts are also being felt."

"Given today's era of big data and internet technology, regulators have become much more proficient at anticipating and adapting to change," explains Manulife's Fong. "Meanwhile, the central government has been preparing the property sector for deleveraging in advance. It's also important to recognize that the real-estate developers' price-to-book ratios are at wide discounts, implying that their valuations have fully reflected the negative impact from credit crunch caused by deleveraging."

He is also unperturbed with the ripple effects to the banking sector. "The banks' overall non-performing loan provision coverage is almost 200%, a solid level far exceeding the required 120% to 150% by China Banking Regulatory Commission. We believe that there is no need to worry too much about systemic risks like those during the Lehman crisis."

Big picture

Andrew McCaffery, Fidelity International's global chief investment officer, admits there are certainly aspects that make China's new paradigm difficult for investors to navigate: the swiftness of policy actions, the regulation of what he describes as seemingly "untouchable" sectors like technology and the concurrence of fiscal and regulatory tightening. But he suggests investors should not miss the bigger picture.

"Global investors tend to fixate on the rate of China's economic growth," McCaffery continues. "But it's worth remembering that there is often a low correlation between economic growth and capital market returns. China's policymakers have adjusted their philosophy towards sustainable economic growth, rather than 'posting a high number' – this is something that global investors have yet to fully digest. Part of what has informed this latest iteration of China's economic growth strategy has been studying where issues have arisen elsewhere in the world."

BBVA Research Asia's China economist Jinyue Dong and chief economist Le Xia agree: "Despite the bluntness of policy promulgation and the lack of market communications, these measures or reforms are deployed to tackle a number of challenges faced by almost all the countries: tech-induced market monopoly, ever-widening wealth gap, global climate change, housing affordability, rising trade protectionism, etc.

Another worry is whether a policy overshoot could derail investors approach. Fidelity's Mio expounds further: "China has initiated many rounds of regulatory changes in the past and they normally last from six months to a year. The correction time period is around that. [In this current round], it started around February to March it is now six months or more into it. We are in the depths of it. We are at the second half or the last innings of implementation [which is] creating market jitters."

Dong and Xia of BBVA admit that it remains an open question whether these Chinese approaches will succeed. However, both are of the view that China's new policy direction will create new winners and losers in China.

When examining the valuation of what Mio of Fidelity describes as China's bellwether sectors such as e-commerce and the internet, valuation used to be 40x forward P/E and the lowest point was about 24x. It is now at around 26x, very close to the bottom.

"The digital economy now accounts for close to 40% of the economy from 27% five years ago, becoming the most important sector. Given China's drive towards a more sustainable economy, digitalization remains the most important driver. This is the sector where investors will continue to find opportunities. For long-term investors looking into performance drivers for the next three to five years, the China market is definitely the place to be."