Investment narratives over the last five to seven years have firmly centred around growth and quality investment styles/factors, with value and most commodities underperforming. Technology disruption, digital economy, green technologies are among the most talked-about mega-trends. Tencent was the first internet stock to be included into MSCI China 13 years ago – accounting for less than 2% of the index at that time.

Today, about half of MSCI China is made up of new-economy companies. Since the inclusion of Tencent, MSCI China has returned 117% (6% compound annual growth rate, or CAGR), while MSCI Asean has returned 47% (3% CAGR) – due in part to the growth in these new-economy listings. We believe this disparity is about to change in the economies of the ten-member Association of Southeast Asian Nations (Asean) region.

Asean is at a pivotal moment for new-economy investment opportunities. Within Southeast Asia’s population of more than 650 million, the median age in most countries, such as Indonesia, Malaysia, Philippines, is just 30 years old – and these are young and digitally savvy populations. According to a Google, Temasek and Bain & Company research report, the number of internet users in Asean has seen explosive growth, with 40 million added in 2020 alone compared to 100 million between 2015 and 2019.

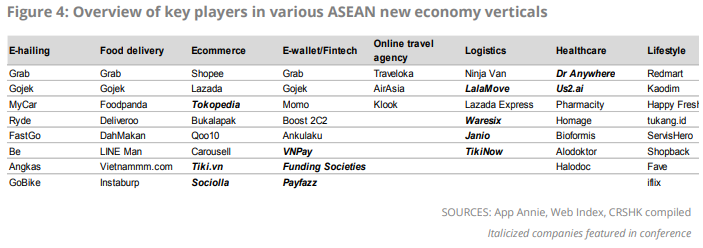

While Wall Street has largely ignored the equities market in Asean, as evidenced by over US$50 billion of foreign outflows since the first mention of quantitative-easing tapering in 2013, main street investors have been capitalizing on these digitally innovative opportunities. Private capital investment has led to a mushrooming of new-economy businesses in Asean (see below).

The new-economy bellwether SEA has stormed onto the scene and was just included into MSCI Asean in May 2021. Interestingly both Tencent and SEA rose almost 20 times from their initial public offering stock price before they were included into the index. Tencent has, since it was admitted into MSCI China in May 2008, gone on to compound at 34% growth (up 45 times).

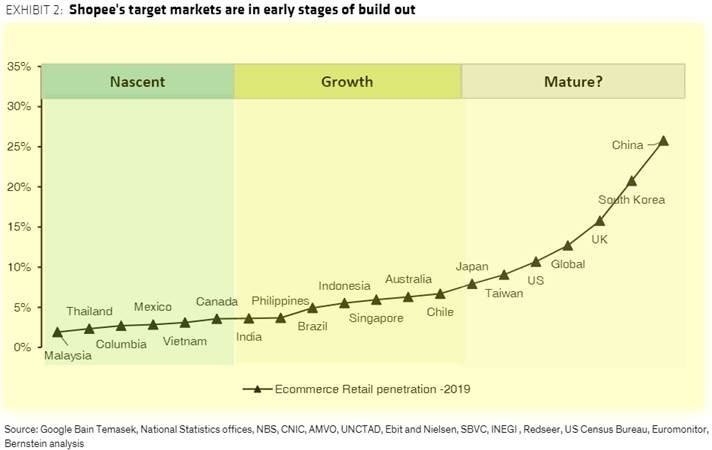

We believe that some of these new-economy businesses in Asean have the potential to deliver healthy growth over the next decade and beyond. The numbers bear it out: E-commerce penetration in Asean is still in the single digits, compared with almost 35% for China already (see below).

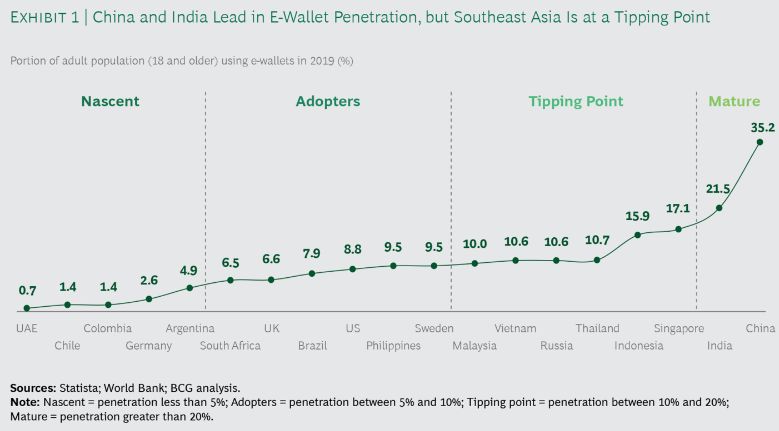

Meanwhile, Asean’s digital payment revolution is also awakening to transform the region into the next bright spot (see below).

Covid-19 has fuelled the take-off, while strong government push from several of the nations in Asean is supportive and will be integral to scaling it higher.

There are several sizeable unicorns which will potentially list over the next 12 months, including Grab, GoTo and Bukalapak. It is projected that the Asean internet economy will triple to US$300 billion by 2025 (Google, Temasek and Bain & Company).

These large unicorns are well-placed to capture a large share of that growth, given their ambitions to be super-apps cross-selling multiple products and services. These listings will mean that new-economy representation within Asean markets will go from close to zero just 12 months ago, to potentially over 20% in 12 months’ time. Our experience rhymes with China, but Asean is moving at an accelerated pace.

A digitally savvy young population coupled with technology, both as a disruptor and an enabler, has far reaching implications for old-economy sectors too. Tomorrow’s winners will be old-economy companies that turn disruption into opportunities. In Asean, one of the structural growth drivers is the rise in financial penetration.

Three out of every four adults in Asean are either unbanked or underbanked. Rising digital adoption is helping to accelerate financial penetration and well-run incumbent banks have embraced these digital trends to deliver new value propositions that are attuned to today’s consumer needs. At the same time, we see scope for new players to innovate and proliferate.

Decarbonization is another mega-trend for the next decade. Today, close to 70% of global GDP has a net-zero emissions pledge. As countries move from pledges to action, green capex will and must accelerate. This is of great relevance to Asean too. Carbon transition investment opportunities in Asean exist in three broad categories:

- utility companies that are proactive in shifting their energy generation mix to renewables

- technology companies with core competencies that benefit from rising electric-vehicle/clean-energy adoption, and

- globally competitive providers of raw materials for green capex.

In conclusion, Asean’s structural merits – favourable demographics and growing domestic consumption, among others – have not translated fully into stock market performance of late, as some of the fastest-growing businesses were not listed. This is changing rapidly. The growing representation of listed new-economy stocks in Asean’s public markets, coupled with the nascent turnaround in the old-economy sectors as the region recovers from Covid-19, means that Asean equities as an investment class can no longer be ignored.

Pauline Ng is the portfolio manager of JPMorgan Asean Fund.