FOR China’s LGFV (local government financing vehicle), 2019 was supposed to be the watershed year. It prompted a speaker at The Asset’s 13th Asian Bond Markets Summit held in Chengdu last May to remark that “there was a shift in sentiment among international investors allocating towards LGFV bonds”. And then Covid-19 emerged.

As offshore US dollar liquidity dissipated with investors switching to high-grade credits, the situation has taken a U-turn. In April, offshore LGFV bond issuance totalled US$800 million, which is 75% less than the US$3.2 billion raised in April 2019. During the first five months of 2020, total issuance dropped 27%, to US$6.1 billion, compared to the same period in 2019, according to Moody’s Investor Service data.

With offshore conditions difficult, LGFVs looking to raise finance have pivoted onto the onshore market. A number of investors The Asset spoke with anticipated this development at the height of the Covid-19 outbreak in China earlier this year. Indeed, issuance hit a record high with Chinese LGFV issuers raising 1.06 trillion yuan (US$149.8 billion) in Q1 2020, up 23% from Q1 2019 figures.

“For the first five months of this year, the total was still up 31% compared with the same period in 2019 despite slowing momentum in May,” explains Sarah Xu, assistant vice-president and analyst at Moody’s. “We expect more onshore issuance in the rest of the year as China plans to increase infrastructure spending.”

Domestic credit easing measures from Chinese regulators has helped, countering the negative effects of Covid-19 in the onshore market. Furthermore, the prospect of increased infrastructure spending from the government bodes well for Chinese LGFV issuers.

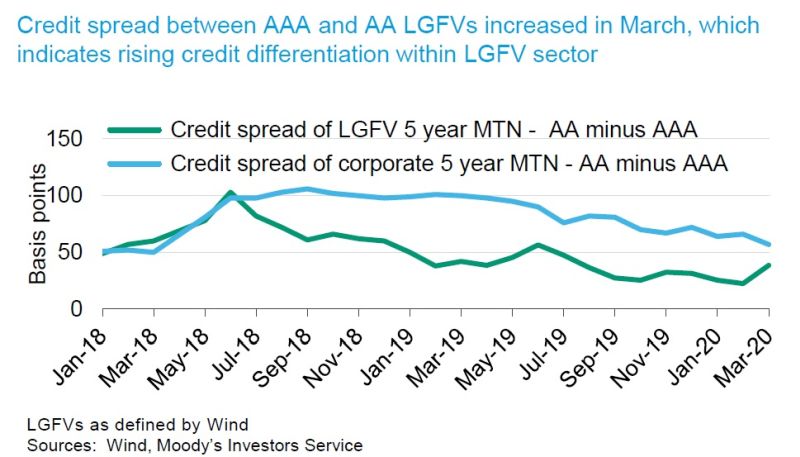

The pandemic has also increased onshore credit differentiation. Credit spreads, for example, widened between AAA and AA rated Chinese LGFVs in March 2020, Moody’s data indicate.

Covid-19’s impact on LGFVs’ access to finance has also been uneven. The eastern provinces of Jiangsu and Zhejiang continued to represent the bulk of LGFV issuance activity in Q1 2020. On the other hand, northeastern provinces such as Jilin, Heilongjiang and Liaoning managed to raise 9.4 billion yuan in Q1 2020, a 61% reduction compared to the same period last year.

Recent regulation on Chinese local government financing has sought to provide flexibility to those entities severely impacted by the economic effects of Covid-19. On June 17, the Ministry of Finance issued a new circular stating that guarantees from Chinese local governments toward international finance organizations such as multilateral organizations and foreign governments (e.g. in the form of panda bonds) will not count for the local government’s total debt quota.