AS foreign investors begin to increase their holding of Chinese A-shares in the run-up to their inclusion in the MSCI Emerging Markets Index in June 2018, international brokerages are also beefing up their coverage of Chinese A-shares to be able to service these fund managers.

In early December, HSBC Global Research expanded its Asian research offering following the launch of HSBC Qianhai Securities, the first Chinese securities joint venture to be majority-owned by a foreign bank.

This followed the announcement by China’s Ministry of Finance that it would lift the maximum holdings limit for foreign partners in onshore securities joint ventures from 49% to 51%. It is likely that international players will continue to deepen their onshore research capabilities in China’s 62-trillion-yuan (US$9 trillion) A-share market and 69-trillion-yuan onshore bond market.

Apart from HSBC, there are seven other securities companies with foreign ownership in China, including Goldman Sachs Gao Hua Securities, UBS Securities and Citi Orient Securities. At least 18 new joint ventures await approval from China Securities Regulatory Commission (CSRC).

The A-share inclusion in the MSCI index is much anticipated given that China is the last remaining large market where the participation of foreign investors remains restricted. Foreign investors hold just US$151 billion – less than 2% of the total market capitalization.

While the introduction of fundamental or technical strategies will become more prevalent as more institutional investors become active in the A-share market, this early, the best strategy may simply be following the so-called National Team (国家队).

In sectors with national significance, such as finance, state-owned investment companies are the major owners. The shareholding structure in the National Team, which comprises Central Huijin Investment (中央汇金投资有限责任公司), China Securities Finance Corporation (中国证券金融股份有限公司), Wutongshu Investment (梧桐树投资平台) and other state-owned asset managers, is sometimes interpreted by equity analysts as the government’s A-share investment strategy.

China Securities Finance Corporation’s shareholders include all major stock exchanges in China, while Central Huijin Investment is indirectly owned by the Ministry of Finance. Wutongshu Investment is under the State Administration of Foreign Exchange.

Given its state background, the National Team plays a clear role in stabilizing the market using a rather simple ‘buy low, sell high’ strategy. A few months following the A-share crisis in 2015, the National Team increased their A-share holdings to 6% of the total A-share market cap.

For both alpha-seeking and passive investors, tracking the portfolio of the national team can be worthwhile in an active A-share market. The quarterly changes in holdings indicate short-term views on certain sectors, while more permanent holdings suggest the nation’s long-term strategy.

Astute investor, Jim Rogers, co-founder of the Quantum Fund, looked at the National Team portfolio when investing in the A-share market. In an interview with Chinese media in 2015, Rogers said there was a good chance of a good return if you follow the National Team’s investments.

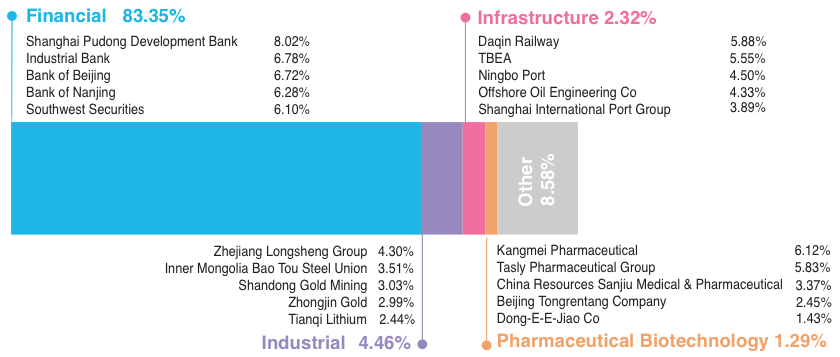

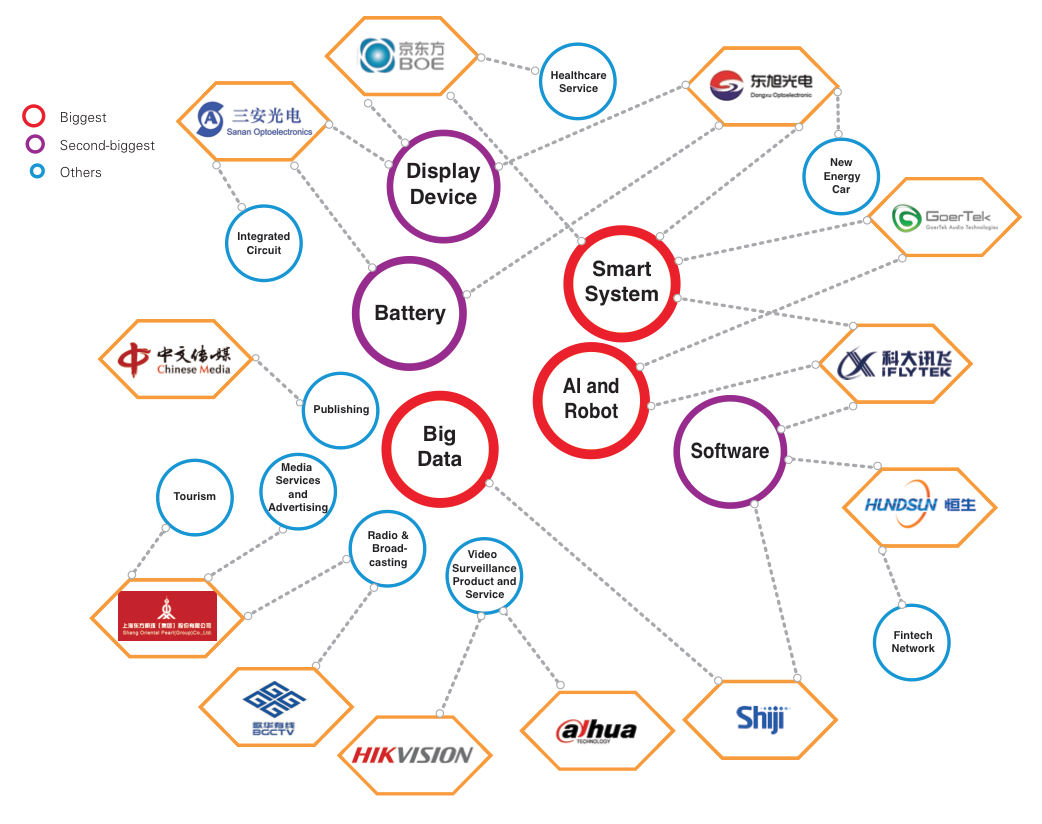

According to Sinolink Securities, the National Team held 4.43 trillion yuan in A-shares as of Q3 2017, accounting for 7.23% of the total A-share market cap. Financial stocks are still largest in the National Team’s A-share portfolio. In addition, the State Council issued an official plan on artificial intelligence (AI) in July 2017, and technology companies with big data and AI capabilities are now also in the National Team’s investment portfolio. For instance, as of Q3 2017 Central Huijin is the sixth-largest shareholder in IfLytek, a leading AI company in China.

Noticeably, China’s pension fund, the National Social Security Fund, also entered the A-share market in 2017. Yet, market data show that the strategy for the pension fund in 2017 was to invest in initial public offerings.

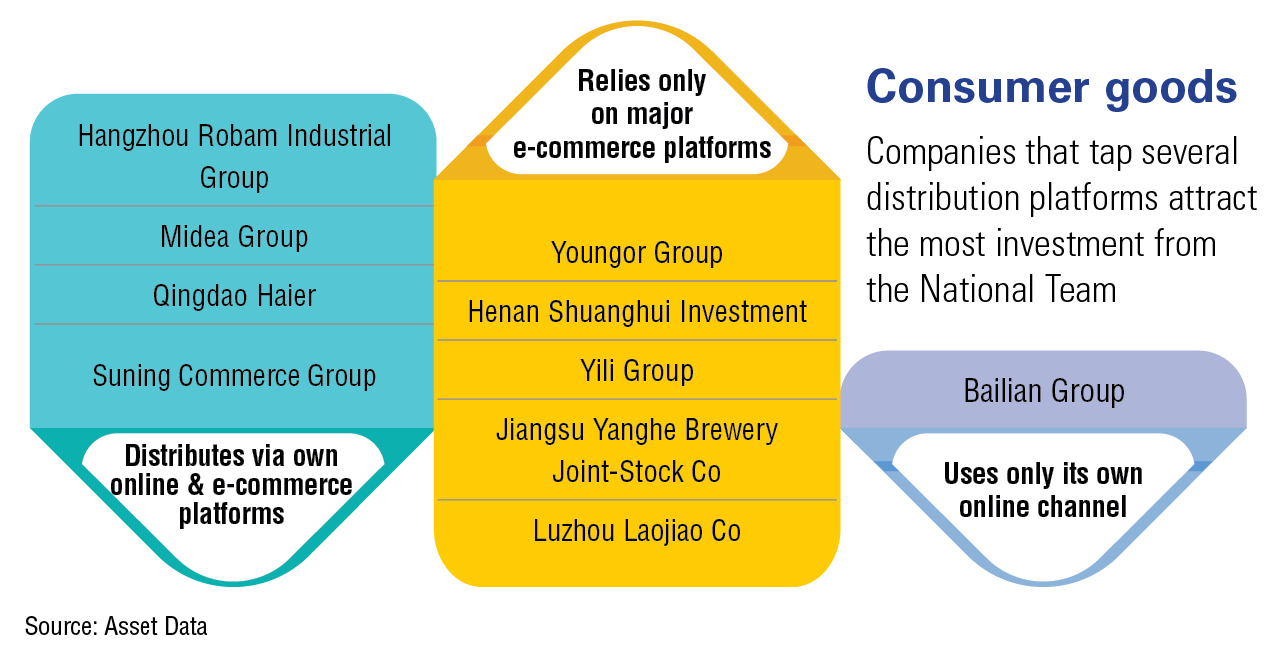

In addition to state investment, cross-shareholding among different state-backed listed companies should also be noted. Specifically, insurance companies appeared in the top 10 shareholders lists in 11 out of 26 listed banks as of Q3 2017, suggesting strong confidence in the long-term returns of Chinese banks. In the technology, media and telecoms (TMT) sector, Suning Commerce Group, in which the National Team has a stake, was largely held by Taobao, the largest Chinese e-commerce platform. Suning sold US$940 million worth of shares in Alibaba in December.

Although the valuation of listed companies will not necessarily change when the shareholding structure changes, it may provide some clues to the state’s future direction and strategy. In August, state-owned China Unicom, the third-largest telecom company in China, announced it sold shares to investors including Alibaba, Tencent and Baidu under plans to bolster its technology capabilities. The proceeds will be used for China Unicom’s 4G and 5G businesses.

Foreign interest

Foreign ownership of A-shares is expected to grow by 10% over the next five to 10 years, according to Chinese security firm CICC, with net inflows amounting to 200 to 400 billion yuan yearly. As foreign ownership remains small, this represents a huge opportunity for growth.

In particular, European insurance and asset management companies are looking to enter China’s A-share market in 2018. “There are some structural reasons behind the growing interest of our clients in A-share market. It is not just about the net profit growth,” says Anthony Wong, portfolio manager at Allianz Global Investors. “It is a natural trend that overseas investors are flocking to the A-share market.”

China Merchants Securities estimates that as of Q2 2017, institutional investors already took up 29% of the outstanding A-shares. In a sign that the market is maturing, investors including pension and mutual funds have helped internationalize A-shares.

However, to foreign investors, China continues to be unknown, unstable and volatile. The memory of the 2015 A-share crisis still lingers, when unprecedented herding was witnessed and the Shanghai Stock Exchange Composite Index dropped from the 5000-level to below 3000 in just six months. Massive margin cuts from A-share brokerage firms were believed to be the major cause of the market collapse.

Yet, CSRC continued to crack down on illegal stock pledging and lifted the minimum requirement for legal margin trading, and leverage in the A-share market was controlled. Data from Chinese financial media firm Eastmoney show that the outstanding margin growth has been steady over the past 12 months without excessive volatility.

Another hesitation that investors have is due to the heavy participation of retail investors, many of whom know little about finance. According to Haitong Securities, retail investors accounted for over 40% of A-share trading volume. In comparison, the proportion is lower than 10% in Hong Kong’s H-share market.

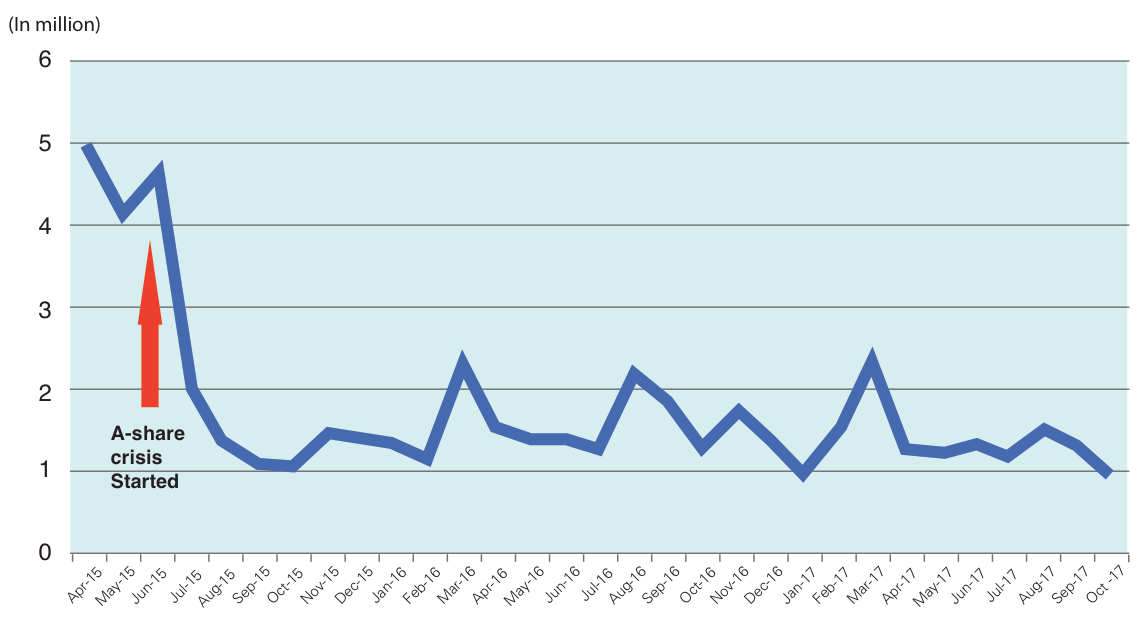

Some believe that the over-participation of retail investors adds to market volatility. Data from the China Securities Depository and Clearing Corporation show that just a few months prior to the crisis in 2015, retail investors opened millions of new A-share accounts. However, this has now mostly been addressed. According to the agency, account openings have dropped and remained stable over the past 12 months.

Reforms

The opening of China’s markets continues at a steady yet inevitable pace. Schemes such as the Qualified Foreign Institutional Investors (QFII) Scheme and Renminbi Qualified Foreign Institutional Investors (RQFII) Scheme, grant limited access to China’s markets with restrictions such as trading quotas.

China widened foreign investors’ access to A-shares through the Stock Connect. The scheme allows investors trading on the Shanghai and Shenzhen exchanges to buy shares on the Hong Kong exchange (known as southbound trading), and investors on the Hong Kong exchange to buy those listed in Shanghai and Shenzhen (known as northbound trading).

Although overseas investors remain generally wary of the A-share market, China’s reforms plus the country’s strong fundamentals have put A-shares back on investors’ radars.

Ongoing reforms in the equity market now encourage increased participation from individual investors. President Xi Jinping, in his 19th party congress speech, cited the growth of “direct financing”, which refers to government efforts to encourage quality listings in the market.

Moreover, in November 2017, Yaqing Xiao, director of State-owned Assets Supervision Administration Commission, said in a meeting that it will welcome more private sector participation in buying shares of SOEs as part of its reforms.

Public listed companies are required to disclose their shareholding structure in China. In a bid to further enhance the level of information disclosure, Shenzhen Stock Exchange launched the Chinese and English snapshot of listed companies for northbound trading under the Shenzhen-Hong Kong Stock Connect in late December.

The snapshot contains 12 major areas including basic information, business summary, price performance, highlights, trading information, directors and executives, top five shareholders, operating revenue, investment risks, dividend data, per share data and major financial data in financial statements. The contents and data are mainly from the periodical reports disclosed by listed companies.

Growth

Furthermore, along with continuous reforms, growth remain healthy, and it is the rise of China’s new economy companies which is driving investor interest in Chinese stocks, despite their high valuations. Analysts expect a bright future for TMT companies.

“In a high growth country or market, we are looking at the PEG ratio, comparing the price to earnings (P/E) and the profit growth,” says Wong. “If you look at the new economy companies, their P/E must be higher than old economy companies, like telecommunications. That justifies why we buy high growth companies with reasonable P/Es.”

Compared to Hong Kong stocks, the P/E ratio of listed companies is still higher in the A-share market. Yet, the robust southbound inflow from the stock connect programmes has not only made the H-share market one of the best performing equity markets in the world in 2017, but also narrowed the valuation gap between the H-shares (Chinese companies listed in Hong Kong) and A-shares.

As of the end of November 2017, the P/E of Shanghai Stock Exchange is 18.1 while the P/E of Shenzhen Stock Exchange is 36.63. The valuation is relatively higher in Shenzhen driven by the new economy companies, including TMT stocks.

Specifically, large cap-stocks have benefited from the growing interest from institutional investors. As of November 30, CSI 300 index, which tracks blue chips such as Kweichow Moutai, Hangzhou Hikvision Digital Technology and Midea Group, has increased by 21% YTD.

The growth is consistent with National Bureau of Statistics’ profit data for industrials. In the first 10 months of last year, industrial firms posted a 23.3% year-on-year increase in combined profits. State-owned enterprises recorded a 48% profit growth in the same period.

Financial and consumer sectors are the most favoured by foreign investors. As of Q3 2017, the top five stocks held by QFII in terms of market cap, starting from the most popular, are Bank of Beijing, Kweichow Moutai, Bank of Nanjing, Midea Group and Wuliangye.

With the impending inclusion of A-shares in the MSCI index, the size and growth in China’s A-share market, as well as the steady pace of reforms and increased foreign participation, could bring ample opportunities for investors. For those looking to win in the A-share market, following the National Team may be a future you can bet on.

.jpg)

.jpg)