Like most SMEs, small and mid-sized Chinese firms face challenges to churn their operating cash flow. Often, they run short. Banks are not necessarily able to support them on a standalone basis. This problem gave birth to supply chain finance, which has become one of the stable sources of revenue for transaction banks.

.png) The next iteration of supply chain finance is now taking shape in China. The lightning speed with which e-commerce is growing in the mainland coupled with robust payment systems are making it possible to collaborate with banks.

The next iteration of supply chain finance is now taking shape in China. The lightning speed with which e-commerce is growing in the mainland coupled with robust payment systems are making it possible to collaborate with banks.But e-commerce is still largely based on consumers rather than B2B (business-to-business), an area that holds considerable promise. It is one of the motivations behind Alibaba’s decision to approach China Merchants Bank (CMB) to collaborate on how to encourage big businesses onto their platform. This makes sense as thousands of suppliers now are using Alibaba’s sourcing platform, 1688.com.

“In China, it is rare that a supplier decides how payment is made. It is still mostly determined by buyers,” says William Fang, business director of enterprise, sourcing and procurement at 1688.com in an interview with The Asset.

“We’ve been getting feedback from our members. They hope to see details of each of their procurement transactions on our platform. For example, how much money they have paid each morning,”says Fang.

Following some brainstorming, CMB, one of the largest privately-owned banks in China, agreed to provide a mechanism to address the needs of large buyers. CMB introduced into the structure its B2B bills pool (B2B票据池) that collects the bank acceptance bills (BABs), also known as bank acceptance drafts (BADs), from member companies.

Following some brainstorming, CMB, one of the largest privately-owned banks in China, agreed to provide a mechanism to address the needs of large buyers. CMB introduced into the structure its B2B bills pool (B2B票据池) that collects the bank acceptance bills (BABs), also known as bank acceptance drafts (BADs), from member companies.“In 2015, Alibaba came to us (with a plan). Initially, we thought the idea was good but complicated because it is actually a ‘bill version’ Alipay,” recalls Wei Wu, product manager at CMB. “Compared to cash payment, the bill payment introduced more elements. It was difficult, but after several rounds of discussion, we decided to do it. After seven to eight months, we launched it and expanded nationwide,” Wu tells The Asset.

So far, over 100 large conglomerates have used the B2B bills pool service. In the past, e-commerce B2B platforms allowed only cash payments between two parties via Alipay, which is not a common payment practice used by most large buyers. The B2B bills pool made non-cash payment to SMEs possible. For both CMB and Alibaba, this was a breakthrough. Indeed, this is the first time Alibaba is involved in a supply chain finance solution working with a bank.

By uploading BABs onto Alibaba’s platform, SMEs that are also members of Alibaba are able to quickly receive payments via CMB’s acceptance bills with a corresponding amount of funds without pledging any assets. To activate the B2B bills pool service, Alibaba members are only required to submit an application form together with the additional documents required by CMB.

“The payment is different from traditional e-banking payments in the sense that B2B platforms connect its data with the order information. The order information can directly act as proof of trade,” says Wu. “In the future, the secured payment model can help platforms like Alibaba to balance the needs of buyers and sellers. That addresses the trade disputes and lack of trust in China to some extent.”

“That is also how we are trying to help large enterprises with their transition to the ‘Internet plus’ platform. The main objective is to help the supply chain for those enterprises to evolve together with our platform,” says Fang.

Growing importance of e-commerce

This innovation in supply chain finance is in line with the digitization trend in China and supported by the government. In particular Circular No. 224, issued by the People’s Bank of China in September, simplified financial institutions’ review process of e-commerce enterprise applications of guarantee for commercial acceptance bills. The new regulation opened up an opportunity for banks to introduce innovative services by working with Chinese e-commerce platforms.

This innovation in supply chain finance is in line with the digitization trend in China and supported by the government. In particular Circular No. 224, issued by the People’s Bank of China in September, simplified financial institutions’ review process of e-commerce enterprise applications of guarantee for commercial acceptance bills. The new regulation opened up an opportunity for banks to introduce innovative services by working with Chinese e-commerce platforms.

“The e-commerce market in China is transforming from an oligopolistic B2C (business-to-consumer) market to an era of monopolistic competition in the B2B market. In light of the supply side reform supported by the government, traditional corporates are urgently looking for transformation,” says Wu. “B2B platform, as a solution, can reduce intermediaries involved in the transactions that can improve (overall) efficiency and reduce cost. That’s why many industries consider e-commerce as an industry upgrading strategy.”

By partnering with banks, e-commerce platforms are starting to play a role in offering working capital solutions to SMEs. China’s e-commerce companies such as JD.com and Alibaba already have their own supply chain financing platforms. “Even if we don’t have 1688.com today, our treasury and payment platforms are still complete and comprehensive. And they will not be restricted by other factors,” says Fang.

By partnering with banks, e-commerce platforms are starting to play a role in offering working capital solutions to SMEs. China’s e-commerce companies such as JD.com and Alibaba already have their own supply chain financing platforms. “Even if we don’t have 1688.com today, our treasury and payment platforms are still complete and comprehensive. And they will not be restricted by other factors,” says Fang.“It (the product) effectively empowers the e-commerce platform to evolve from a data platform to a trading platform. This is the future of the big data platform where you can further explore the potential of financial services. It also helps Alibaba to complete its ecosystem,”says Wu.

Traditional e-commerce players are exploring their offline models by working with retailers. To illustrate, Alibaba announced a partnership with Bailian Group, a Shanghai-based retailer, in February last year. The e-commerce giant also invested in Suning, the leading retailer in China. Another e-commerce leader JD.com announced in its 2016 annual report that Wal-Mart Stores Inc, the world’s largest retailer, increased its holdings in the company to 12.1%. According to JD.com, supply chain management is the core area of the collaboration with the US retailer.

“As e-commerce booms in China, the era of pure e-commerce will end. It will cease to exist in 10 to 20 years’ time. That means the integrated structure consisting of the online and offline business as well as logistics will give rise to the new retail model,” said Jack Ma in a speech at a conference in Hangzhou in October.

For banks, this is both an opportunity and a challenge. “Alibaba can make a payment in two seconds, which is much quicker than our payment system,” says an executive at a European bank. “It takes two days for us to make a payment. We are not on the same level.”

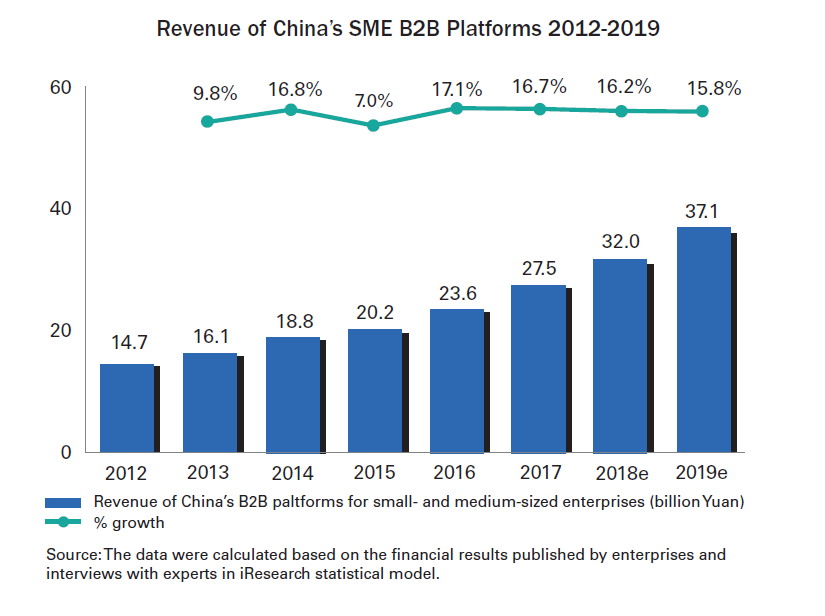

Chinese B2B platforms are expected to benefit from the new supply chain solution. According to the latest data from iResearch, the revenue of China’s B2B platforms for SMEs totalled 23.59 billion yuan (US$3.5 billion) in 2016, up 17.1% from 2015.

According to iResearch, China’s SME B2B e-commerce market is still dominated by Alibaba. The e-commerce giant, together with the main players, accounted for 70% of the market. In 2015, total transactions through China’s online B2B market totalled 12 trillion yuan. The market is expected to grow 20% annually over the next few years.

“Alibaba’s solution is actually a blueprint (for supply chain finance),” says Wu. “A lot of B2B platforms came to us because they saw the success of this product (B2B bills pool).”

For Alibaba, the search for innovative ways to improve its services continues. “As an e-commerce platform, we hope to serve more traditional corporates. From advertisement to marketing, we plan to deliver our service to their procurement and then create more synergy from the collaboration,” says Fang.

.jpg)

.jpg)