If 2016 saw the flowering of Chinese investors buying US dollar bonds of Chinese issuers – the so-called China bid – 2017 could mark the emergence of their long march to become a force in the global bond market. To understand what is behind this trend, China Zheshang Bank’s (CZBank) investment activity sheds some light.

Listed on the Hong Kong Exchange last year following its US$1.7 billion initial public offering, CZBank is among the 12 nationwide joint-stock commercial banks in China. Despite its modest size with total assets of US$172 billion as of June 2016, the bank headquartered in Hangzhou typifies a segment of the Chinese investor community that is becoming prominent in the G3 bond market.

“Our foreign currency bond investments are not limited to China,” Liu Xiaochun (), vice-chairman and president of the bank tells The Asset. “This year, we are exploring other countries for dollar bond trading opportunities.” Liu, who until a few years ago was the general manager of the Hong Kong branch of Agricultural Bank of China (ABC), has worked in the international business department of ABC both at the head office in Beijing and also at its Zhejiang provincial branch.

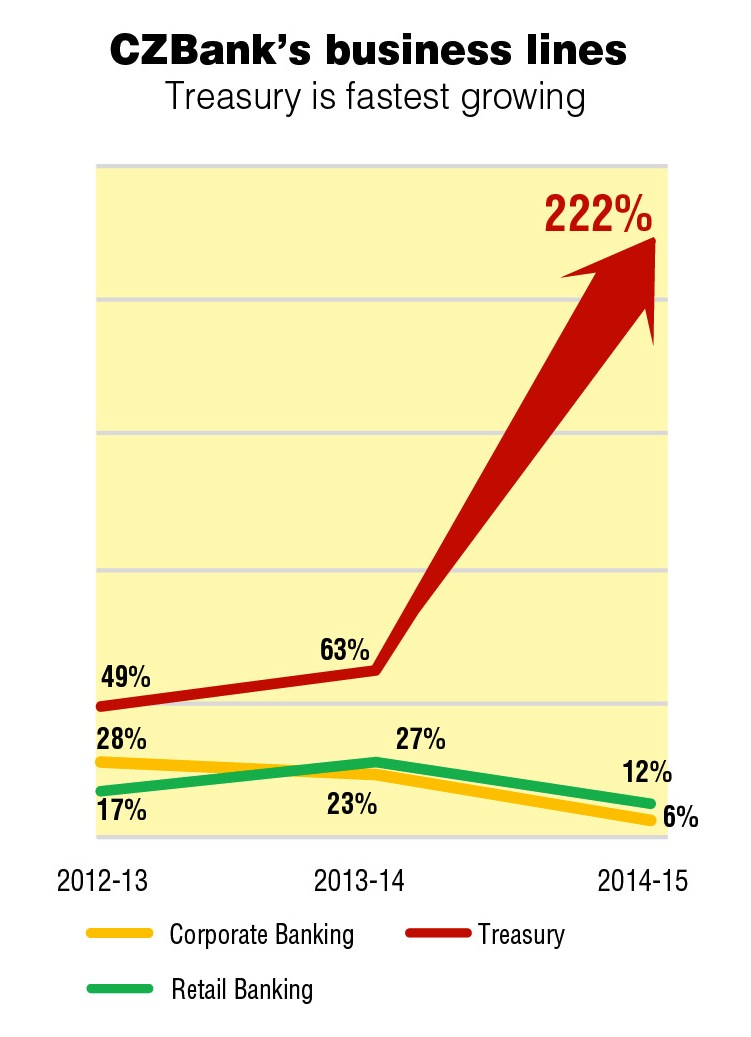

CZBank has seen a quantum leap in its treasury business, which comprises its money market activity, investment in bonds and other financial assets, foreign exchange and derivatives trading and treasury business conducted on behalf of customers. In 2015, operating income from treasury reached 9.8 billion yuan (US$1.4 billion), which is a 680% jump from the level of 1.2 billion yuan in 2012. The share of treasury business to total operating income has likewise grown from 12% to nearly 39% by end of 2015.

Within the bank, Liu says it is the bank’s financial markets department that is responsible for its G3 bond-related investments and transactions. “The department handles all investment management and is now engaged extensively in domestic and foreign bonds, FX, precious metals, commodities and various types of derivatives trading,” he adds.

At the moment, the ratio of investment invested in bonds issued by Chinese companies, including state-owned enterprises and private enterprises, is around 60% of the total investment. He attributes this to a few factors. “Bonds issued by Chinese companies ranked first in the bond market issuance in Asia,” he points out. As a Chinese bank he believes the institution has a better grasp of information of the Chinese enterprises. “For some enterprises our focus is on the development of bilateral relations and cooperation through bond investment.”

Unlike other Chinese investors, Liu takes pride in CZBank’s proprietary trading strategies, which he says is more flexible. “We are very active in market trading and we do not only trade bonds in Asia. The portfolio management is also more meticulous – we use bond options, interest rate swaps and swapping options to dynamically manage the complex and volatile market risks ensuring the stability of investment profit.”

In evaluating the risk-adjusted return of bonds in its portfolio, the bank focuses on three factors: internal FTP cost, credit risk and market risk costs. The returns are then adjusted based on all three factors.

When investing in G3 bonds, Liu says the bank will review the target company and its debt ratings taking different strategies based on them. “For example, high-rated bonds have a higher sensitivity to the market interest rates and so we are focusing on macroeconomic analysis.

For high-yield bonds, we are focusing on fundamental data and the prospect of the company instead. Market liquidity is also a factor depending on the market situation. If there are trading opportunities in the short-term, we will also trade accordingly for capital gain. On the whole, the bank prefers the target companies to have good fundamentals and ratings, which makes us a conservative investor.”

Ratings from reputable credit rating companies, he believes, are important references for the bank’s bond investment. “They are also for market investors to distinguish between investment-grade bonds (BBB-and above) or high yield bonds (BB+ down to no rating).”

He describes ratings much like a threshold to guide the bank’s clients. “If the threshold is too high, it is hard to enter, which will easily turn guests away. In order to facilitate the guests, we set the threshold low. We also have a concierge, who is responsible for identifying the visiting guests. This is our thinking towards credit product investment. In practice, we set the threshold as BB. The choice of bonds is focused more on the different trading strategies.”

There are no constraints on how long the bank should hold on to the bonds. “Our investment and trading value more the types of bond and the investment value of the bonds. For the bonds with shorter maturities, i.e. within three years, with lower interest rate risk and good return ratings, we tend to hold until maturity. As for bonds with longer maturities, we will back them up with relevant hedging tools or band trade according to the market situation.”

In terms of the types and tenors, Liu says the bank invests in bonds with moderate maturities averaging five years. “From the perspective of risk control, the industries of the issuers of the bonds we hold are relatively diversified. There is not one dominant industry.” In the case of domestic bonds, for example, the bank has recently focussed on those issued by the top four asset management companies.

In the case of foreign bonds, Liu says the bank is studying opportunities to invest in issues in places such as the Middle East, India and Australia. “The main reason is that commodities had a sharp correction over the past few years leading to the high possibility for the price to bounce back in the future, which benefits issuers from these areas.” He also points out the bank’s interest “to increase stakes of sovereign or corporate bonds in places such as Saudi Arabia and Brazil.”

Looking into the future, Liu says interest rate risk is a concern. “Market interest rates [have] continued to rise not only because the major developed economies are gradually withdrawing from easing their monetary policy (or less easing), but also the forecast of inflation from infrastructure [expenditure] after Donald Trump’s coming to power.”

He says the pace of Fed rate hikes and the changes in other major economies present considerable uncertainty. He expects the risk-free interest rate is on a rising trend for a certain period.

Facing the uncertainty in 2017, the strategy is to shorten the bond holding duration for asset allocation and mainly focus on short-term debt. “At the same time, we will be increasing short-term high yield bonds and financial bonds, which performed relatively stable in allocation. Meanwhile, we will continue to purchase investment-grade bonds at a lower price at the right time by paying attention to whether there is a market overreaction.”

.jpg)

.jpg)