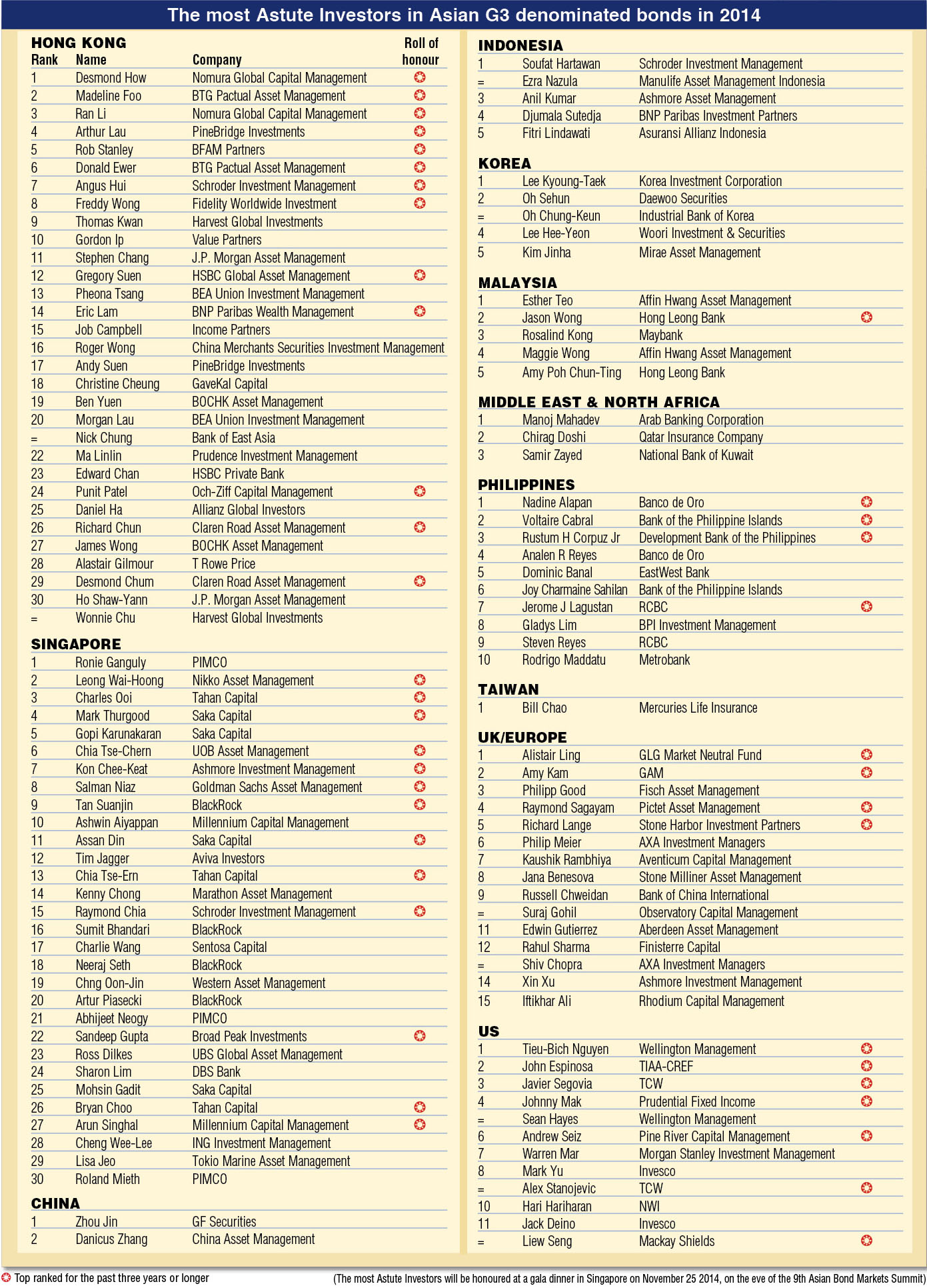

We asked Astute Investors to give their outlook for the Asian G3 bond market in the next 12 months on a scale of most negative to most positive. The 26 top-ranked Astute Investors gave the rationale behind their forecasts

|

Hong Kong

Desmond How

Nomura Global Capital Management

Positive

|

|

The JPM Asia Credit Index (JACI) returned 7.8% to date this year, outperforming every sell-side strategists’ expectations. The surprise element has been the US treasury rally as global growth stalled, enabling easy monetary policies. JACI spreads indeed only tightened by 5bp from the year’s start. As a result, investment grade credits (+ 8.2%) which have longer duration on average, outperformed high yielders (+6.5%). In fact, high yield (HY) widened 50bp, dragged down by Indonesian/Mongolian coal and Chinese property sectors.

Into the next year, investors will continue to worry about treasury volatility, credit deterioration and possibly higher default rate. Nonetheless, spreads are still one-third off the cycle tights; at current 260bp for an average high BBB rating, JACI overstates default probability and instead prices high market risk. I believe a diversified portfolio of investment grade and high yield bonds would adequately compensate strategic investors into 2015.

|

Arthur Lau

PineBridge Investments

IG – Positive;

HY – Neutral to negative

|

|

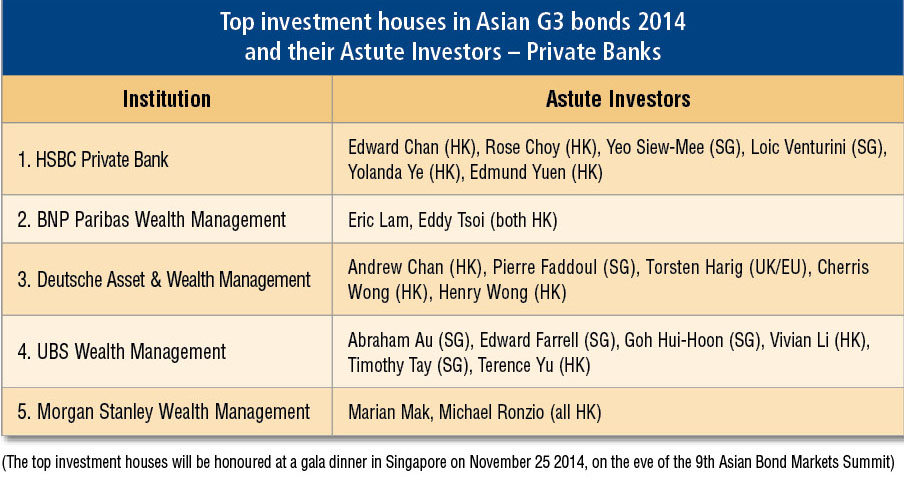

| Top investment houses in Asian G3 bonds 2014 and their Astute Investors – Private Banks (Click to enlarge) |

In investment grade (IG), with expected high US treasuries and benign credit spread outlook, we believe absolute yield levels will be increasingly attractive to investors. High yield overall is neutral to negative depending on the sector. The credit matrix in HY sectors is likely to deteriorate, e.g. profit margins expect to narrow, sales turnover growth is moderating, asset quality is likely to decline etc. The commodities sector will continue to be under pressure, while property sector in China will continue to face industry consolidation and funding challenges.

Rob Stanley

BFAM Partners

Positive

An increase in idiosyncratic risks marks this part of the credit cycle and we expect that there will be plenty of decent trading opportunities across the credit spectrum. We have already seen the start of the credit differentiation with names like Citic Pacific and 1MDB repricing tighter, while in HY, the coal sector and more recently Agile’s bond price collapse following the detainment of the chairman, also evidenced disparate valuation moves. Near-term, we see a tangible risk of a sharp broad-based correction, but this should present broader beta opportunities as deflationary pressures keep USD rates low and demand for credit likely remains intact.

|

Singapore

Ronie Ganguly

PIMCO

Neutral

|

|

The Asian IG market has exploded with issuance and seen a much wider participation – improving the depth and width of the market. These are strong structural positives for a wider investor base likely to focus on Asian credit. On the flip side, the persisting low-rate environment has allowed for weaker quality of issuers and lighter covenants in new issues. This will lead to more special situations and restructuring going forward – making the presence of strong research and bottom-up analysis a key for success in this market.

|

Charles Ooi

Tahan Capital

Positive

|

|

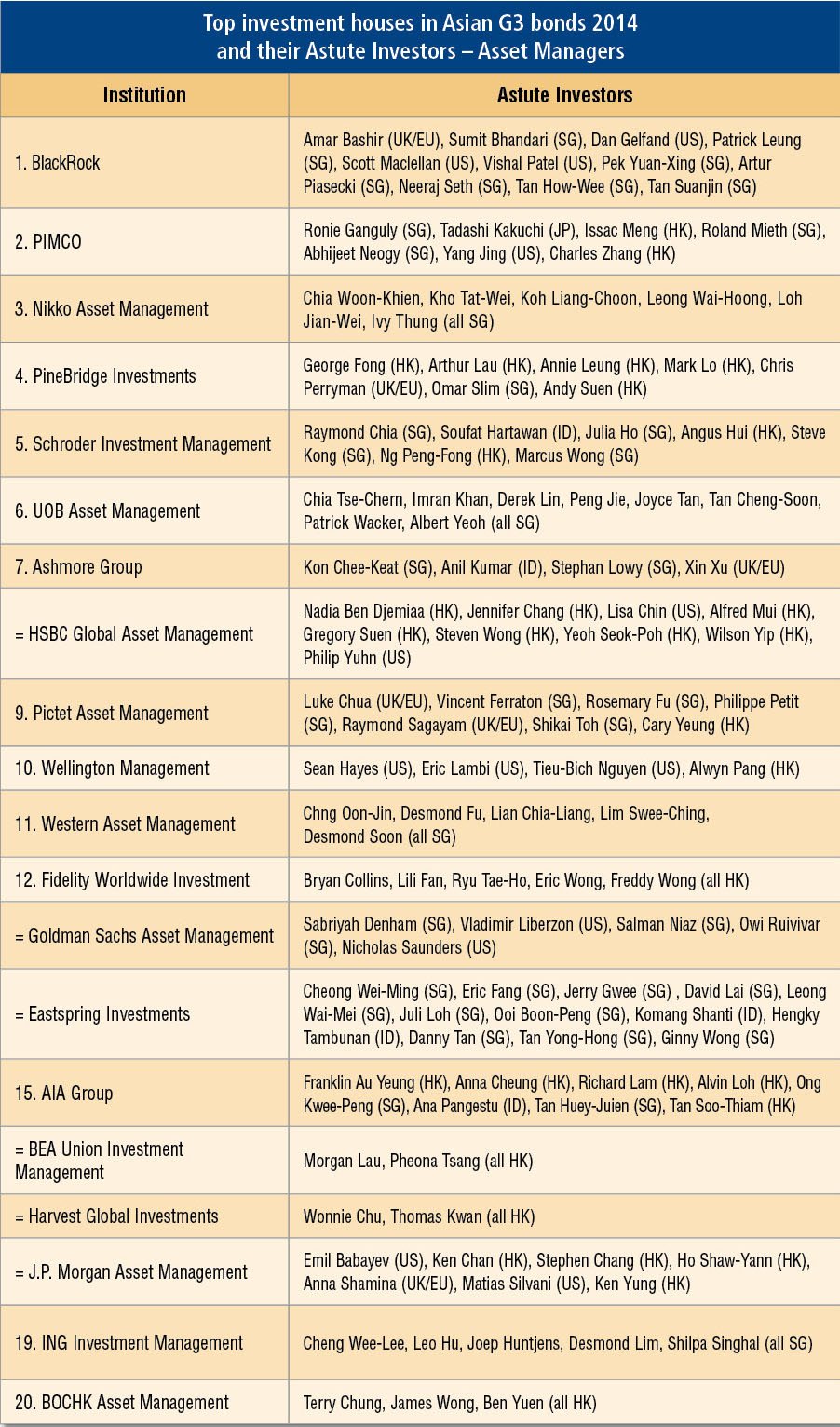

| Top investment houses in Asian G3 bonds 2014 and their Astute Investors – Asset Managers (Click to enlarge) |

The monetary policy of G4 central banks is expected to remain relatively accommodative, though volatility will pick up as the market continues to gauge timing and impact of the US Fed’s first rate hike. Investment grade spreads remain attractive given overall stable credit fundamentals and supportive banking environment – volatility will present opportunities to accumulate bonds. Idiosyncratic risks will rise in HY, hence bottom up securities selection is key.

Mark Thurgood

Saka Capital

Positive

A year is likely to be a very long time in credit given the potential for headwinds from US interest rate policy, China macro data, and geopolitical concerns. However, as Asia remains a growing and deepening credit market, there are likely to be substantial opportunities for positive performance during the course of the next 12 months in both investment grade and high yield.

|

China

Danicus Zhang

China Asset Management

Negative

|

|

Although Asian credit spreads remain attractive on a relative value basis compared to other markets, in current circumstances (US treasuries, slower Asian emerging market (EM) growth, political turbulence etc.), the spreads have limited space to tighten further. So in my view, the outlook for Asian G3 bonds is negative, and the total returns are likely to be relatively subdued.

Indonesia

Soufat Hartawan

Schroder Investment Management

Negative

The interest rate normalization in the US will enter a new stage next year after the bond purchasing programme ends this year. The Asian bond market will be challenged by liquidity gradually shrinking while the current credit spread has not fully discounted such factors. We believe there will be a re-adjustment of long-term risk premium going forward after years of low-rate environment.

|

Ezra Nazula

Manulife Asset Management Indonesia

Neutral

|

|

| Top investment houses in Asian G3 bonds 2014 and their Astute Investors – Hedge Funds (Click to enlarge) |

The higher trajectory of US treasury yields will weigh down on Asian G3 bonds, although pressures could be alleviated by positive sentiments from improving macroeconomic conditions and fiscal reforms.

Korea

Lee Hee-Yeon

Woori Investment & Securities

Positive

The growth outlook for the global economy has deteriorated due to the recent “burdening” situation including ongoing geopolitical risk, economic downturn and even possible deflation in the Eurozone, as well as acceleration of dollar strengthening, the rising preference for safety asset and the tendency to defer risky investment. The revision in the Asian G3 bond market seems inevitable, but the worsening situation will stir up the need for more stimuli such as additional Eurozone quantitative easing (QE) and delay of base rate increase from the US Fed and the Bank of England which will continuously support long-term money inflow to the global IG bond market.

I believe that the most effective strategies for the end of 2014 and the first quarter of 2015 in response to drying market liquidity and portfolio rebalancing demand seem a conservative portfolio management and look out for bottom-fishing chance. However, the next 12-month outlook for the Asian G3 bond market is still positive considering relatively stable buying demand and better market sentiment.

Spotting the right moment to buy and build up portfolio is an incessant task for investors. Now we are standing before numerous uncertainties coming from the monetary policy lag among leading countries, a looming nervousness in carry trade movement due to rising currency volatility, possibly temporary geopolitical risk, and decelerating Chinese economy and its shadow-banking concerns. However, I believe that the market turmoil will be moderately contained due to the excessive global liquidity, the learning effect from the Bernanke Shock, and the year-long preparations by market participants and policy-makers. I expect real money will take the lead in the emerging markets, especially the Asian G3 bond market in the midst of continuing global low rate condition.

|

Malaysia

Jason Wong & Amy Poh

Hong Leong Bank

Neutral

Asian USD bond spreads have compressed. Asian low beta IG names are getting expensive, offering a small 20bp-30bp pickup over similar rated peers in the US. The higher beta IG names and HY space have also rallied in H1 2014, and are somewhat prone to a selloff on the back of idiosyncratic events. We would advocate staying in the low beta IG space, and be compensated by going into long bonds. Given our expectations of an uneven recovery in the US, we think the USD rate curve will likely stay flat. Following that, we believe buy-and-hold investors, such as pension funds and life insurance funds would be keen to pick up bonds when long-dated yields rise.

Rosalind Kong

Maybank

IG – Positive; HY - Neutral

With rising global yields and potential USD strength, the Asian bond markets in general will be under pressure. However, we are still a bit more constructive on IG as not all markets react similarly, depending on their domestic conditions and valuations. Hence, if there were to be any monetary or fiscal measures to support the economy, it would generally be more positive for credits of higher grades.

Also, with the low rate environment in the Euro region and talks of sovereign fund diversification, there will be persistent interest in the EM IG space in search of yields to stay invested. As the relative valuations between IG and HY become compressed (HY at a multi-year low), any global investor considering to invest in Asia will likely be more tempted by the IG space.

As we move into 2015 with the general perception of rising interest rates of US treasuries and economic pick up from the US, there will be more volatility in the HY space. No doubt HY is less rate-sensitive and more growth-inclined, Asian HY yield spreads are at multi-year lows and any volatility will expose this asset class on the downside.

The majority of HY names are in China be it property, industrials or mining and they are slowly showing deteriorating sales and commodity prices which will eventually translate into the price of the debt and spreads. However, having said that, we can see that the Chinese government is taking proactive measures to curb the slow growth and these will ease pressure to allow property developers to manage their inventories effectively. With this in mind, there is still a compelling story to still be invested in this space. We will be selective in looking at the better quality names especially if they are SOE-backed and with bigger projects.

|

Maggie Wong

Affin Hwang Asset Management

Neutral

|

|

| The most Astute Investors in Asian G3 denominated bonds in 2014 (Click to enlarge) |

In view of the rising rate environment, we are neutral to slightly positive on the Asian G3 bond market. Given tight credit spreads, we think Asian credits are not susceptible to sell-off in rates. Nonetheless, Asian credits still offer an attractive spread pick-up relative to US and European credits that could continue to attract global fund flows into the Asian G3 bond market. In the next 12 months, we favour IG over HY due to expensive valuations and deteriorating metrics in the HY space.

Middle East & North Africa

Manoj Mahadev

Arab Banking Corporation

Negative

The sentiment towards the Asian G3 bond market from our perspective is negative over the next 12 months. A potent combination of rising US yields and challenging economic fundamentals especially from China and India is going to push the market towards negative returns. Also, a few Asian economies are reeling under inflationary pressures and the US rates scenario could compound the fact further by capital outflows and reserves depletion. The next 12 months could see flows from EM to DM and skewed towards equity. We probably don’t see a stress in credit metrics but idiosyncratic risks are expected to get heightened, especially in the HY sector. We also expect volatility to rise over the next six to 12 months and anticipate heavy issuances on the primary front.

Philippines

Nadine Alapan

Banco de Oro

Positive

Despite the shadow of China’s weaker growth prospects over the region, the economic outlook in Asia remains broadly positive. The expected growth seen in India, Indonesia, Thailand and the Philippines mitigates the slowdown in the region’s largest economy as a result of current balancing of structural reforms and economic growth.

Voltaire Cabral

Bank of the Philippine Islands

Neutral

Asian bonds would continue to benefit from accommodative policies in Europe and Japan. And until we see escape velocity in the US, Fed monetary tightening will be a very gradual process. Also, geopolitical concerns in the Middle East and Latin America should augment flows into Asian bonds.

Rustum H Corpuz Jr

Development Bank of the Philippines

Neutral

What investors were preparing for this year could actually happen in the next 12 months. With the strategies already in place and early 2014 providing a sort of a dress rehearsal for what might actually happen, conditions might not turn out that badly. Now more than before, selection would be paramount to take advantage of rare opportunities to outperform the market.

|

UK/Europe

Alistair Ling

GLG Market Neutral Fund

Neutral

|

|

Alistair Ling

GLG Market Neutral Fund

Neutral

Asian credit will probably start 2015 on the back foot as investors are confronted with the challenging combination of 1) the deteriorating credit cycle in China 2) increased levels of Asian corporate leverage; and 3) valuations at historical tights in spreads/yields. This fragile combination is exacerbated by banking regulatory capital constraints that would leave markets with an undersized catcher’s mitt to facilitate an orderly redistribution and re-pricing of risk. Having said that, it’s not all bad news with the global validation of Larry Summer’s ‘secular stagnation’ fears, meaning that rates will likely stay low and the reach for yield via credit will continue with good structural support.

Amy Kam

GAM

Neutral

Asia is getting expensive vs other EM except for China. China will likely remain high beta due to slower growth trajectory and domestic reform, though EM assets are supported by low treasury rates.

Philipp Good

Fisch Asset Management

Neutral

We view the lower growth expectation in China as a negative. The property market is likely to cool down further. On the other hand, we can expect that the government and therefore the People’s Bank of China will do whatever it takes to ensure stability. Overall, this will have impact on the other Asian countries that depend on the China growth story such as Korea, Malaysia and Indonesia.

|

Raymond Sagayam

Pictet Asset Management

Negative

|

|

| Overall market outlook comparison between 2013 and 2014 for most Astute Investors (Click to enlarge) |

The Asian hard-currency bond market has increased from approximately US$150 billion in September 2009 to US$500 billion currently. While investible, dedicated assets have also grown during this period, I feel this 28% annual compounded growth hasn’t been fully matched by a commensurate increase in market depth. I am not entirely convinced that the broad investor community has had the time to develop a deep understanding of all the new names nor has there been an improvement in market liquidity. As a result, the potential for single-name/sectoral disappointment down the line with a lack of exit liquidity is quite high. I think this degree of growth is, to an extent, mirrored in other EM regions but not to the same extent as in Asia.

It is also worth considering that in recent weeks, Asian credit has outperformed relative to US and European high-yield which have been more affected by outflows. This relative outperformance also implies there is a valuation consideration.

Richard Lange

Stone Harbor Investment Partners

Positive

We believe Asian credits will continue to show good performance as an asset class given the combination of investor demand, growth in Asian economies and relative attractiveness of spreads. In particular, we think Indian corporates and new form of bond instruments (Tier 1, Tier 2 capital securities) will provide an attractive return.

|

US

Tieu-Bich Nguyen

Wellington Management

Neutral

|

|

We have a neutral view on the Asian G3 bond market in the year ahead but have a sanguine view on the Asian credit market from a long-term, structural perspective. In the near and medium term, we believe that Asia will continue to exhibit stronger macro-economic fundamentals than Latin America and emerging Europe as the region starts to shift from a high current account surplus/savings region to one which will focus more on consumption and domestic growth stories. This ongoing economic transformation underpins stable corporate credit fundamentals, although we recognize that the deleveraging trends in the Asian credit space have waned as Asian issuers gear up to capture growth opportunities.

It is clear that there is a growing trend among Asian issuers to focus more on growth and M&A, driven by macro expansion and broad growth in the industrial and financial sectors. On balance, technicals will be challenging due to the anticipated supply from Asian issuers who aim to take advantage of lower rates in the USD market to obtain financing as well as the growth of new segments in the market such as SBLC issues and the growth of Basel III bank issuance. We expect the latter to comprise a larger part of the market due to the growth and capital needs of Asian banks, including the Chinese megabanks, the limited fiscal capacities of governments to provide financing, a trend that one can observe more widely in emerging market countries and the growing demand for infrastructure and other investment needs.

Offsetting this robust supply pipeline is the growing interest in Asian credit markets from non-Asia-based investors and the attractive premia offered by Asian credits over similarly rated credits in the developed markets. In addition, the universe has become more diverse due to the growth of issuance from Chinese corporates and banks as well as the growth in issuance from India and Indonesia.

John Espinosa

TIAA-CREF

Neutral

The overhang of interest rate normalization from the Federal Reserve and its monetary policy divergence with other major central banks will continue to provide an uncertain macro-backdrop for the Asian G3 credit markets. Given such uncertainty credit selection, carry, and duration management should prove key to generating outperformance in the year ahead.

Across the regional sovereign space, in China we remain vigilant on the rebalancing progress, along with downside pressures to growth, and potential for negative systemic events from the property and financial channels. India should continue to benefit from positive investor sentiment, but execution on policy reform, reducing inflation, and a pick-up in growth is tantamount to maintaining this positive momentum. In Indonesia, we are less optimistic on major reform prospects from the incoming government, but view that broad macro stability will remain. The Philippines and Sri Lanka continue to stand out as countries with positive credit trajectories. From a technical standpoint, net supply trends should remain a positive for the Asian G3 sovereign debt markets in the coming year.

In the Asian G3 corporate landscape, we are constructive on IG corporates where balance sheets have broadly been stable and also favour quasi-sovereign credits that stand to benefit from longer term structural reforms in select countries. Many Indian corporates remain globally competitive and still offer reasonably attractive returns especially with the reduced threat of the sovereign losing its investment grade rating status. We remain cautious on China property, however, outside of that sector there are select opportunities in HY corporates where balance sheets and liquidity are appropriately positioned for the current credit cycle. Further issuance of Basel III compliant bank capital will be an important trend to monitor and could provide relative value opportunities particularly in stronger banking systems. Supply will remain high, especially if the rate environment stays benign, but should be well absorbed given Asia offers diversification from other regions that have greater geopolitical noise.

Javier Segovia

TCW

Positive

I am positive in relative terms. I think that returns will be lower in the region next year compared to this year, but they will still outperform the EM corporate index (like this year).

Johnny Mak

Prudential Fixed Income

Positive

Over the next 12 months, the region remains a bright spot in overall global growth and some countries, such as Japan, China, and Korea may benefit from lower commodity prices. Regional fund flows, along with our view that US interest rates will remain low in the year ahead, should provide support to the asset class. Structurally, the emerging markets debt universe has expanded and provides diversified opportunities within its individual sectors. The composition of Chinese credits within the region has dominated issuance. While we are cautious on economic growth in China, we feel there are attractive opportunities in individual credits within the region compared to other emerging markets and global debt.

Editor’s Note: Investors that ranked within the top 5 were invited to express their views. These award-winning individuals are presented in rank order by region. Their responses were gathered in October 2014.

.jpg)

.jpg)