|

|

|

As the year of the amicable and gentle Wood Goat gives way to that of the ambitious yet irritable Fire Monkey, there looks to be much unease in the realm of finance. Nevertheless, fortune favours the brave, and the discerning. Now more than ever, it is important to tease apart the differing fundamentals of the various markets in Asia so as to divine their divergent prospects.

The start of fiery financial markets?

The financial markets have already begun to show signs of the irritability that is characteristic of the Year of the Fire Monkey. The simmering unease that had been going on since August 2015 finally boiled over in December, after the RMB acquired its reserve currency status and the authorities seemed to let the currency fall in line with the market’s pull. This ironically reignited questions about the authorities’ plans for the RMB and their commitment to reform. Old tales of mercantilist devaluation were revived and whispered gossip of currency wars abounded.

Adding oil to the fire was….well, oil. An exacerbation of the extended weakness in the crude market, after OPEC demurred from a decision to cut production that the market had expected, sent clouds of doubt billowing through the markets. Deflationary fears dominated some parts of the narrative and others wondered if it wasn’t weakening demand that was contributing more to the weakness in the price of oil. The prospect of a return of Iranian and US supply to the international markets will likely continue to weigh on the fortunes of that market.

In the background though, other dangers lurk. The US Federal Reserve finally pulled the trigger on the first rate hike but this has not reduced the uncertainty surrounding the pace at which normalization will take place. Europe’s growth prospects look better but worries remain over the political landscape, potential debt-related instability, and the risk of a ‘Brexit’. Japan too is clouding the horizon with its faltering growth and stop-start structural reform moves.

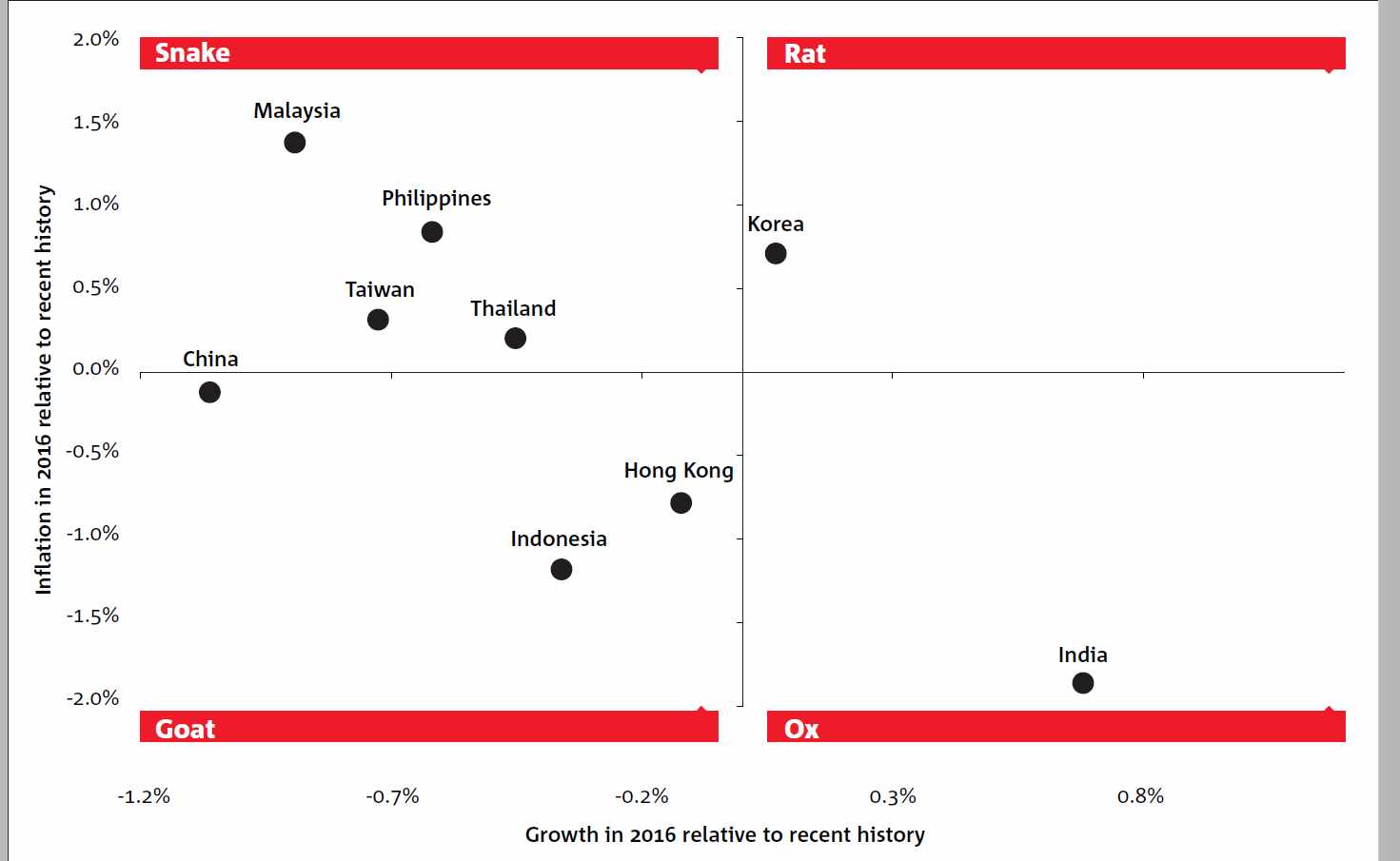

In this environment, the characteristics of some will allow them to thrive, while others could struggle. The qualities of the Ox and the Rat, according to Chinese astrology, are well suited to the nervous energy of the Monkey, while those of the Goat and the Snake might lead to less harmonious outcomes.

(Graph extracted from National Australia Bank’s ‘Essential Asia’ report, December 2015)

More fun than a barrel of monkeys for India & Korea?

Alone amongst the Asia ex-Japan economies is India, which possesses characteristics that most resemble those of the Ox. The Indian economy at this juncture, possesses a degree of strength unmatched by the rest of Asia, with the market expecting a substantial acceleration in 2016’s GDP growth relative to that of the previous years. The domestic drivers – consumption and investment – still seem to be champing at the bit while easing inflation, and the scope for further policy easing that it provides, adds dependability to that strength. The Ox’s robustness should be able to adequately cushion against the Monkey’s capriciousness.

Korea, on the other hand, seems to possess the quiet pace of the Rat. Expectations are for 2016’s GDP growth to mildly exceed the previous years’ rates but at the same time, inflation is also seen as accelerating, which might entail a tightening of monetary policy. The dependence on the global economy and its larger neighbour China, lend a certain amount of fragility to Korea’s growth prospects. Nevertheless, the Korean economy mirrors the Rat’s adaptability and resourcefulness, in terms of the scope to let the currency adjust, allied with the resilience of its domestic growth engines.

Markets possibly with a monkey on their backs

In the temperamental environs of the Monkey year, the economies that currently resemble the Goat’s attributes – China, Indonesia and Hong Kong – might see some discomfort. While usually stable and mild, the combination with Monkey brings out the Goat’s inner irascibility. This certainly applies to China, and by extension, Hong Kong. China’s domestic reforms generate their own confusion that compound the uncertainty from the external environment.

In the temperamental environs of the Monkey year, the economies that currently resemble the Goat’s attributes – China, Indonesia and Hong Kong – might see some discomfort. While usually stable and mild, the combination with Monkey brings out the Goat’s inner irascibility. This certainly applies to China, and by extension, Hong Kong. China’s domestic reforms generate their own confusion that compound the uncertainty from the external environment.

Indonesia is also undergoing a similar adjustment, albeit to a lesser extent. The attempt to move up the value chain has seen a disruption to some of their metal ore exports, although the current weak commodities market reduces the opportunity cost of these endeavours. All three of these economies are expected to see a deceleration in their growth rates but given their benign inflation outlooks, they are unlikely to lose their footing and might just bounce back before long – just like the Goats they resemble.

The final group likely to find most difficulty coexisting with the Monkey is the one that bears the attributes of the Snake. The Monkey is said to bring out the worst in the Snake - an apt metaphor for the current economic conditions in Taiwan, Philippines, Thailand and Malaysia where the slowdown in China has left its mark. Additionally, the commodity slump has hit Malaysia hard while the lack of a revival in merchandise export demand has hurt Taiwan and the Philippines. The overall risk-aversion could, consequently, inflate the significance of Thailand’s domestic political tensions. The group is expected to see a deceleration in growth and robust inflation means it would be difficult for monetary policy to be employed to ameliorate their inherent sluggishness

The year of the Fire Monkey therefore offers rewards to the adventurous and ambitious who are cognizant of the different compatibility of each economy with the broader environment. Watch where you step and you might just manage to avoid chasing your tail!

(See NAB's predictions for last year )

Christy Tan is the Hong Kong-based head of markets strategy and research - Asia, National Australia Bank Limited

Julian Wee is senior markets strategist - Asia, National Australia Bank Limited