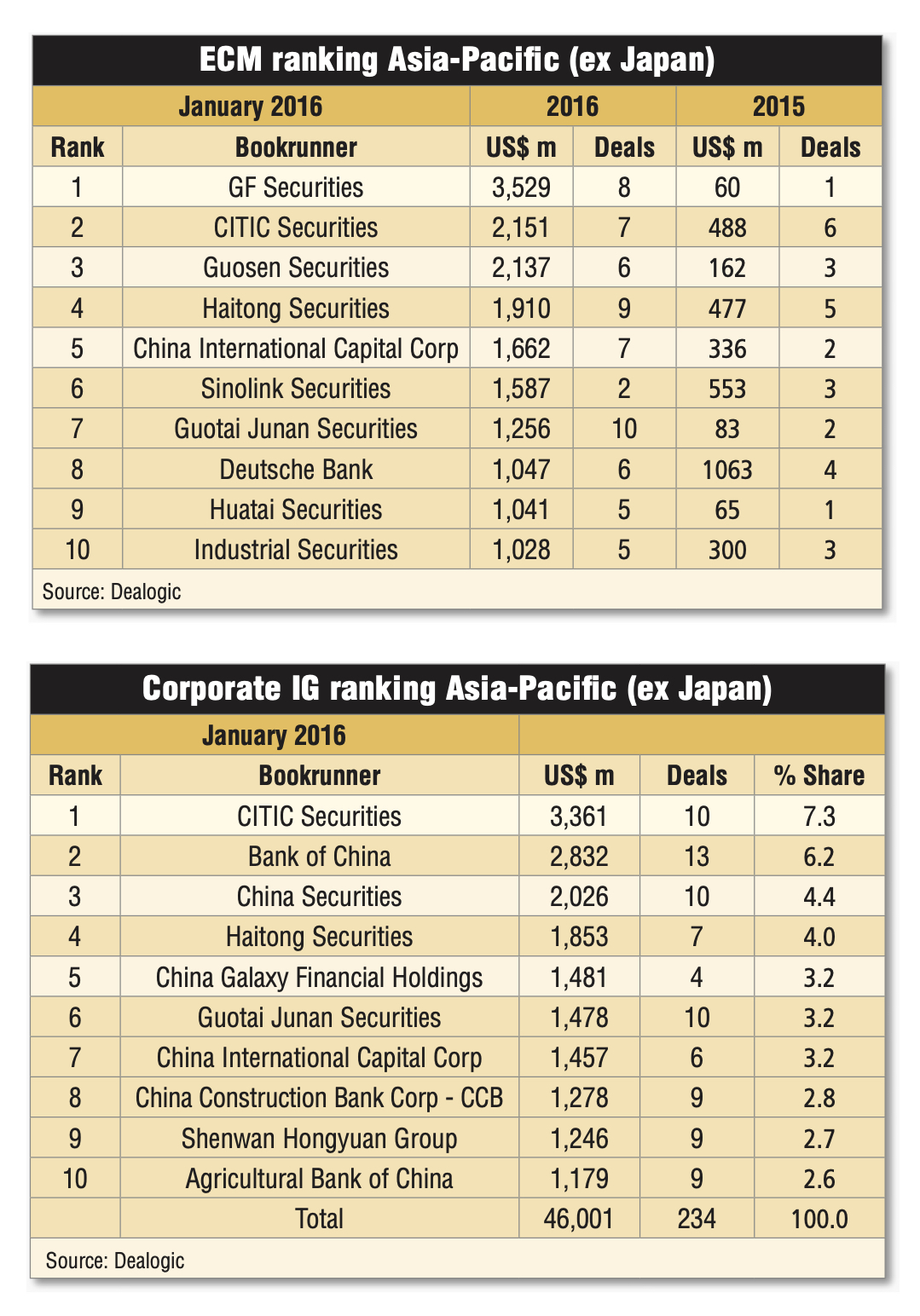

GF Securities is not the only Chinese underwriter on the ECM Asia Pacific (ex-Japan) top-ten league table. Indeed, other than Deutsche Bank, the rest of the ranked houses are from China. GF topped the league raising US$3.5 billion from eight deals followed by Citic Securities with US$2.1 billion from seven deals and in third is Guosen Securities with a similar US$2.1 billion raised from six deals.

It is not just in the ECM ranking that Chinese underwriters are starting to feature prominently. A similar pattern is also notable in the ranking for debt capital markets (DCM). The latest Asia Pacific (ex-Japan) corporate investment-grade (IG) volume, which combines G3 and local currency, has Citic Securities at the top of the ranking with a total volume of US$3.4 billion from 10 deals. In Dealogic’s latest top-ten ranking for January 2016, not a single international bank featured.

A DCM veteran and head of debt syndicate at an international house says that especially in the past year, he is feeling the winds of change. “These days at the syndicate desk and especially when pricing a deal I am surrounded by Mandarin-speaking, 25-year-olds,” he chuckles. “The desk now has to arrange more China-related deals than ever.”

The number of sizeable deals listing in Hong Kong is now largely from China. In 2015, for example, Hong Kong was the largest IPO market in the world on the back of several deals from China’s financial services sector including Huatai Securities, GF Securities, China Huarong Asset Management Co and China Reinsurance (Group), among others. Together, these four deals account for US$13.5 billion raised or 40% of the total funds in 2015, according to a report by KPMG.

The number of sizeable deals listing in Hong Kong is now largely from China. In 2015, for example, Hong Kong was the largest IPO market in the world on the back of several deals from China’s financial services sector including Huatai Securities, GF Securities, China Huarong Asset Management Co and China Reinsurance (Group), among others. Together, these four deals account for US$13.5 billion raised or 40% of the total funds in 2015, according to a report by KPMG.

It is mirrored on the DCM side with the largest G3 bonds also from Chinese issuers. Bankers estimate that issuers from China now account for up to 65% of the market annually. Deals of US$1 billion upwards now feature regularly from issuers such as the Sinopec Group, China Minmetal, China Bluestar and China Communications Construction on the corporate side supplemented by large deals from Chinese financial institutions such as Bank of China, Huarong Asset Management, Agricultural Bank of China and Industrial and Commercial Bank of China.

The head of syndicate at a Chinese bank says he expected that over time Chinese underwriters for both equity and debt will begin to rank among the top houses in the region. “The increasing number of Chinese companies tapping the capital markets makes this inevitable,” he relates. “But I was surprised at the speed and how quickly Chinese investment banks are now competing alongside the international houses.”

There is a big factor on the demand side as well. Following the meltdown of China’s stockmarkets from the middle of 2015 to date together with the weakness of the renminbi versus the US dollar, Chinese investors also have been turning to the overseas markets for investments. As has been the case in other countries, Chinese investors are putting their overseas funds to work by buying Chinese securities whether equity or debt. “These investors are more familiar and prefer to buy Chinese names they know,” says one bond syndicate manager. “We are seeing the so-called domestic bid that have driven the technicals we regularly see in the Asian G3 bond market where home buyers support household names they know.”

One indicator of the recent growth is the total assets under management of QDII funds (qualified domestic institutional investor), the scheme that permits Chinese investors to buy overseas securities. Since August 2015, QDII funds invested offshore has reached 66.2 billion yuan (US$10.2 billion), a jump by close to 20% by the end of 2015 according to the Asset Management Association of China. The State Administration of Foreign Exchange has dramatically increased the QDII quota in 2015 to over US$507 billion, more than the total quota approved from 2007 to 2014 of US$392 billion.

PwC, the international accounting firm, believes that 2016 will be a continuation of 2015. “We believe that fundraising by IPOs in Hong Kong and China will be even more buoyant,” says Benson Wong, assurance partner at PwC Hong Kong. “We estimate that there may be more than 10 IPOs raising between HK$5 billion (US$641 million) and HK$10 billion and seven to eight mega IPOs raising over HK$10 billion in Hong Kong in 2016.”

One area where the visibility of Chinese investment banks that is not yet as apparent as in ECM and DCM is M&A advisory. The latest ranking from Dealogic showed that while China International Capital Corp (CICC) is at the top of the January table with a total value of US$11.4 billion advised from three deals, it is joined by a large number of international houses such as Credit Suisse (ranked second with US$10.5 billion, 7 deals) and Bank of America Merrill Lynch (ranked 3rd with US$8.5 billion, 3 deals). But already three of the top ten houses are Chinese investment bank advisers.

An M&A banker shares that he is seeing Chinese banks muscle into deals largely on the back of the financing they are able to offer companies to finance takeovers. “When they get into deals, they also get to learn how to put them together,” he says. “It is a matter of time when we will see more Chinese M&A advisers as part of the large China-related M&A deals.”

It is not necessary to wait too long. The recently announced takeover of Syngenta by ChemChina, which has a deal value of US$43 billion is being advised by HSBC and Citic Bank International. With more Chinese companies going overseas to acquire technology and resources, the 2016 ranking of M&A advisers for the Asia-Pacific will almost certainly include more than a handful of Chinese M&A advisers.

In answer to the first question, GF Securities – the top ECM house in January 2016 – started life as the securities unit within China Guangfa Bank (formerly known as Guangdong Development Bank). It was spun off as a separate legal entity in 1996 and was listed on the Shenzhen Stock Exchange six years ago via a reverse takeover of Yan Bian Road Construction Co. (延邊公路建設股份有限公司).

In 2015, it joined the number of Chinese securities companies that listed on the Hong Kong Stock Exchange raising US$4.1 billion in an IPO that was oversubscribed by 49 times. Its share price traded up by 42% on the first day. It is The Asset Triple A Best IPO of 2015.

| ECM Bookrunner - Year to Date | |||||

| Year to date | |||||

| Rank | Bookrunner | ||||

| 1 | GF Securities | ||||

| 2 | CITIC Securities | ||||

| 3 | Guosen Securities | ||||

| 4 | Haitong Securities | ||||

| 5 | China International Capital Corp | ||||

| 6 | Sinolink Securities | ||||

| 7 | Guotai Junan Securities | ||||

| 8 | Deutsche Bank | ||||

| 9 | Huatai Securities | ||||

| 10 | Industrial Securities | ||||

| Asia Pacific (ex Japan) Corporate IG Ranking | |||||

| Year to date 02/01/2016 | |||||

| Rank | Bookrunner | ||||

| 1 | CITIC Securities | ||||

| 2 | Bank of China | ||||

| 3 | China Securities | ||||

| 4 | Haitong Securities | ||||

| 5 | China Galaxy Financial Holdings | ||||

| 6 | Guotai Junan Securities | ||||

| 7 | China International Capital Corp | ||||

| 8 | China Construction Bank Corp - CCB | ||||

| 9 | Shenwan Hongyuan Group | ||||

| 10 | Agricultural Bank of China | ||||

| Total | |||||