|

|

For three days in a row, the PBOC devalued the renminbi in its daily fixing against the USD – 1.8% on Tuesday morning, 11 August, 1.6% on Wednesday morning and 1.1% on Thursday morning - a total of 4.5% in three days. The devaluation move stoked a sell-off in the currency in both the onshore and offshore markets. By the middle of the second day, the onshore market had fallen by 4% while the offshore market (CNH) had fallen by 6% before the PBOC reportedly intervened to pull back the markets.

Killing two birds with one stone – liberalising the fixing and devaluing

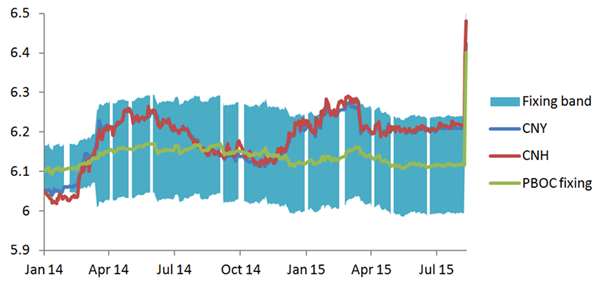

It all started with the PBOC making a surprise announcement on Tuesday morning, 9:15am local time that it was doing a one-off “adjustment” to its daily USDCNY central parity fixing to align itself to the actual spot market which has been trading weaker than the official fixing by 1% on average since late last year (1.4% at Monday closing, see Figure 1). The PBOC also said that going forward, the fixing would be determined by quotes from 35 market makers, with a majority being Chinese banks, complemented by a handful of China-based foreign banks. By adopting a market-based official fixing, the PBOC said it would work at converging the onshore and offshore FX markets.

Market participants who initially saw the PBOC’s announcement on Tuesday morning more as a liberalisation move rather than a devaluation move were subsequently convinced there was some degree of devaluation intended by the policymakers. In our view, the two objectives hold equal weight – the need to switch to a free market mechanism and second, the need to revive growth.

Figure 1: Actual market closing on onshore USDCNY and offshore USDCNH vs PBOC’s daily fixing

Source: Bloomberg, Nikko Asset Management

IMF endorsement

China has long made known its desire to have the RMB included in the IMF’s Special Drawing Rights (SDR). Likewise, the IMF has been increasingly clear that it would support China’s bid for SDR inclusion. To the extent that the IMF recently said the criterion of “free usability” does not require the SDR component currency to be fully convertible, the IMF is saying that some degree of market controls can be allowed. However, there was a question about the CNY’s official exchange rate being a true market rate given that the actual spot market was trading nowhere close to it. Hence, it was inevitable that the PBOC has to “fix its fixing”. And it seems clear that the move was sanctioned by the IMF ahead of the announcement as the IMF released a statement on Wednesday – the day after the PBOC’s move – to say it welcomes the PBOC’s move and that the consequent devaluation of the RMB would not impact the SDR decision.

Forex devaluation is a reinforcement rather than substitute to interest rate cuts

Based on the data regarding external trade, CPI, PPI, monetary aggregates and industrial output for July released over the past few days, the Chinese economy did seem to weaken further in Q2. The pressure has thus mounted on policymakers to act more in propping up growth through all channels – one of which is exports, which would benefit from devaluation. However, devaluation policy is a double-edged sword. First, it is difficult to “control” the quantum of devaluation without having to intervene at some point to prevent a free fall and intervention has the consequence of tightening domestic liquidity. Devaluation is thus not a substitute to interest rate cuts. Second, only export industries have direct benefits from devaluation, while industries that import suffer and the non-tradeable sector receives no direct benefits. With inflation being of no concern, interest rate cuts are therefore still needed to support the rest of the economy. In short, devaluation reinforces interest rate cuts as an overall monetary easing.

RMB is about 5-10% overvalued

Since the last devaluation in January 1994, China has never used forex as a policy tool to either support growth or fight inflation. In the aftermath of the 2008 global financial crisis, the RMB has in fact taken on the role to shore up China’s stature in the global arena by maintaining a stable to gradually appreciating pace. This has caused the RMB’s real effective exchange rate (REER) to appreciate by over 30% versus its long-term average starting from 2000 (see Figure 2). Adjusted for the output gap and current account gap, our in-house model evaluates the overvaluation gap to be about 5-10%. We thus believe the PBOC’s aim is to devalue the RMB by a magnitude of 5-10% in a controlled step-wise fashion.

Figure 2 – RMB real effective exchange rate (REER) vs fundamental equilibrium exchange rate (FEER)

Source: Bloomberg, BIS, Nikko Asset Management

Liberalisation pushing into bond market

In the big scheme of China’s market liberalisation, we note another important recent "liberalisation" step in the bond market. The Liaoning local government bond issuance last Friday was the first of this newly created municipal/local government bond market to be issued at "real" market levels. The coupons for its 5y and 10y bonds were set 29bp and 52bp spread above the 5-day average CGB curve, hitting the 15% cap set on these spreads. Until last Friday’s Liaoning auction, every auction had come in virtually flat to the China Government Bond (CGB) curve. The initial market chatter was that the poor Liaoning auction was due to the local government's failure to engage more than its two regular banks to participate in the auction, which fell short of its targeted amount. A less clear point was whether that the central government has decreed that banks no longer needed to support local government auctions. If so, this would not surprise us, as after the latest exchange rate policy overhaul, we believe local government bond market will become a major part of the overall liberalisation drive.

Delay in SDR inclusion improves chance of a higher SDR weight

All leads to the question on the RMB's bid for SDR inclusion which the IMF said last week that it could be delayed to September 2016. The delay we believe is to give China more time to promote the RMB to other central banks to hold the RMB in their reserves. The SDR weight is calculated as an average of the RMB's use in international trade and the RMB's representation in world reserves. Without much of the second, the RMB's weight would come well below 10% and China would be stuck with a low SDR weight for five years since the SDR review is a five year-cycle. Delaying it by a year, there is good chance for China to achieve 15-20% in the SDR given that it already scores very high on the first factor and this weight will serve them for a good five years.

Short-term pain for long-term gain

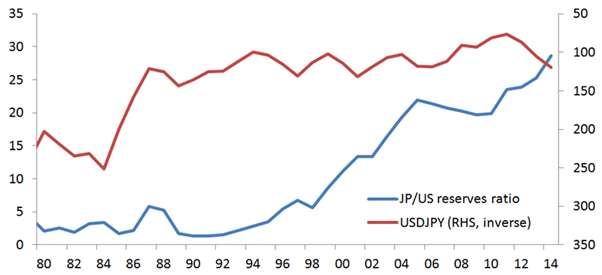

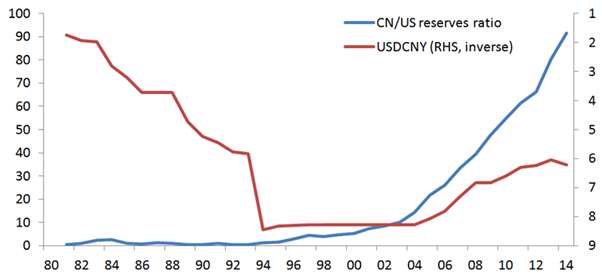

Over the coming year, as China gains more success in promoting the RMB to other foreign central banks, the mere substitution of USD for RMB by the world’s central banks would act as a stop to the free fall of the RMB. Once included into the SDR, the RMB will also gain seigniorage value as a reserve currency. In this regard, we only have to extrapolate the Japanese yen’s pace of appreciation over the two decades after its inclusion into the SDR in 1980 to gauge where USDCNY could be heading on a very long-term horizon (see Figure 3 and Figure 4).

Figures 3 & 4: The Japan precedent for SDR inclusion

Source: Bloomberg, Nikko Asset Management

Source: Bloomberg, Nikko Asset Management

Conclusion

We believe that while RMB weakness will persist for a few months until at least the Fed’s first rate hike, we don’t expect the currency to devalue more than 10% versus USD and we maintain our confidence that the currency will be included into the IMF SDR basket in a year from now. Thereafter, the currency will likely be on a long-term appreciation path.

Chia Woon Chien is senior portfolio manager for fixed income at Nikko Asset Management